Think your Etsy shop is too small to get sued? Think again.

Etsy lets you sell without proof of insurance, but that doesn’t mean you’re covered.

Product liability claims can cost millions, the average settlement is about $7.6 million, and your homeowners policy usually won’t help.

This post lays out the coverages Etsy sellers actually need — general liability, product liability, property, cyber, and when an umbrella matters — plus real cost examples and the red flags to check before you buy.

Essential Insurance Guidance for Etsy Sellers

Etsy doesn’t require sellers to carry business insurance to open or operate a shop. You can list products, process sales, and run a handmade business without ever showing proof of coverage. But here’s the thing: Etsy strongly recommends sellers protect themselves with their own insurance, and there’s a good reason for that. The platform’s Seller Protection Policy doesn’t cover product liability, customer injuries, or damage claims that come from the items you make and sell.

A lot of Etsy sellers think their homeowners or renters insurance will step in if something goes wrong. It won’t. Personal policies almost always exclude business related claims. If a customer gets injured by your product or accuses you of copyright infringement in your product photos, your home policy will probably deny the claim. The Insurance Information Institute puts the average product liability claim settlement at $7.6 million. Even one lawsuit over a defective candle, an allergic reaction to skincare, or a choking hazard in a children’s toy can wipe out years of profit and personal savings if you’re uninsured.

The risks Etsy sellers face depend on what they make, where they store inventory, and how they market products. Handmade businesses are small, but the legal exposure is the same as any other manufacturer or retailer. Essential coverage types include general liability insurance (for customer injuries and property damage), product liability insurance (for defects, design flaws, or failure to warn), and business property insurance (for tools, materials, and finished inventory). Sellers who handle customer payment data or run their own website should also think about cyber liability insurance. Those offering design consultations or custom services may need professional liability coverage for negligence claims.

Common risks Etsy sellers face:

- Product defects causing bodily injury (burns from candles, skin reactions from cosmetics, choking hazards in toys)

- Property damage to a customer’s home or belongings (staining furniture, damaging walls, ruining clothing)

- Advertising injury claims (copyright or trademark infringement in photos, descriptions, or branding)

- Fire, theft, or water damage destroying inventory, equipment, or craft supplies stored at home

- Data breaches or payment fraud exposing customer credit card information or personal details

- Customer lawsuits over failed custom orders, missed deadlines, or unmet design expectations

Types of Insurance for Etsy Sellers

Every Etsy seller’s risk profile is different, but a handful of insurance policies cover the majority of handmade business exposures. The policies below protect against financial loss from lawsuits, property damage, cyberattacks, and product defects. Most small sellers start with one or two core policies and add coverage as revenue and complexity grow.

Product Liability Insurance

Product liability insurance covers legal claims and damages when something you made or sold injures someone or damages their property. This includes manufacturing defects (a cracked ceramic mug that cuts a hand), design flaws (a necklace clasp that fails and causes injury), and failure to provide adequate instructions or warnings (a cleaning product without hazard labels). Product liability is often bundled into a general liability policy under “products and completed operations” coverage. Higher risk sellers, those making food, cosmetics, children’s items, or anything that touches skin, should verify the coverage is explicitly included and consider a standalone product liability policy for higher limits.

Product liability insurance pays for legal defense costs, settlements, and judgments up to your policy limit, typically starting at $1,000,000 per occurrence. Without it, you’re personally responsible for every dollar. For example, if a customer’s child is injured by a small part that breaks off a handmade toy, the medical bills, legal fees, and potential settlement could easily exceed $100,000. Even if the lawsuit is baseless, defending yourself in court costs tens of thousands of dollars. Product liability insurance handles both the defense and any damages awarded.

General Liability Insurance

General liability insurance is the foundation policy for nearly every small business. It covers third party bodily injury (a customer trips over a display at a craft fair and breaks an arm), third party property damage (you accidentally spill dye on a venue’s carpet during setup), and personal and advertising injury (a competitor sues you for using their copyrighted image in a product listing). For Etsy sellers, general liability is essential even if you work from home and never meet customers face to face, because it also protects against claims arising from your marketing, packaging, and shipping activities.

A standard general liability policy for a small Etsy business costs a median of $850 per year and typically provides $1,000,000 per occurrence with a $2,000,000 aggregate limit. The “occurrence” limit is the maximum the insurer will pay for a single incident. The “aggregate” is the total the policy will pay across all claims during the policy period. If you participate in craft fairs, farmers markets, or pop up events, general liability is non negotiable. Most event organizers require proof of at least $1,000,000 in coverage before allowing vendors to set up.

Business Property Insurance

Business property insurance covers the physical assets you use to run your Etsy shop. Tools, equipment, raw materials, finished inventory, and sometimes the workspace itself if you rent a studio. This policy protects against fire, theft, water damage, vandalism, and certain natural disasters. If your sewing machines, jewelry making tools, or boxes of finished products are destroyed in a house fire, business property insurance reimburses you for the replacement cost. You can rebuild inventory and resume operations without draining personal savings.

Homeowners and renters insurance specifically exclude business property and inventory, so you can’t rely on your personal policy if you store products or materials at home. For example, if you keep $5,000 worth of finished candles and supplies in your basement and a pipe bursts, your homeowner’s policy will deny the claim because the items were held for sale. Business property insurance fills that gap. Many Etsy sellers bundle this coverage into a Business Owner’s Policy (BOP), which combines general liability and property insurance at a lower cost than buying each separately. Median cost for a BOP is around $2,000 per year.

Cyber Liability Insurance

Cyber liability insurance protects your business if customer payment data is stolen, your website is hacked, or you’re hit with ransomware. Even if you use Etsy’s payment processing and never touch a credit card number yourself, your business can still be liable if customer information stored in spreadsheets, email, or third party tools is breached. Cyber policies typically cover notification costs (you must inform affected customers), legal fees, credit monitoring services for customers, regulatory fines, and the cost to restore data or rebuild your website after an attack.

For small online retailers, median cyber insurance runs about $1,500 per year. The policy also covers your own business interruption. If a hacker takes down your Etsy shop or website and you lose sales during recovery, cyber liability insurance can reimburse lost income. This coverage is especially important for sellers who maintain their own e-commerce site alongside their Etsy shop or who store customer order histories and contact lists for email marketing. One phishing attack that compromises a spreadsheet of customer emails can trigger notification requirements under state data breach laws. Handling that without insurance can cost thousands in legal and administrative fees.

Commercial Umbrella Insurance

Commercial umbrella insurance adds an extra layer of liability protection above your general liability and product liability policies. It kicks in once you exhaust the limits on your underlying policies. For example, if you carry $1,000,000 in general liability and face a $1,500,000 judgment, your umbrella policy pays the additional $500,000. Umbrella policies are sold in $1,000,000 increments and typically cost $150 to $400 per year for the first million dollars of coverage.

Most Etsy sellers don’t need umbrella coverage at launch, but it becomes important as revenue grows or if you sell higher risk products. If your annual sales exceed $250,000, you sell items that pose bodily injury risk (candles, skincare, children’s products), or you frequently participate in large public events, an umbrella policy offers peace of mind at a relatively low cost. It’s cheaper to add $1,000,000 or $2,000,000 of umbrella coverage than to increase the limits on every underlying policy individually.

Insurance Costs for Etsy Sellers

Small business insurance for handmade sellers typically ranges from $25 to $70 per month, or roughly $300 to $850 per year, for basic general liability coverage. A seller making low risk items like art prints or digital downloads will pay closer to the low end. Someone crafting skincare, food products, or children’s toys will see premiums climb toward $1,000 to $3,000 annually. Adding product liability, business property, or cyber coverage pushes total annual costs higher. Expect to budget $500 to $1,500 per year for a bundled Business Owner’s Policy that includes general liability and property protection for inventory and tools.

What you pay depends on several factors beyond just the type of coverage you buy. Insurers evaluate your revenue, the nature of your products, where you operate, your claims history, and whether you have employees. A seller with $100,000 in annual revenue making jewelry can expect to pay $400 to $800 per year for $1,000,000/$2,000,000 general liability. But a seller with the same revenue making bath bombs or candles might pay $1,200 to $2,000 because the product risk is higher. If your revenue climbs to $500,000, premiums typically rise proportionally. Plan on $1,500 to $3,000 or more per year for comprehensive coverage.

Factors that increase your insurance premium:

- Selling consumables, skincare, or children’s products (higher injury and liability risk)

- Hiring employees (triggers mandatory workers’ compensation in most states, raising total cost)

- High sales volume or rapid revenue growth (larger revenue base increases exposure)

- Operating from a commercial space instead of home (commercial property premiums exceed home based coverage)

- Prior claims history or lawsuits (even denied claims signal risk to underwriters and push rates up)

| Insurance Type | Typical Monthly Cost |

|---|---|

| General Liability (GL) Only | $25 – $85 |

| Product Liability (Standalone or Add-On) | $35 – $125 |

| Business Owner’s Policy (BOP: GL + Property) | $40 – $125 |

| Cyber Liability Insurance | $25 – $100 |

Best Insurance Providers for Etsy Sellers

Choosing an insurer comes down to how they handle small craft businesses, how fast you can get a quote, and whether they make it easy to get proof of coverage when event organizers or marketplaces ask for it. Some carriers specialize in online sellers and handmade businesses, offering instant quotes and flexible monthly billing. Others provide broader small business policies through local agents. Below are some of the top options for Etsy sellers, each with different strengths depending on your product type, coverage needs, and budget.

| Provider | Best For | Key Features | Typical Cost Range |

|---|---|---|---|

| Next Insurance | Fast online quotes, event vendors | Instant certificates of insurance, monthly billing, tailored for craft and handmade sellers | $20 – $60/month |

| Thimble | Short-term and event coverage | Coverage sold by the day, month, or year; popular with craft-fair vendors and seasonal sellers | $5/day to $50/month |

| Hiscox | Professional liability and higher limits | Easy online quotes, strong professional liability options for custom design work | $30 – $80/month |

| The Hartford | Bundled BOP and workers’ comp | Comprehensive small-business policies, agent support, established carrier with high financial ratings | $40 – $100/month |

| State Farm | Local agent access, home-based sellers | Business endorsements for home-based operations, bundling with personal policies for discounts | $25 – $70/month |

Digital first carriers like Next Insurance and Thimble make it simple to buy coverage in minutes and download unlimited certificates of insurance. That’s critical if you sell at multiple events per year or if a marketplace asks for proof. Traditional insurers like The Hartford and State Farm offer more hand holding through local agents and may provide better bundling discounts if you already carry personal auto or home insurance with them. Hiscox stands out for sellers offering custom services or design consultations, because their professional liability coverage is easy to add and competitively priced for small businesses.

How to Choose the Right Insurance for Your Etsy Business

Start by evaluating the specific risks your products create. A seller making downloadable art templates faces almost zero product liability risk. Someone hand pouring soy candles or formulating lotions carries significant exposure to burns, allergic reactions, and fire hazards. Product type is the single biggest factor in determining what coverage you need and how much it’ll cost. Higher risk products (anything consumable, flammable, used on skin, or designed for children) require product liability insurance at a minimum. They often justify higher limits or additional endorsements like product recall coverage.

Sales volume and growth trajectory also matter. If you’re clearing less than $10,000 per year and making low risk goods, a basic general liability policy may be enough to start. Once you hit $50,000 to $100,000 in annual revenue or begin hiring help (even part time contractors), you should add business property coverage for inventory and consider workers’ compensation if your state requires it for employees. If you sell on platforms beyond Etsy, especially Amazon or Walmart, which impose specific insurance requirements once you exceed monthly sales thresholds, check those marketplace rules early and make sure your policy meets their minimum liability limits.

Where you operate and ship also influences your insurance needs. Sellers who work exclusively from home and ship via USPS or commercial carriers can often skip commercial auto insurance. But if you regularly drive to craft fairs, supplier warehouses, or shipping hubs, your personal auto policy likely excludes business use and you’ll need a commercial auto endorsement. Similarly, if you store inventory in a rented warehouse or third party fulfillment center, you’ll need inland marine or transit coverage to protect goods while they’re off premises. Standard business property policies only cover items at your listed business address.

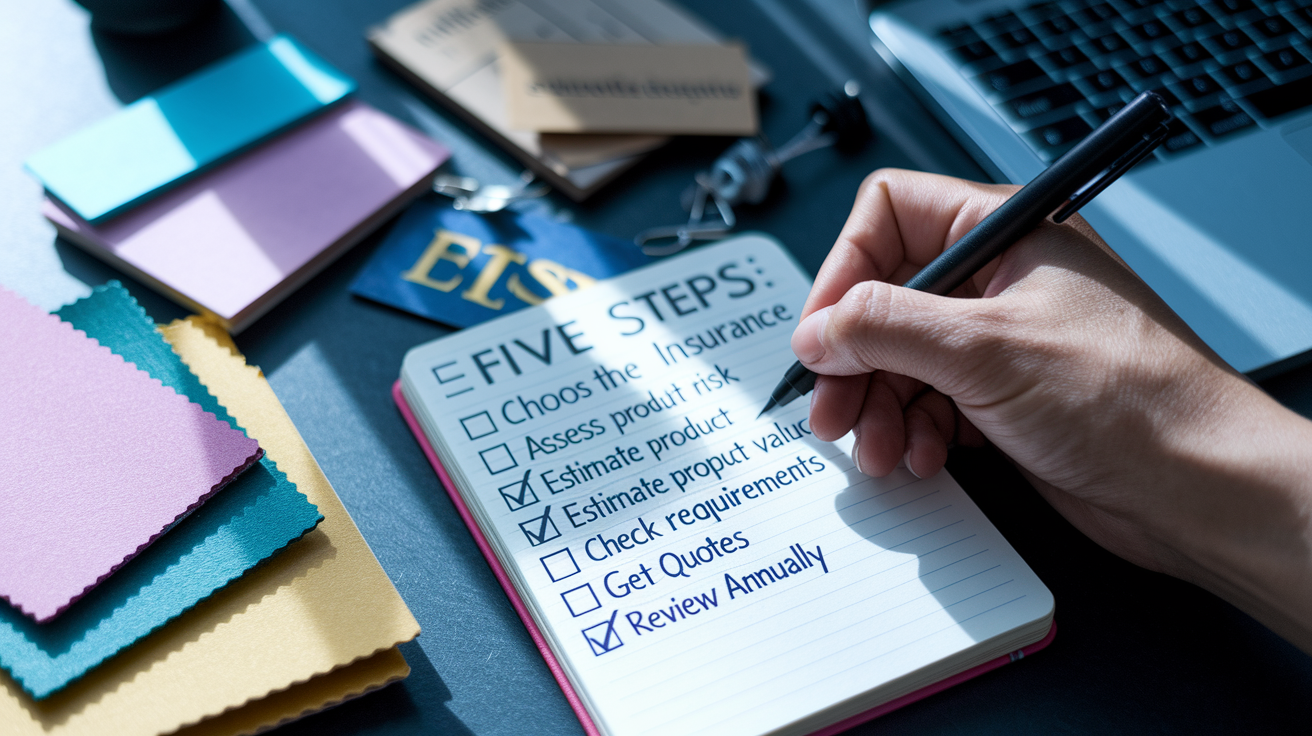

Five steps to choose the right insurance for your Etsy shop:

- Assess your product risk. List everything you make and sell. Flag items that are consumable, flammable, worn on the body, or intended for children. If any flagged items exist, product liability is mandatory.

- Estimate your total business property value. Add up the replacement cost of tools, equipment, raw materials, and finished inventory. If the total exceeds $5,000, buy business property coverage or a BOP.

- Check state and marketplace requirements. Verify whether your state requires workers’ compensation if you have employees, and confirm any insurance mandates from platforms where you sell (Amazon, Walmart, or large event organizers).

- Get quotes from at least three providers. Compare not just price, but policy limits, coverage exclusions, ease of getting certificates of insurance, and customer service accessibility (online chat, phone support, agent access).

- Review and update annually. Reassess coverage every year or after major business changes. Hiring your first employee, adding a new high risk product line, moving into a commercial space, or crossing $100,000 in revenue all justify increasing limits or adding policies.

Final Words

You now know Etsy doesn’t require insurance, but sellers still face product defects, customer injury, damaged inventory, and copyright claims. General, product, property, cyber, and umbrella policies each cover different gaps.

We covered typical costs, top providers, and a clear way to pick coverage. Watch exclusions, limits, and whether a policy covers home-based or shipped goods.

Treat small business insurance for etsy sellers as protection, not optional. Get quotes, compare limits and exclusions, and pick the plan that matches your risks — you’ll be ready if a claim shows up.

FAQ

Q: Do I need business insurance for an Etsy shop? What insurance do you need to sell on Etsy?

A: You don’t legally need business insurance for an Etsy shop, but you should carry it—at least general and product liability. Add business property or professional coverage if you store inventory or sell higher-risk goods.

Q: How much does a $1,000,000 liability insurance policy cost?

A: A $1,000,000 liability policy for small handmade sellers typically runs about $25–$70 per month (roughly $300–$850 a year), depending on product risk, sales volume, and your claims history.

Q: Does Etsy have insurance for sellers?

A: Etsy does not provide insurance for sellers; its Seller Protection program is not a substitute. Buy your own liability and property coverage, and get written confirmation of limits before selling risky items.

{kind=link}