How long does underwriting take for life insurance—days, weeks, or months?

Most applications land in a 2 to 8 week window, but that wide span hides the real drivers: whether you need a medical exam, how fast doctors send records, if the insurer runs extra checks for prescriptions or driving history, and how large or unusual the policy request is.

Read on for a clear timeline, the common gotchas that stretch waits into months, and three practical steps you can take now to speed approval or avoid surprises.

Typical Duration of Life Insurance Underwriting

Standard life insurance underwriting usually takes 2 to 8 weeks from application to final decision. That’s a pretty big range because every case is different. Your path depends on what type of coverage you’re asking for, which underwriting method the carrier uses, and how complicated your health history looks. Someone in great shape applying for a straightforward term policy might wrap up in two weeks. Someone with a chronic condition going for a million‑dollar permanent policy? Two months or longer isn’t unusual.

The 2 to 8 week window covers time for scheduling and finishing a medical exam, pulling records from your doctors, running background checks on prescriptions and driving history, and letting an underwriter review everything before assigning your risk class. Simplified or accelerated programs can shrink that timeline drastically. Some carriers deliver approval in 48 to 72 hours by using electronic data and skipping the in‑person exam. On the flip side, complex cases involving multiple physicians, foreign medical records, high coverage amounts, or unclear test results can push past eight weeks. Sometimes into several months.

The most important thing? “How long” isn’t fixed. Underwriting speed depends on how quickly third parties respond (doctors’ offices releasing records, lab companies processing blood work, the paramedical examiner scheduling your appointment), how complete and accurate your application is, and whether the underwriter needs to ask follow‑up questions or request additional documentation. A clean application with electronic health records and a cooperative physician can move through final review in days once all data arrives. An incomplete form or a hard‑to‑reach specialist can stall things for weeks.

Key Factors That Influence Underwriting Speed

Medical exams are one of the largest variables. If your application requires a paramedical exam (blood draw, urine sample, basic vitals, short health questionnaire), you’ll first need to schedule an appointment with the examiner, which typically happens within 3 to 14 days of your application. The exam itself takes 20 to 60 minutes, then the lab processes your samples over the next 24 to 72 hours. Add it all up and the exam stage alone commonly eats 1 to 3 weeks. Accelerated and simplified policies often skip this step entirely, which is why they can deliver decisions in days instead of weeks.

Physician records (formally called Attending Physician Statements or APS) are the second most common source of delay. When your medical history includes chronic conditions like diabetes, heart disease, high blood pressure, or a recent hospitalization, underwriters request detailed notes and test results directly from your doctors. Most doctors’ offices take 2 to 6 weeks to pull charts, complete forms, and fax or mail records to the insurer. If you see multiple specialists, the insurer may need to collect records from each one. Foreign medical records, older paper files, or busy practices can push this timeline past two months. Because underwriters can’t finalize a decision until they review all requested records, APS retrieval often becomes the longest single stage in the entire process.

Application accuracy and completeness also play a major role. When you leave questions blank, provide vague answers about medication names or dosages, or fail to list all your physicians, the underwriting team has to stop and reach out for clarification. Every round‑trip of questions and answers adds days. Similarly, lifestyle disclosures matter. If you participate in high‑risk hobbies like skydiving or scuba diving, work in a hazardous occupation, or have a complex financial situation (for example, business owners applying for key‑person insurance), the underwriter may need to request additional statements, occupational details, or financial documentation. Each extra document request extends the clock.

Common causes of underwriting delays include:

- Scheduling conflicts or cancellations for the paramedical exam

- Slow response from physicians’ offices when releasing medical records

- Discrepancies between your application answers and data found in prescription‑history databases or the Medical Information Bureau

- High face amounts (policies over $1 million) that trigger reinsurance review or additional financial underwriting

- Incomplete applications missing signatures, beneficiary designations, or required health details

Step‑by‑Step Breakdown of the Underwriting Process

The underwriting process unfolds in a series of distinct stages, each contributing time to the overall timeline. Understanding what happens at each step helps you see where delays are most likely and what you can do to keep things moving.

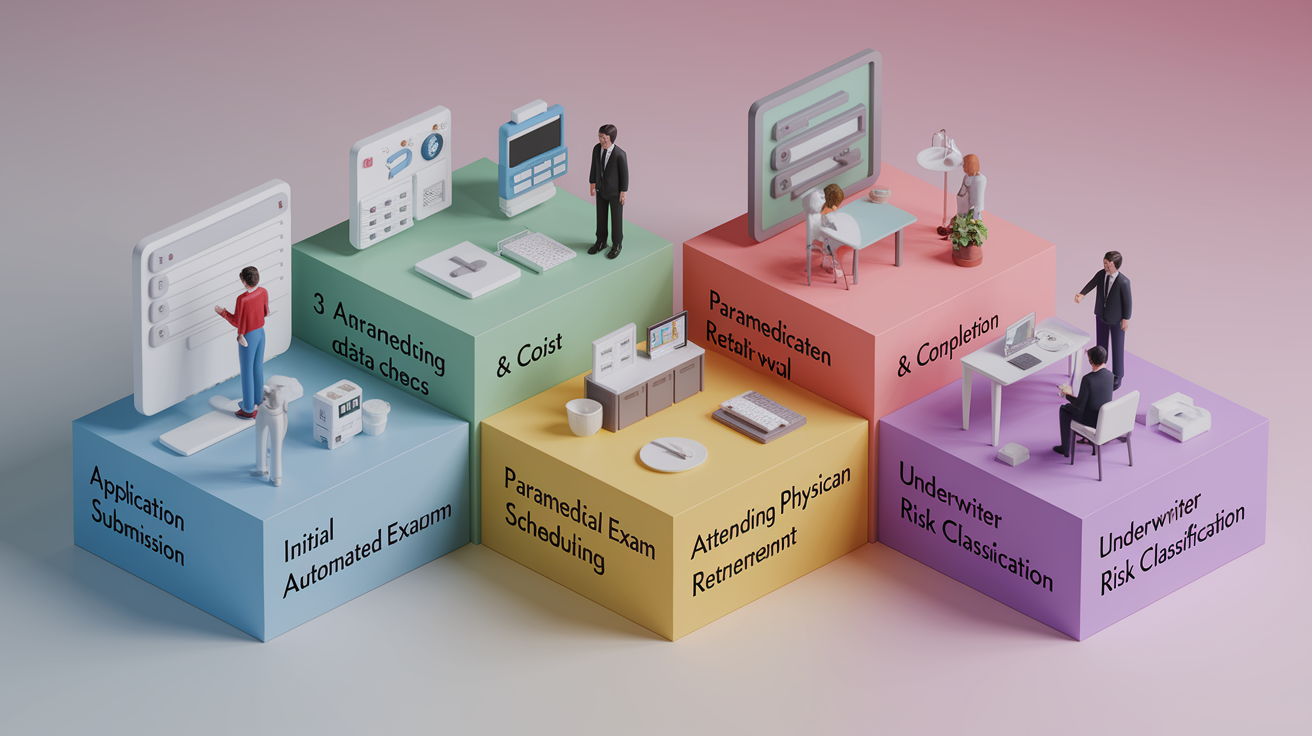

Application Submission and Intake

You begin by completing the application, either online with an electronic signature or on paper through an agent. The insurer’s intake team logs your application, confirms that required fields are filled out, and assigns your case to an underwriter. This stage typically takes the same day to three business days. Many carriers now offer instant electronic submission, which moves your file into underwriting review within minutes. Paper applications mailed to the home office can add several days for delivery and data entry.

Initial Automated Data Checks

Once your application is in the system, underwriters run automated checks against several databases: the Medical Information Bureau (a shared industry database of prior insurance applications and certain medical conditions), prescription‑history vendors that show filled medications over the past several years, motor‑vehicle records to check for DUIs or serious violations, and sometimes credit reports for financial underwriting on high face amounts. These checks usually complete within minutes to 72 hours. If the data comes back clean and matches your application answers, the process moves forward quickly. If the system flags a discrepancy (say, a prescription you didn’t mention or an MIB code that suggests a past health issue), the underwriter will pause to investigate and may contact you for clarification.

Paramedical Exam Scheduling and Completion

For traditional fully underwritten policies, the next step is scheduling your medical exam. The insurer contracts with a paramedical service that calls or emails you to arrange a convenient time and location, often at your home or workplace. Scheduling commonly takes 3 to 14 days depending on your availability and the examiner’s calendar. The exam itself (measuring height, weight, blood pressure, pulse, drawing blood, collecting a urine sample, and asking a series of health questions) takes 20 to 60 minutes. After the exam, the paramedical company ships samples to a lab, which processes the blood and urine panels and sends results to the insurer within 24 to 72 hours. From the moment you’re contacted to schedule until lab results reach the underwriter, this stage typically spans 1 to 3 weeks.

Attending Physician Statement Retrieval

If your application or exam results reveal a chronic illness, recent surgery, abnormal lab values, or any red‑flag condition, the underwriter sends a records request to one or more of your treating physicians. The doctor’s office must locate your chart, copy relevant visit notes and test results, complete an APS form detailing diagnosis and prognosis, and return everything to the insurer by fax, mail, or secure upload. This process usually takes 2 to 6 weeks, but can stretch to 8 weeks or longer if the practice is backlogged, if records are stored offsite or overseas, or if the office requires multiple follow‑up calls. Because underwriters wait for all requested APS documents before making a final decision, this stage is the most common reason applications exceed the typical 2 to 8 week window.

Underwriter Review and Risk Classification

Once the underwriter has your application, exam results, automated data‑check reports, and any physician records, they review everything to assign a risk class: preferred plus, preferred, standard, or substandard (rated). During this review, the underwriter compares your health profile against the insurer’s underwriting guidelines and actuarial tables, checks for consistency across all documents, and decides whether your case fits within standard appetite or needs reinsurance approval (common for face amounts above $1 million or unusual risk factors). This review stage typically takes 3 to 10 business days after all records are received. Complex cases (multiple chronic conditions, borderline lab values, or occupation hazards) may require consultation with a medical director or reinsurer, adding another week or more.

Final Decision and Policy Issuance

After the underwriter reaches a decision, the insurer generates an approval notice (or a decline or counteroffer with higher premiums). If approved, the company issues the policy document and mails or emails it to you or your agent. Policy issuance usually takes 3 to 7 business days after approval. Your coverage effective date is often set on the approval date or on a requested backdated effective date if state law allows. If the underwriter offers a rating (substandard approval with extra premium), you have the option to accept, decline, or negotiate by providing additional medical evidence.

Ways Applicants Can Speed Up the Underwriting Process

The single most effective way to shorten underwriting time is to choose an accelerated or simplified‑issue product if you qualify. Accelerated underwriting programs use algorithms and electronic data to deliver decisions in minutes to 72 hours without requiring a medical exam. Simplified‑issue policies ask a short health questionnaire and issue coverage within days to two weeks. Both skip the exam‑scheduling delay and the wait for lab results. If you’re young, healthy, and applying for a moderate face amount, these options can cut weeks off the timeline while still providing solid coverage.

Completing your application fully and accurately is the second‑biggest time‑saver. Provide complete names, addresses, and phone numbers for every doctor you’ve seen in the past five years. List all medications with correct dosages and the conditions they treat. Answer health questions truthfully and in detail. Vague answers like “I think I had high cholesterol a few years ago” force underwriters to dig for records. Use electronic signatures when available. Paper forms add mailing time and data‑entry delays. Double‑check that you’ve signed every required page and designated beneficiaries clearly.

Six practical steps to minimize delays:

- Schedule the paramedical exam immediately when the examiner contacts you, and choose a morning appointment if possible so samples reach the lab the same day.

- Authorize medical‑records release up front and call your doctors’ offices directly to let them know the insurer will be requesting records. Ask the office staff to prioritize the request.

- Respond to underwriter questions within 24 to 72 hours. Keep your phone and email accessible and check messages daily during the underwriting period.

- Provide recent test results if you already have blood work, EKGs, or other diagnostics from a recent physical. Sending these proactively can sometimes eliminate the need for additional testing.

- Consent to electronic data checks for prescription history and MIB records to reduce the number of manual record requests.

- Avoid starting new medications, scheduling elective surgeries, or taking up high‑risk hobbies while underwriting is in progress. Any new health event or risk factor can trigger additional questions and delay the decision.

What to Expect While Waiting for an Underwriting Decision

Most insurers and agents provide periodic status updates during underwriting, especially if the process stretches beyond a few weeks. You may receive an email or phone call confirming that your exam is complete, that records have been requested from your physician, or that your file is in final review. If you don’t hear anything for two weeks after submitting a traditional application, it’s reasonable to contact your agent or the insurer’s customer‑service line to ask for a status update. For accelerated or simplified applications, follow up after 48 to 72 hours if you haven’t received a decision.

Requests for additional information are common and not a sign that your application is in trouble. Underwriters routinely ask clarifying questions about medication changes, the outcome of a past surgery, details about a family‑history item, or confirmation of a current health measurement. When you receive one of these requests, respond as quickly as possible with specific, documented answers. If the underwriter asks for a letter from your doctor explaining a diagnosis or recent test result, contact the physician’s office the same day and ask them to prioritize the letter. Delays in responding to these requests are one of the easiest ways to add weeks to your timeline.

If several weeks pass without communication and you’re approaching or exceeding the typical 2 to 8 week window, escalate your follow‑up. Ask your agent to contact the underwriting department directly, request a timeline for outstanding items (such as pending APS or reinsurance review), and confirm that no additional documents are needed from you. Proactive follow‑up won’t necessarily speed the insurer’s internal processes, but it does ensure that your case isn’t stalled due to a missing signature, an overlooked records request, or a clerical error.

Final Words

We laid out the usual 2–8 week window for life insurance underwriting and explained why the timeline varies.

You saw the key stages—application review, medical exam, records checks—and the common delay points.

We gave practical steps to speed things up: fill forms correctly, schedule exams quickly, and push for doctor responses.

If you’re asking how long does underwriting take for life insurance, plan for 2–8 weeks but expect exceptions. Be proactive and you’ll usually get a decision sooner and avoid surprises.

FAQ

Q: Can I get life insurance with HPV?

A: Having HPV does not automatically bar you from getting life insurance. Insurers mainly care about cancer or serious cervical changes; routine HPV usually has little effect. Disclose history and expect normal offers unless complications exist.

Q: What are red flags for underwriters?

A: Red flags for underwriters include undisclosed risky activities, recent or serious illnesses (like cancer), substance misuse, inconsistent application answers, dangerous jobs, and extreme health measures; they lead to delays, higher premiums, or denial.

Q: Does life insurance pay for suicidal death in Louisiana?

A: Life insurance in Louisiana typically follows the policy’s suicide clause: deaths by suicide within the usual two-year contestability/exclusion period are often denied, while suicides after that period are generally paid; always check your policy.

Q: Can a person with dementia get life insurance?

A: A person with dementia usually has limited options: active dementia often leads to denial for standard coverage, but early-stage applicants may still qualify, or they can get guaranteed-issue or final-expense plans at higher cost.

{kind=link}