For most people, term life gives the same protection at a fraction of the cost, while whole life locks you into lifelong coverage plus a slow-growing savings account.

Term covers a fixed period and is cheap; whole covers you forever and builds cash value but costs 5–20 times more.

Which fits you depends on budget, how long you need protection, and whether you want forced savings or flexibility.

This guide cuts through the fine print so you can pick the option that actually works when a claim matters.

Key Differences Explained for Choosing Between Term and Whole Life

Term life insurance delivers a death benefit if you die during a fixed period, commonly 10, 15, 20, 25, or 30 years. The policy pays nothing if you outlive the term, and there’s no savings account or cash value. Whole life insurance covers you for life (to age 100 or longer), builds cash value that grows at a guaranteed rate, and pays the death benefit whenever you die, as long as premiums are current.

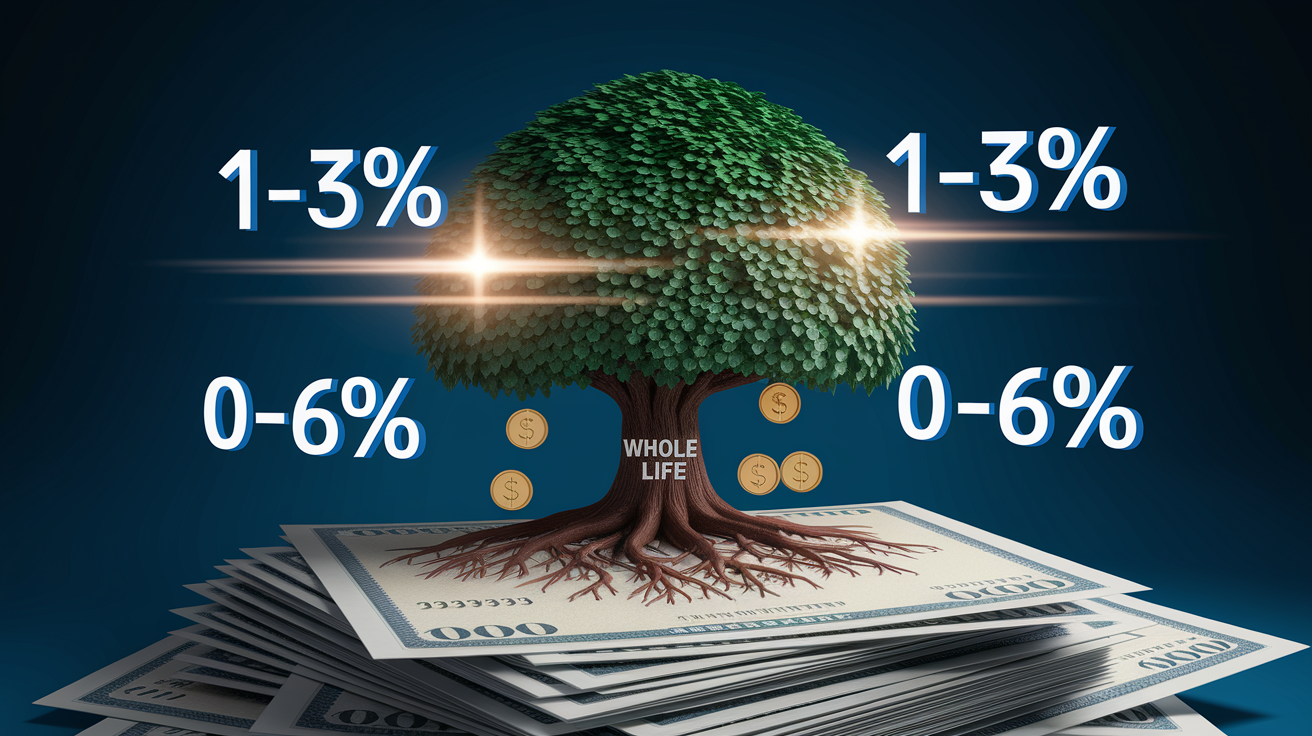

Whole life premiums run 5 to 20 times higher than term because you’re funding two things: lifelong coverage and a cash value account. The insurer must reserve enough to pay the death benefit decades from now, and a portion of each premium feeds guaranteed cash value growth, typically 1 to 3% annually, plus possible dividends if you own a participating policy. Term premiums cover only the risk of death during the term, which makes them dramatically cheaper, especially for younger, healthier buyers.

Whole life offers policy loans (usually at 4 to 8% interest) and the option to surrender the policy for its cash value, though early surrender charges can last 5 to 15 years. Many term policies include a conversion option, typically until age 60 to 65, that lets you switch to permanent coverage without a new medical exam. Term renewals are guaranteed but reset at much higher age based premiums. If you don’t convert or buy a new policy, coverage stops when the term ends.

| Feature | Term Life | Whole Life |

|---|---|---|

| Premium Cost | Low, typically $20 to $150/month for $500,000 coverage (healthy non-smoker, ages 30 to 45) | High, typically $800 to $2,500/month for the same face amount and age range |

| Coverage Length | Fixed term (10, 15, 20, 25, or 30 years) | Lifetime (to age 100+, as long as premiums are paid) |

| Cash Value | None | Guaranteed growth at 1 to 3%, plus potential dividends (0 to 6% historically); can borrow against or surrender |

| Death Benefit Timing | Pays only if death occurs during the term | Pays whenever the insured dies, as long as the policy is in force |

| Flexibility & Loans | No cash value; some policies offer conversion to permanent coverage | Policy loans at 4 to 8% interest; loans reduce death benefit if unpaid; cash can be withdrawn or policy surrendered |

| Renewal / Conversion | Can renew at higher premiums or convert to permanent (typically until age 60 to 65); coverage ends at term expiration if not renewed | Level premium for life; no renewal needed; policy remains in force as long as premiums are paid |

How Term Life Insurance Works and What It Covers

A term life policy is a contract between you and an insurer: you pay a fixed monthly or annual premium, and if you die during the term, the insurer pays your named beneficiary the face amount, often tax free. The most common structure is “level term,” where the death benefit and premium stay constant for the entire term (10, 15, 20, 25, or 30 years). If you’re still alive when the term expires, the coverage stops, and you receive nothing back. That’s by design. You’re buying protection, not a savings account.

If you need coverage after the term ends, you can renew the policy, but premiums jump sharply because you’re older and statistically more likely to die. Alternatively, many term policies offer a conversion feature that lets you switch to permanent coverage, usually whole or universal life, without a new medical exam, typically until you hit age 60 to 65 (the exact cutoff varies by insurer and policy). Conversion locks in your insurability even if your health has declined, though the new permanent premium will be much higher than your original term rate.

Key features of term life include:

- Affordability — Premiums are lowest when you’re young and healthy. A 30 year old non-smoker can often secure $500,000 of coverage for $20 to $50 per month.

- Level term vs annual renewable term — Level term keeps premiums flat for the entire term; annual renewable term (ART) starts cheaper but premiums rise each year.

- No cash value — Every dollar of premium pays for the death benefit and insurer expenses. Nothing accumulates in a savings account.

- Renewal at expiration — Guaranteed renewable clauses let you extend coverage without underwriting, but expect premiums to double or triple at renewal due to your increased age.

- Conversion availability — Not all term policies include conversion. Check the policy fine print for the conversion window and which permanent products you can convert into.

- Underwriting factors — Age, smoking status, medical history, and occupation determine your rate class (Preferred, Standard, or substandard); smokers typically pay 2 to 3 times more than non-smokers.

How Whole Life Insurance Works and Why It Costs More

Whole life insurance combines a guaranteed death benefit with a savings component called cash value. Each premium payment covers three things: the cost of insurance (mortality charges), administrative fees, and a contribution to the cash value account. The insurer guarantees that cash value will grow at a minimum rate, usually 1 to 3% annually, and many participating whole life policies also pay dividends (historically 0 to 6%, though not guaranteed) when the insurance company performs well. That cash value grows tax deferred, and you can borrow against it, withdraw a portion, or surrender the policy for its accumulated value.

Because whole life is designed to cover you for life, the insurer must set aside enough money today to pay the death benefit decades from now, even if you live to 100. That long term obligation drives premiums much higher than term: a healthy 30 year old buying $500,000 of whole life might pay $800 to $1,800 per month, compared to $20 to $50 per month for a 20 year term policy. At age 45, whole life premiums for the same face amount often run $1,200 to $2,500 per month, versus $50 to $150 for term. The premium stays level for life, which protects you from future rate increases, but you’re committing to decades of higher payments.

Whole life offers several financial features that term lacks, but each comes with trade offs:

- Dividends — Participating policies (usually sold by mutual insurers) may pay annual dividends. You can take the dividend in cash, use it to reduce premiums, buy paid up additional coverage, or leave it to accumulate at interest. Dividends are not guaranteed and fluctuate with insurer performance.

- Policy loans — Borrow against the cash value at interest rates typically between 4 and 8%. Unpaid loans reduce the death benefit dollar for dollar and accrue interest that compounds. If total loans exceed cash value, the policy can lapse and trigger a taxable event.

- Long term contractual commitment — Missing premiums or letting the policy lapse forfeits much of the early cash value. Insurers often apply steep surrender charges in the first 5 to 15 years to recoup sales commissions and administrative costs.

- Surrender charge periods — If you cancel the policy early, you receive the cash surrender value, which is the accumulated cash value minus surrender charges. These penalties decline over time and eventually disappear, usually after year 10 to 15.

Side by Side Cost Comparison of Term and Whole Life

The premium gap between term and whole life is wide enough to reshape your entire financial plan. A 30 year old male non-smoker buying $500,000 of 20 year term coverage might pay $25 to $40 per month. The same person buying whole life for the same death benefit would pay $800 to $1,200 per month, 20 to 40 times more. That difference compounds over time: over 20 years, term premiums total roughly $6,000 to $9,600; whole life premiums total $192,000 to $288,000. The whole life buyer gets cash value that grows tax deferred, but early cash value is low because much of the first decade’s premiums cover commissions, administrative loads, and mortality charges. Break even, the point where cash value plus dividends match cumulative premiums, typically takes 10 to 20 years, depending on insurer performance and dividend history.

Premiums rise sharply with age for both products, but the percentage increase is steeper for whole life. A 45 year old male buying the same $500,000 of term coverage pays roughly $70 to $120 per month for a 20 year term. Whole life at that age costs $1,400 to $2,200 per month. Women generally pay 10 to 20% less than men at the same age and health class because actuarial tables show longer life expectancy. Smokers of either gender pay 50 to 200% more than non-smokers, and the surcharge is permanent unless you quit and remain tobacco free for a specified period (usually 12 months) and then request reclassification.

| Age & Gender | Coverage Amount | Term Premium Range (monthly) | Whole Premium Range (monthly) | Notes |

|---|---|---|---|---|

| 30 year old male, non-smoker | $500,000 | $25 to $40 | $800 to $1,200 | Term is 20 year level; whole is participating policy |

| 30 year old female, non-smoker | $500,000 | $20 to $35 | $700 to $1,000 | Lower rates reflect longer life expectancy |

| 45 year old male, non-smoker | $500,000 | $70 to $120 | $1,400 to $2,200 | Premium gap widens with age; term renewals after 20 years reset at much higher rates |

| 45 year old female, non-smoker | $500,000 | $55 to $100 | $1,200 to $1,900 | Whole life premiums remain level for life; term expires at end of term unless renewed |

Matching Term or Whole Life to Your Financial Needs

The right choice depends on how long you need coverage, what you can afford, and whether you want a death benefit only or a forced savings vehicle with lifelong protection. Term fits buyers who need large amounts of coverage for a finite period, typically 10 to 30 years, to cover a mortgage, replace income while children are young, or protect a business partnership. Whole life fits buyers who need guaranteed lifetime coverage, want tax deferred cash value growth, or have estate planning goals that require a predictable death benefit regardless of when they die. Most financial planners recommend buying enough coverage to replace 7 to 10 times your annual income, adjusted for debts, mortgage balance, and future education costs.

Age plays a major role in affordability and fit. Younger buyers get the steepest discounts on both term and whole, but the absolute dollar difference favors term so heavily that most people under 40 prioritize term and invest the savings. Older buyers, especially those over 50, face much higher premiums for both products, and whole life becomes prohibitively expensive unless estate or trust funding needs justify the cost. If you’re unsure whether you’ll need lifelong coverage, start with convertible term. It locks in your insurability and gives you the option to upgrade to permanent coverage later without a new medical exam.

Choose Term Life If You…

- Need affordable, high coverage death protection for a specific time period (mortgage payoff, child rearing years, business loan).

- Are young, healthy, and on a limited budget. Term premiums are lowest when you’re in your 20s or 30s.

- Plan to invest the premium savings elsewhere (tax advantaged retirement accounts, taxable brokerage) rather than accumulate cash inside an insurance policy.

- Expect your financial obligations to decline over time (kids graduate, mortgage pays down, net worth grows).

- Want the option to convert to permanent coverage later if health declines or needs change. Look for policies with conversion clauses extending to age 60 or 65.

Choose Whole Life If You…

- Can comfortably afford higher, lifelong premiums without risking a lapse due to budget constraints or job loss.

- Need guaranteed lifetime coverage for estate planning purposes, such as funding an irrevocable life insurance trust (ILIT) or covering estate taxes on a multimillion dollar estate.

- Want predictable, tax deferred cash value accumulation that you can borrow against or use for supplemental retirement income.

- Have lifelong dependents, for example, a child with disabilities who will never be financially independent, and need a death benefit that pays no matter when you die.

- Have already maxed contributions to 401(k), IRA, and HSA accounts and seek additional tax advantaged savings vehicles (recognize that cash value growth typically lags diversified investment returns).

Cash Value, Loans, and Long Term Growth Tradeoffs

Whole life’s cash value grows slowly in the early years because much of your premium covers sales commissions (often 50 to 110% of first year premium), administrative fees, and the cost of providing guaranteed lifetime coverage. Guaranteed cash value growth is contractually set at 1 to 3% annually, and participating policies add dividends when the insurer’s investment portfolio and mortality experience perform well. Historical dividend rates have ranged from 0 to 6%, though recent decades have trended toward the lower end as bond yields fell. After 10 to 15 years, cash value begins to compound meaningfully, and by year 20 or 30, the accumulated value can represent a substantial portion of total premiums paid.

Policy loans let you access cash value without surrendering the policy, but the loan accrues interest at rates typically between 4 and 8%, and unpaid loans reduce the death benefit dollar for dollar. If you borrow heavily and then die, your beneficiaries receive the face amount minus the outstanding loan balance. Loans are not taxed as long as the policy remains in force, but if the policy lapses with an unpaid loan, the IRS may treat the loan as a distribution, triggering ordinary income tax on any amount that exceeds your total premium payments (your “cost basis”). That tax surprise can be large if you’ve borrowed aggressively against decades of cash value growth.

Comparing whole life to alternative investments exposes the opportunity cost: the $800 to $1,200 per month a 30 year old pays for whole life could instead fund a Roth IRA ($500/month = $6,000/year) and a taxable brokerage account, both invested in low cost index funds with historical long term returns around 7 to 10% annually. Over 30 years, that strategy would likely accumulate more wealth than the whole life cash value, even accounting for the tax deferred growth inside the policy. Whole life makes financial sense when you value the guaranteed death benefit, forced savings discipline, creditor protection (in many states), and the certainty of knowing coverage will never lapse due to health changes. But it’s rarely the highest return use of your dollars.

Conversion, Renewal, and Switching Options Between Term and Whole

Most level term policies include a conversion feature that allows you to switch to permanent coverage, usually whole life, universal life, or guaranteed universal life, without a new medical exam, blood work, or health questionnaire. Conversion windows typically extend until age 60 to 65, or for a specified number of years into the term (for example, the first 10 years of a 20 year term). The new permanent premium is based on your age at conversion and the rate class you qualified for when you bought the original term policy, so if you were rated Preferred at age 30 and convert at age 45, you’ll pay the Preferred whole life rate for a 45 year old. Conversion is the single best way to preserve insurability if your health has declined. Heart disease, cancer, diabetes, or other chronic conditions would either disqualify you or dramatically raise rates on a new application.

If your term expires and you don’t convert, you can renew the policy without underwriting, but premiums reset to age based rates that are often two to five times higher than your original level term premium. Alternatively, you can apply for a new term policy, but you’ll face full underwriting, and any new health issues will push you into a worse rate class or result in a decline. Replacing one whole life policy with another (or switching from whole to term) usually requires surrendering the old policy, which triggers surrender charges if you’re still within the surrender charge period (often 5 to 15 years). Surrendering also creates a taxable event if the cash value exceeds your total premiums paid. The IRS treats the gain as ordinary income.

Key switching and conversion mechanics:

- Conversion privilege — Exercise before the deadline (commonly age 60 to 65 or a term specific cutoff). You skip health underwriting but accept a higher permanent premium based on your current age.

- Guaranteed renewability — Term policies with guaranteed renewable clauses allow renewal at term end without health questions, but premiums rise steeply.

- Replacing term with new term — Requires full underwriting; new policy premiums reflect your current age and health; often much more expensive if you’ve aged significantly or developed medical conditions.

- 1035 exchange — Internal Revenue Code Section 1035 allows you to transfer cash value from one life insurance policy to another (or to an annuity) without immediate taxation. This is the tax efficient way to switch permanent policies.

- Surrender charges and taxation — Surrendering whole life before the surrender charge period ends reduces your cash payout. If cash value exceeds premiums paid (your “basis”), the excess is taxed as ordinary income in the year you surrender.

Policy Rider Options for Both Term and Whole Life

Riders are optional add ons that customize coverage for specific risks or provide financial flexibility. Both term and whole life policies offer riders, though some, especially long term care and chronic illness riders, are more common on permanent policies because they require cash value or extended coverage periods. Riders increase your premium, sometimes by 5 to 25% depending on the benefit, and availability varies by insurer and state. The most valuable riders address real financial risks: disability that stops premium payments, terminal illness that accelerates the death benefit, or catastrophic medical expenses that drain savings before death.

Waiver of premium riders are especially useful on whole life because missing even one premium can cause the policy to lapse or force a loan against cash value to cover the payment. If you become totally disabled (definitions vary, but commonly mean inability to work in your own occupation for at least six months), the insurer waives premiums while you’re disabled, and the policy remains in force with cash value continuing to grow. Accelerated death benefit riders let you access a portion of the death benefit, typically 25 to 100%, if you’re diagnosed with a terminal illness (usually defined as life expectancy of 12 to 24 months or less). The advance reduces the death benefit your beneficiaries receive, but it can cover medical bills, hospice care, or end of life expenses when you need the money most.

Common riders and their functions:

- Waiver of premium — Insurer pays premiums if you become totally disabled; especially important on whole life to prevent lapse.

- Accelerated death benefit — Access 25 to 100% of death benefit early if diagnosed with terminal illness (life expectancy ≤ 12 to 24 months); reduces payout to beneficiaries.

- Long term care (LTC) or chronic illness rider — Pays monthly benefit if you meet LTC triggers (inability to perform two or more activities of daily living); more common on permanent policies; can be costly.

- Accidental death benefit (double indemnity) — Pays an additional death benefit (often double) if death results from accident; limited value because most deaths are from illness, not accident.

Tax Treatment of Term vs Whole Life Benefits and Cash Value

Death benefits paid to named beneficiaries are generally income tax free under federal law, whether the policy is term or whole life. The IRS treats life insurance proceeds as a return of premiums (even though total premiums paid are usually far less than the death benefit), so beneficiaries receive the full face amount without owing income tax. Estate taxes are a different issue: if you own the policy at death, the death benefit is included in your taxable estate, which matters for estates above the federal exemption (roughly $13.6 million per person in 2024, indexed for inflation). To keep the death benefit out of your estate, you can transfer ownership to an irrevocable life insurance trust (ILIT) or another person, but the transfer must occur at least three years before death to avoid IRS inclusion rules.

Whole life’s cash value grows tax deferred, meaning you owe no income tax on the annual credited interest or dividends as long as the money stays inside the policy. If you take a policy loan, the loan itself is not taxed. You’re borrowing your own money. But if the policy lapses with an outstanding loan, the IRS treats the loan as a taxable distribution to the extent it exceeds your cost basis (total premiums paid). That can create a large, unexpected tax bill. Withdrawals from cash value (partial surrenders) are tax free up to your cost basis; amounts above basis are taxed as ordinary income. Full surrenders follow the same rule: you receive the cash surrender value, and any gain over your basis is taxable income in the year you surrender.

| Feature | Term Life | Whole Life |

|---|---|---|

| Death Benefit to Beneficiary | Income tax free | Income tax free |

| Estate Tax Treatment | Included in taxable estate if insured owns policy at death | Included in taxable estate if insured owns policy at death; ILIT ownership can exclude it |

| Cash Value Growth | N/A, no cash value | Tax deferred; no annual tax on credited interest or dividends |

| Loans and Withdrawals | N/A | Loans not taxed if policy remains in force; lapse with unpaid loan triggers tax on gain; withdrawals tax free up to cost basis, then taxed as ordinary income |

Alternatives to Traditional Term and Whole: Universal, Variable, Indexed

Permanent life insurance comes in several flavors beyond traditional whole life, each trading guarantees for flexibility or potential upside. Universal life (UL) unbundles the premium and death benefit: you can adjust premium payments and coverage amounts (within limits), and cash value earns interest tied to current market rates or a declared crediting rate set by the insurer. That flexibility sounds attractive, but if interest rates fall or the insurer lowers the crediting rate, your cash value may grow more slowly than illustrated, and you might need to pay higher premiums later to keep the policy in force. Guaranteed universal life (GUL) strips out most cash value and focuses on providing the lowest cost permanent death benefit. Premiums are higher than term but much lower than whole life, and the policy stays in force as long as you pay the specified premium, making it popular for estate planning when cash value isn’t a priority.

Variable life (VL) and variable universal life (VUL) let you allocate cash value among investment subaccounts, essentially mutual funds inside the policy, offering stock and bond exposure with the potential for higher long term returns than whole life’s guaranteed 1 to 3%. The downside is investment risk: if the subaccounts perform poorly, cash value can shrink or disappear, and you may need to pay additional premiums to prevent the policy from lapsing. Variable policies also carry higher fees. Mortality and expense charges, fund management fees, and administrative loads can total 2 to 3% annually, which drag on long term performance. Indexed universal life (IUL) credits interest based on the performance of a stock market index (commonly the S&P 500), subject to a cap (often 10 to 12%) and a floor (usually 0 to 1%). IUL offers upside participation with downside protection, but caps limit gains in strong market years, and the crediting formula can be complex and opaque.

The four main alternatives and their trade offs:

- Universal life (UL) — Flexible premiums and adjustable death benefit; cash value earns interest at insurer declared rates (historically 3 to 5%, but can fall); lower guarantees than whole life; risk of lapse if crediting rates drop and you don’t increase premiums.

- Guaranteed universal life (GUL) — Minimal cash value, lowest permanent premium; coverage guaranteed as long as you pay the scheduled premium; ideal for estate planning when you need a death benefit but don’t care about cash accumulation.

- Variable life (VL) and variable universal life (VUL) — Cash value invested in subaccounts (stocks, bonds, money market); potential for higher returns but also risk of loss; higher fees (2 to 3% total); requires active management and tolerance for volatility.

- Indexed universal life (IUL) — Cash value growth linked to stock index performance with caps (commonly 10 to 12%) and floors (0 to 1%); upside limited, downside protected; complex crediting methods and potential for lower than expected growth if market returns are concentrated in a few strong years that hit the cap.

Age, Health, and Lifestyle Factors Influencing Your Premiums

Insurers price life insurance by estimating how likely you are to die during the coverage period, so age and health dominate the underwriting equation. A 25 year old non-smoker in excellent health might qualify for “Preferred Plus” rates, the lowest available, while a 55 year old with controlled high blood pressure and a 20 pound weight surplus lands in “Standard” class, paying 30 to 50% more for the same coverage. Smoking status is the single biggest surcharge: smokers typically pay 100 to 200% more than non-smokers, and the surcharge applies whether you smoke cigarettes, cigars, a pipe, or use chewing tobacco. Some insurers also penalize marijuana use, though policies vary. Occasional recreational use might still qualify for non-smoker rates, while daily use often triggers smoker pricing.

The medical exam checks for red flags: elevated blood pressure, high cholesterol, glucose levels indicating prediabetes or diabetes, abnormal liver enzymes (which can signal alcohol abuse or hepatitis), and cotinine (a nicotine metabolite) to verify tobacco use. Insurers also review your prescription history through the Medical Information Bureau (MIB) and pharmacy databases, so undisclosed medications for chronic conditions, antidepressants, statins, blood pressure meds, will surface during underwriting. Body mass index (BMI) matters too: applicants significantly overweight or underweight may be surcharged or declined. Dangerous hobbies like skydiving, scuba diving below recreational depths, rock climbing, piloting small aircraft can trigger exclusions, flat extra charges (a fixed dollar amount per $1,000 of coverage), or outright declines.

Underwriting is stricter and more expensive as you age. A 30 year old applying for $500,000 of term life faces a straightforward exam and quick approval if healthy; a 60 year old applying for the same amount can expect additional tests like EKG, stress test, or cognitive screening, and longer underwriting timelines. Whole life underwriting is equally rigorous, and because the insurer commits to paying a death benefit decades in the future, they scrutinize family history (early heart disease, cancer, or stroke in parents or siblings), occupation (hazardous jobs like logging, roofing, or commercial fishing add risk), and driving record (multiple DUIs or reckless driving convictions can result in declines). If you’re applying in your 40s or later, expect underwriting to dig deep, and be prepared to justify any prescription, past diagnosis, or lifestyle factor that appears in your medical records.

Common FAQs About Term and Whole Life Insurance

Can I convert my term policy to whole life, and how does that work? Most term policies include a conversion option that lets you switch to permanent coverage, usually whole, universal, or guaranteed universal life, without a new medical exam, as long as you convert before a specified age (commonly 60 to 65) or within a set number of years from policy issue. The new permanent premium is based on your age at conversion and the rate class you originally qualified for, so if you were rated Preferred at age 30 and convert at age 50, you pay the Preferred whole life rate for a 50 year old. Conversion preserves insurability if your health has declined, but expect the new premium to be significantly higher than your term premium.

Is whole life a good investment compared to other savings or investment options? Whole life offers tax deferred cash value growth and a guaranteed death benefit, but it rarely matches the long term returns of diversified stock and bond portfolios in taxable or tax advantaged accounts. Guaranteed cash value growth of 1 to 3% plus historical dividends of 0 to 6% typically lags the 7 to 10% average annual return of a low cost index fund over decades. Whole life can be valuable for forced savings discipline, estate planning, or creditor protection (in states that shield cash value), but if your primary goal is wealth accumulation, investing the premium difference in a Roth IRA or 401(k) usually generates higher after tax returns.

What happens if I outlive my term policy? The coverage expires, and you receive nothing. No death benefit, no refund of premiums. You can renew the policy at age based rates, which will be much higher (often double or triple your original premium), or apply for a new term policy, which requires full underwriting and will also be more expensive due to your age. If your term policy includes a conversion feature and you’re still within the conversion window, you can convert to permanent coverage without a medical exam, though the permanent premium will reflect your current age.

How does cash value actually work in a whole life policy? A portion of each premium is allocated to a cash value account that grows at a guaranteed rate (typically 1 to 3% annually) plus potential dividends if the policy is participating. Cash value is yours. You can borrow against it, withdraw a portion, or surrender the policy for the accumulated value. But early cash value is low because much of the first several years’ premiums cover sales commissions and administrative costs. After 10 to 15 years, cash value compounds more noticeably, and by year 20 or 30, it can represent a significant asset you can tap for supplemental retirement income or emergencies.

Can I switch from whole life back to term, and should I? You can surrender your whole life policy, take the cash surrender value (minus any surrender charges), and use the money to buy a new term policy, but you’ll need to pass underwriting for the new term coverage. If your health has declined, you may not qualify for term at all, or you’ll pay higher rates. Surrendering whole life also triggers taxes if your cash value exceeds total premiums paid. A better option is often to keep the whole life death benefit and reduce or eliminate new term purchases, or use a 1035 exchange to move the cash value into a lower cost permanent policy like guaranteed universal life.

Are life insurance death benefits taxed when my beneficiaries receive them? Death benefits are generally income tax free to beneficiaries under federal law. However, if you own the policy at death, the death benefit is included in your taxable estate, which can trigger estate taxes if your total estate exceeds the federal exemption (roughly $13.6 million per person in 2024). To exclude the death benefit from your estate, you can transfer ownership to an irrevocable life insurance trust (ILIT) or another person, but the transfer must occur at least three years before death.

How much do premiums increase if I renew or buy a new policy at an older age? Premiums rise steeply with age because mortality risk increases. A 30 year old paying $30 per month for $500,000 of 20 year term might pay $150 to $300 per month to renew the same coverage at age 50, and $500 to $1,000 per month at age 60. Buying a new term policy at an older age requires underwriting, and any new health conditions will push you into a worse rate class or result in a decline. That’s why convertible term is valuable. It locks in your right to permanent coverage at a set rate class, even if your health deteriorates.

What’s the difference between a policy loan and a withdrawal from cash value? A policy loan is money you borrow from the insurer using your cash value as collateral. You don’t have to repay it, but unpaid loans accrue interest (commonly 4 to 8%) and reduce the death benefit dollar for dollar. Loans are not taxed as long as the policy stays in force, but if the policy lapses with an outstanding loan, the IRS may treat the unpaid amount as taxable income. Withdrawals permanently remove cash from the policy and reduce both cash value and the death benefit; they’re tax free up to your cost basis, then taxed as ordinary income on any gains.

Final Words

You learned the real trade-offs fast: term gives big death benefit for low cost over 10–30 years, whole gives lifetime cover plus slow cash value but costs a lot more.

Watch the fine print. Conversion deadlines, loan interest, surrender charges, and renewal jumps are where people get burned.

Match the choice to your budget and goals. Compare quotes, ask for written answers, and you’ll be ready to choose—term life insurance vs whole life insurance can work for different needs, and you can pick the one that actually protects your family.

FAQ

Q: Which is better life insurance, term life or whole life?

A: The better choice between term life and whole life depends on your goals: term is cheaper and temporary for mortgages or income replacement; whole gives lifetime coverage and cash value but costs much more.

Q: What are the disadvantages of term life insurance?

A: The disadvantages of term life insurance are that coverage expires, there’s no cash value, renewal premiums jump with age, conversion windows can close, and you can be left uninsured if you outlive the term.

Q: Do you get money back at the end of term life insurance?

A: You do not get money back at the end of term life insurance unless you purchased a return-of-premium rider, which increases cost; otherwise premiums are not refunded when the term ends.

Q: How much does a $100,000 whole life insurance policy cost?

A: A $100,000 whole life policy typically costs about $150–$350 per month for a healthy person in their 30s, rising to $400–$1,000+ by age 45, depending on health and the insurer.

{kind=link}