Think your insurance will always pay after a loss? Think again.

An insurance policy exclusion is the clause that removes coverage for specific risks, meaning the insurer can legally say no even when the rest of the policy looks broad.

This post breaks down what an insurance policy exclusion is, common exclusions you’ll actually run into (flood, mold, intentional damage, cyber), where to find them in your policy, and the simple checks to avoid costly surprises at claim time.

Clear Breakdown of Insurance Policy Exclusions and What They Mean

An insurance policy exclusion is contract language that removes coverage for specific losses, perils, or situations. If a claim involves an excluded risk, the insurer won’t pay, even if the event otherwise falls under the policy’s broad coverage promise. Exclusions create legally binding gaps in protection. They can eliminate coverage entirely for certain claims.

Insurers use exclusions to control risk exposure and keep premiums manageable. Without them, policies would need to cover every conceivable disaster, and premiums would become unaffordable for most buyers. Policies are structured in layers: first, an insuring agreement states what’s broadly covered (for example, “we cover physical damage to your home”). Then a list of exclusions follows, narrowing that broad promise by carving out specific risks the insurer won’t pay for.

Common examples include flood damage, earthquake, intentional damage (like arson you cause yourself), pollution or contamination cleanup, and cyber attacks or data breaches. These exclusions matter because they define the moment an insurer can legally say no, and when you become personally liable for the full cost of a loss. For instance, a hazardous waste exclusion may be irrelevant for a law firm but would eliminate coverage entirely for a medical clinic handling x-rays, CT scans, and MRIs.

How Insurance Policy Exclusions Are Structured and Where to Find Them

Exclusions typically appear in a dedicated section of the policy labeled “Exclusions” or “What Is Not Covered.” You’ll also find exclusion language embedded in endorsements, definitions, and conditions clauses. Most policies follow a predictable structure: insuring agreement (what’s covered), then exclusions (what’s carved out), followed by conditions (rules for maintaining coverage) and endorsements (add ons or modifications).

Endorsements are especially important because they can either restore coverage for an excluded risk or introduce brand new exclusions. Always read the full endorsement text, not just the title.

When scanning a policy for exclusions, look for these six signals:

- Phrases like “we will not cover,” “excluded,” or “does not apply to.”

- Named perils listed after words like “except” or “but not for.”

- Conditional language such as “coverage does not apply if,” “unless,” or “only when.”

- Bolded, capitalized, or boxed text highlighting excluded risks.

- Cross references to definitions that limit or remove coverage (for example, “See ‘Flood,’ excluded under Section II”).

- Separate exclusion endorsements attached to the main policy document.

Common Insurance Exclusions and Real World Examples

Exclusions vary by policy type and insurer, but certain exclusions appear across almost every personal and commercial policy. Recognizing them helps you identify coverage gaps before a claim happens.

Auto Exclusion Examples

Most auto policies exclude coverage when you use your car for business purposes like rideshare driving (Uber, Lyft), delivery work (pizza, food, flowers), or any commercial activity not disclosed at purchase. Policies also exclude unnamed drivers, vehicles not listed on the declarations page, and specialty vehicles like motorcycles, golf carts, or ATVs. Some policies include “Acts of God” exclusions that deny coverage for crashes caused by sudden medical events, like a heart attack or stroke behind the wheel.

Homeowners Exclusion Examples

Homeowners policies routinely exclude the following risks:

Flood damage from rising water, storm surge, or overflowing bodies of water. Long term water leakage or slow seepage that occurs over weeks or months. Mold growth, especially when caused by unaddressed moisture or maintenance neglect. Damage from settling, shifting, or expanding soil. Claims arising from faulty construction, poor workmanship, or defective materials.

Some insurers also exclude liability for injuries caused by specific dog breeds or exotic pets, leaving owners personally liable for bite or attack claims.

Health & Liability Exclusion Examples

Health insurance policies often exclude coverage for pre-existing conditions, medical issues diagnosed or treated before your policy start date. Commercial liability policies typically exclude pollution or contamination cleanup, intentional acts (like assault or fraud), and hazardous waste handling. Cyber liability exclusions are standard on general liability policies, meaning data breaches, ransomware attacks, and system failures require separate cyber insurance.

These exclusions exist because the risks are either predictable, controllable by the policyholder, or so catastrophic that insurers can’t reliably price them into standard coverage.

Why Insurance Policies Use Exclusions and Their Impact on Coverage and Long Term Protection

Insurers draft exclusions to limit exposure to unpredictable or uninsurable risks. Underwriters use exclusions to keep premiums affordable by removing perils that would require massive reserves or create pricing volatility. Exclusions also reduce moral hazard, the risk that policyholders might act carelessly or even cause losses intentionally if every possible event were covered.

Removing an exclusion or buying back coverage through an endorsement raises your premium because the insurer must now price in the additional risk. For example, adding earthquake coverage to a California homeowners policy can increase your annual premium by hundreds of dollars. The insurer is no longer excluding a high severity, low frequency peril, so the cost of coverage goes up to reflect the new exposure.

Exclusions shape real world claim outcomes in immediate, concrete ways. If your basement floods and your policy excludes flood, you receive zero payment, even if the rest of your home suffered covered wind damage in the same storm. If your business suffers a ransomware attack and your general liability policy excludes cyber losses, you pay for forensic investigation, legal fees, notification costs, and regulatory fines out of pocket. The exclusion eliminates recovery entirely. There’s no partial payment or negotiation.

Over the long term, unaddressed exclusions create substantial financial exposure. Major perils like flood, mold, earthquake, cyber attack, and pollution can produce six or seven figure losses. Without separate coverage or endorsements, a single excluded claim can wipe out savings, force asset liquidation, or trigger bankruptcy.

| Term | What It Means |

|---|---|

| Exclusion | Removes coverage entirely for a named risk; insurer will not pay if the exclusion applies. |

| Limitation | Restricts coverage through caps, sublimits, time conditions, or higher deductibles; some payment may still occur. |

| Covered Peril | A risk explicitly included in the policy’s insuring agreement; insurer must pay if this peril causes a loss. |

Policy Exclusions vs Policy Limitations: How to Tell the Difference

Exclusions eliminate coverage for specified risks. If a loss falls under an exclusion, the insurer pays nothing. Limitations, on the other hand, modify coverage by imposing caps, sublimits, waiting periods, higher deductibles, or conditional requirements. A limitation may reduce what you recover, but it doesn’t deny the claim outright.

For example, a flood exclusion means zero payment for flood damage. A mold limitation might cap mold remediation at 10,000 dollars, even if actual damage costs 50,000 dollars. Both create out of pocket exposure, but the exclusion is absolute while the limitation allows partial recovery.

Here’s how to distinguish them:

Exclusions use language like “we do not cover,” “excluded,” or “this policy does not apply to.” Limitations use phrases like “coverage is limited to,” “maximum payment,” “sublimit,” or “subject to a separate deductible.” Exclusions often appear in a dedicated section or bolded clause. Limitations are usually embedded in coverage descriptions, special limits schedules, or conditions sections.

How to Review Your Policy for Exclusions Before You Buy

Reviewing exclusions before you purchase a policy is the most effective way to avoid claim time surprises. Exclusions define where your coverage stops, and identifying them early gives you time to request endorsements, buy separate policies, or walk away from inadequate coverage.

Follow these eight steps:

- Request the full policy form and all endorsements in writing, not just a quote summary or declarations page.

- Locate the Exclusions section and read every line. Don’t skim or assume standard language.

- Cross check the Declarations page for endorsements or riders that add or remove exclusions.

- Review the Definitions section for capitalized terms that limit coverage scope (for example, “Flood” may be defined narrowly to exclude certain water damage).

- Identify high risk exclusions relevant to your property, business, or activity: flood, earthquake, mold, cyber, pollution, intentional acts.

- Ask your agent or broker to explain any exclusion you don’t understand. Request written clarification.

- Compare exclusion lists across competing policies. Some insurers exclude fewer perils or offer broader exceptions.

- Evaluate whether you need endorsements, separate policies (like flood or cyber insurance), or umbrella coverage to close gaps.

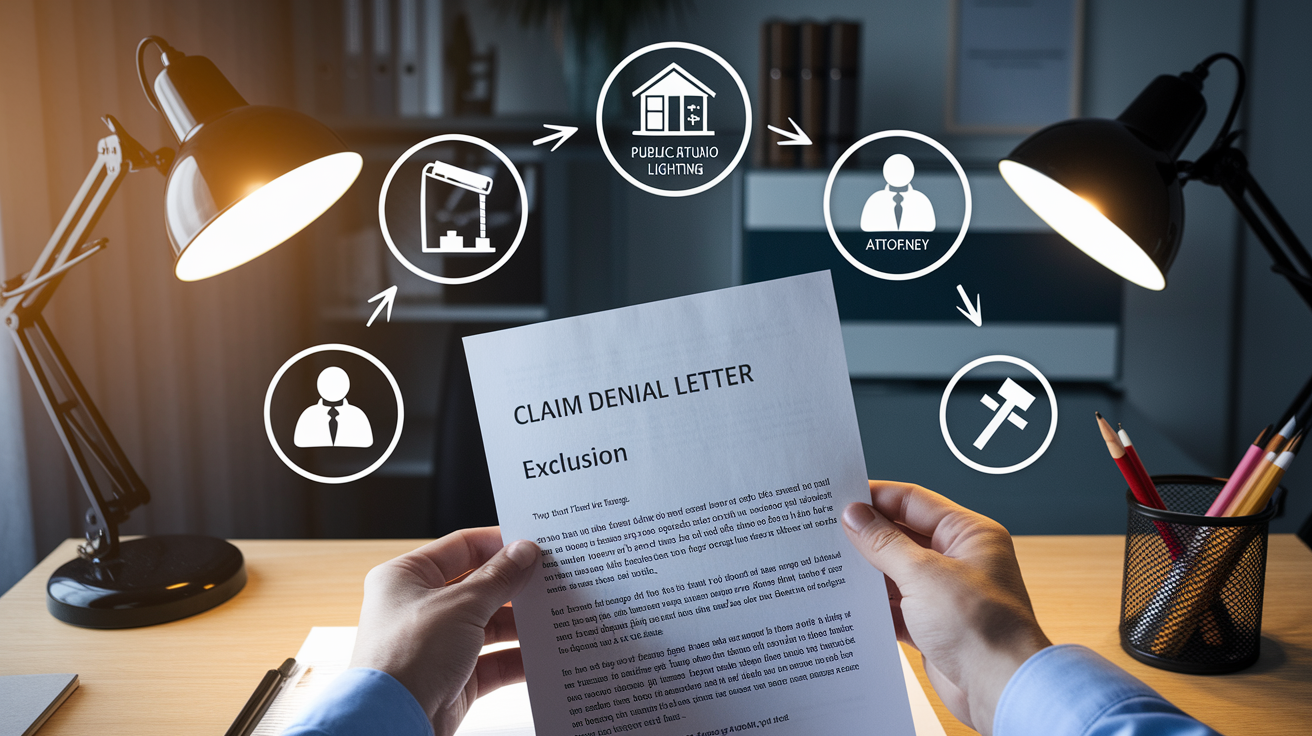

When an Insurance Exclusion Leads to Claim Denial: What to Do Next

When an insurer denies your claim based on an exclusion, the insurer bears the legal burden of proving that the exclusion applies. Exclusion clauses must be conspicuous, plain, and clear, especially in first party all risk policies. If the policy language is ambiguous or the exclusion is buried in fine print, courts often rule in favor of the policyholder.

Start by requesting a written denial letter that cites the specific exclusion language and explains why the insurer believes it applies to your claim. Review the exclusion clause yourself, and compare it to the facts of your loss. Look for gaps: Does the exclusion actually cover the peril you experienced? Is the wording broad or narrow? Are there exceptions or carve backs within the exclusion that might restore coverage?

If you believe the denial is wrong, gather and document the following evidence to challenge it:

Photos, video, and physical evidence showing the cause and extent of damage. Expert reports (contractors, engineers, forensic specialists) that explain what happened and why. Witness statements or third party records (weather reports, police reports, inspection logs). Policy language showing ambiguity, exceptions to the exclusion, or conflicting clauses. Timeline records proving the loss occurred during the policy period and under covered circumstances. Written correspondence with your agent or insurer that contradicts the denial or suggests coverage was expected.

You can file an internal appeal with the insurer, hire a public adjuster to re-evaluate the claim, or consult an insurance attorney to assess whether the insurer misapplied the exclusion or acted in bad faith. In some cases, litigation is necessary to compel payment.

Endorsements, Riders, and Buy Back Options That Can Override Exclusions

Some exclusions can be removed or modified through endorsements, also called riders or buy back clauses. An endorsement is a policy amendment that either restores coverage for an excluded risk or narrows an exclusion’s scope. Endorsements are purchased separately and usually increase your premium.

Common buy back endorsements include flood endorsements for homeowners policies, cyber liability endorsements for general liability policies, and mold remediation endorsements that raise or eliminate mold sublimits. Specialty endorsements can also add coverage for earthquakes, sinkholes, ordinance or law upgrades, and hazardous waste cleanup.

Not all exclusions can be overridden. Some risks, like intentional acts, nuclear hazard, or war, are universally excluded and can’t be restored through standard endorsements. Other exclusions require separate, standalone policies (for example, flood insurance through the National Flood Insurance Program or a private flood carrier).

Here are four key types of endorsements that modify exclusions:

- Coverage restoration endorsements remove or narrow a standard exclusion (for example, adding back cyber coverage or pollution cleanup).

- Sublimit expansion endorsements raise caps on partially covered risks like mold, sewer backup, or identity theft.

- Named peril add ons extend coverage to specific excluded events like earthquake or windstorm in high risk zones.

- Exclusion endorsements. Some endorsements add new exclusions or tighten existing ones, so always read the full text before accepting.

Legal Interpretation of Insurance Exclusions and Why It Matters

Courts apply plain meaning rules when interpreting exclusion clauses. If the language is clear and unambiguous, judges enforce the exclusion as written. But if the exclusion is vague, contradictory, or buried in dense legalese, courts apply the doctrine of contra proferentem, construing ambiguities against the insurer and in favor of the policyholder.

Exclusions must be conspicuous. That means they should be clearly labeled, easy to locate, and written in straightforward language. If an exclusion is hidden in a definitions section, printed in tiny font, or written in confusing jargon, a court may refuse to enforce it.

In first party all risk claims, where the policy covers “all risks of physical loss” unless specifically excluded, the insured only needs to prove the loss occurred. The burden then shifts to the insurer to prove a specific exclusion applies. In third party liability claims, the insurer must investigate the claim and prove the exclusion applies “in all possible worlds,” meaning the exclusion must bar coverage under every conceivable theory of liability, not just the most obvious one. These rules exist to protect consumers from overreaching exclusion language and to make sure insurers can’t deny claims without meeting a high standard of proof.

Final Words

Start with the exclusions, because they’re the fine print that actually changes what you’re covered for. This post defined what exclusions are, showed where to find them in a policy, and explained why insurers use them.

We gave clear examples, explained pricing and claim impacts, covered how to challenge denials, and showed endorsements that can buy coverage back. Read your declarations and exclusion sections carefully.

If you still ask “what is an insurance policy exclusion”, remember: it’s a clause that removes coverage for a specific risk. Check those clauses now, ask for written answers, and you’ll be better protected.

FAQ

Q: What are some examples of exclusions and the major exclusions in a policy?

A: Some examples and major policy exclusions are flood, earthquake, intentional acts, pollution/contamination, cyber/data breaches, pre-existing health conditions, mold and long-term water damage, and business or rideshare vehicle use.

Q: Why do insurance policies have exclusions?

A: Insurance policies have exclusions to limit insurer exposure, keep premiums affordable, and prevent moral hazard; they narrow broad coverage after the insuring agreement so underwriting can price and manage risky perils.

Q: Does plan exclusion mean not covered?

A: A plan exclusion means the policy does not cover that risk unless you buy an endorsement or separate policy; ambiguous exclusions can be contested and, in some cases, courts favor the insured.

{kind=link}