Think a plan change is instant? Think again.

Most insurance changes usually start on the first day of the month after you enroll, but same-day fixes, mid-month cutoffs, and qualifying life events can push that date weeks earlier or later.

This post explains exactly when changes become active for health, employer, auto, home, and life policies.

You’ll see the common gotchas—like missing a carrier cutoff or assuming newborns aren’t covered—and the three quick checks to avoid gaps or surprise bills.

Understanding When Insurance Changes Become Active

Most insurance changes kick in on the first day of the month after you enroll or make your request, but same day coverage, mid month cutoffs, and qualifying events can push your start date weeks forward or back. Health insurance you buy during open enrollment usually begins January 1 if you enroll by December 15. Miss that and you’re looking at February 1. Auto and home endorsements can go live within hours, while life insurance beneficiary updates take effect as soon as the carrier processes your paperwork.

The effective date is when your coverage or change actually starts. It’s the moment claims become payable and premiums begin accruing. Not the same as the policy issue date, which is when the insurer prints and mails your documents, or the binding date, when your application becomes a legal contract (usually when you pay). A policy can be issued on the 10th, bound on the 12th, but not effective until the 1st of the following month.

Health insurance follows strict calendar and enrollment window rules. Most annual changes take effect January 1, midyear changes hinge on qualifying events or special enrollment windows, and carrier specific cutoffs (often the 15th of the prior month) determine whether you wait an extra 30 days. Auto and homeowners endorsements usually start immediately or at 12:01 AM the next day, unless underwriting review is required. Life insurance changes—beneficiary updates, riders, or coverage increases—take effect when the insurer approves your request. That can be same day for simple beneficiary swaps or weeks later if medical evidence is needed.

Common effective date scenarios:

Annual health plan renewals: Coverage begins January 1 for marketplace and most employer plans if enrolled by mid December.

Special enrollment after a qualifying life event: Coverage can start the first of the month after your request, or the day of the event for newborns and adoptions.

Mid month carrier cutoffs: Enroll after the 15th and your start date often jumps to the first of the month after next. Example: enroll January 20, coverage starts March 1.

Same day newborn or adoption coverage: Many plans allow you to enroll within 60 days but backdate coverage to the birth or placement date.

Late month enrollment shifting to the next cycle: Submit your application on January 30 and you may still land a February 1 start if your carrier allows last minute enrollments. Otherwise, you’re waiting until March 1.

Effective Dates for Marketplace and Individual Health Insurance Changes

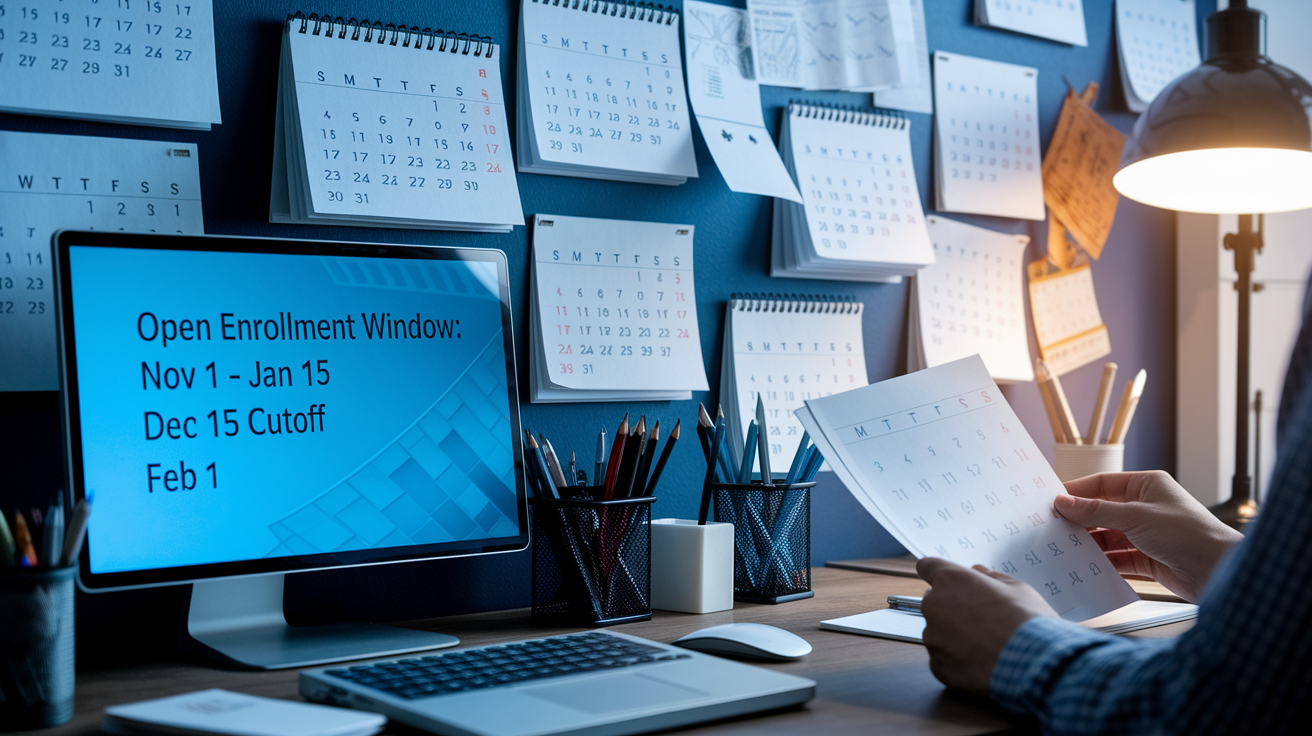

Federal open enrollment runs November 1 through January 15, with a hard December 15 cutoff to secure January 1 coverage. Enroll between December 16 and January 15 and your plan doesn’t start until February 1, leaving you exposed for the first month of the year. States with their own marketplaces sometimes extend the window. California, Colorado, Massachusetts, Minnesota, Nevada, New Jersey, New York, Pennsylvania, Rhode Island, Washington, and Washington, D.C., offered extended enrollment for 2026, with some accepting applications until January 30. Always confirm your state’s exact deadline, because missing it by a single day can cost you a full month of coverage or force you to wait until next year’s open enrollment.

Special enrollment periods let you buy or change coverage outside open enrollment if you experience a qualifying life event. Marriage, birth, adoption, job loss, move to a new ZIP code, or loss of other coverage. You generally have 60 days after the event to enroll, and coverage usually begins the first of the month after your application is approved. Births and adoptions are the exception. You can enroll up to 60 days after the event, but coverage backdates to the day your child was born or placed with you, closing the gap. COBRA works differently. You have 60 days to elect continuation coverage, and if you choose it within that window, coverage is retroactive to the day after your employer plan ended, though you’ll owe back premiums for any gap period.

| Event | Enrollment Timing | Coverage Effective Date |

|---|---|---|

| Open enrollment (enroll by Dec 15) | Nov 1 – Dec 15 | January 1 |

| Open enrollment (enroll Dec 16 – Jan 15) | Dec 16 – Jan 15 | February 1 |

| Birth or adoption SEP | Within 60 days after event | Date of birth or placement (retroactive) |

| Marriage, job loss, or move SEP | Within 60 days after event | First of the month after approval |

| Missed open enrollment, no SEP | No qualifying event | Wait until next open enrollment (Jan 1 following year) |

Employer-Sponsored Insurance Change Timing

Employers can modify group health plans at any time during the year, but federal rules force them to give employees 60 days’ advance notice before implementing changes and to distribute a Summary of Material Modifications within 210 days after the plan year containing the change ends. That notice requirement means an employer planning a July 1 plan switch must alert employees by May 1 at the latest. If the change increases employee costs or narrows networks, the employer must usually offer a mini open enrollment so affected workers can adjust their elections or drop coverage. Most employers skip the hassle and make all plan changes effective January 1, timing them to the annual open enrollment window in the fall.

Mid year employee changes are tightly restricted if premiums are paid with pre tax dollars through a Section 125 cafeteria plan. IRS rules prohibit changing elections unless a qualifying life event occurs. Marriage, divorce, birth, adoption, job status change, dependent aging out, or significant cost increase. The change must be “consistent with” the event. You can’t use a marriage to drop coverage, you can use it to add a spouse. The effective date usually lands on the first of the month after the event is reported and approved. If premiums are paid post tax, the employer’s plan documents control whether mid year changes are allowed, and some employers permit cancellations or downgrades at any time.

Administrative factors can delay even approved changes. Carriers must consent to mid year plan modifications, and if the employer is switching insurers or changing contribution formulas, the new carrier will verify minimum participation rules and underwriting requirements before binding coverage. Payroll cycles matter, too. If your employer processes benefits changes only on the first and fifteenth of each month, a request submitted on the 10th might not take effect until the first of the following month, and the coverage start date will follow the payroll effective date. When an employer adds a waiting period mid year (capped at 90 days under the ACA), new hires won’t see coverage start until the waiting period expires, even if they complete enrollment on day one.

Effective Dates for Mid-Year Changes Triggered by Qualifying Life Events

Qualifying life events open a 60 day window to enroll in or change employer sponsored or marketplace coverage, and the effective date depends on when you report the event and what type of event it is. Report a marriage on March 10, and your new spouse’s coverage usually begins April 1. That’s the first of the month after your election is processed. Report a birth on March 10, and the baby’s coverage often backdates to March 10 itself, even if you don’t submit the enrollment paperwork until late April, as long as you stay within the 60 day reporting deadline.

The timing rules shift when you lose other coverage. If you know in advance that your coverage will end, say your employer announced a plan termination effective March 31, you can request a special enrollment period up to 60 days before the loss, and your new plan can start April 1 with no gap. If the loss is unexpected (you’re laid off on March 15), you have 60 days after March 15 to enroll, and coverage typically begins the first of the month after your application is approved. Likely May 1 if you enroll in early April. Moves to a new rating area usually require proof that you had at least one day of coverage in the prior 60 days, except when you’re moving from outside the U.S. In that case, coverage starts the first of the month after enrollment without a prior coverage check.

Six common life event scenarios and their effective date rules:

Marriage: Enroll within 60 days. Coverage for the new spouse begins the first of the month after election approval. Example: marry April 5, enroll April 20, coverage starts May 1.

Birth or adoption: Enroll within 60 days. Coverage backdates to the date of birth or placement, closing any gap. Example: baby born April 5, enroll May 30, coverage retroactive to April 5.

Divorce or legal separation causing loss of coverage: Enroll within 60 days of the loss. Coverage begins the first of the month after approval.

Job loss or reduction in hours: Enroll within 60 days. If loss is known in advance, request coverage to begin the day after the old plan ends. Otherwise, first of the month after approval.

Move to a new ZIP code or rating area: Enroll within 60 days. Coverage starts the first of the month after approval. May require proof of prior coverage unless moving from abroad.

Dependent aging out (turning 26 on a parent’s plan): Enroll within 60 days. Coverage begins the first of the month after the birthday or approval, depending on state rules and plan documents.

How Quickly Auto, Home, and Life Insurance Changes Take Effect

Auto insurance endorsements (adding a driver, increasing liability limits, or swapping vehicles) usually take effect immediately upon insurer approval or at 12:01 AM the next day, whichever the carrier specifies in the confirmation. If you call your agent at 2 PM on a Tuesday to add your teenage daughter to the policy, coverage often starts that same day at 2 PM or at 12:01 AM Wednesday morning. High risk changes, like adding a driver with a recent DUI or increasing a stated value classic car limit, may trigger underwriting review, delaying the effective date by days or weeks until the insurer completes the risk assessment and either approves the change or offers a modified premium.

Homeowners endorsements (increasing dwelling coverage, adding scheduled personal property, or adding flood or earthquake riders) follow the same immediate or next day pattern, but underwriting dependencies are more common. Request a $100,000 jewelry rider and the insurer will likely require an appraisal before binding the change. Submit the appraisal electronically and the endorsement might take effect within 24 hours, but mail it and you’re waiting 5 to 10 business days for processing. Coverage increases above certain thresholds (often $500,000 for dwelling or $100,000 for a single item) almost always require underwriting review, which can push the effective date out by two weeks.

Life insurance beneficiary changes take effect the moment the insurer receives and approves your written request, which is usually same day if submitted electronically or within 3 to 5 business days if mailed. Adding a rider (accidental death, waiver of premium, or a term conversion option) depends on underwriting. If no medical evidence is required, the rider starts the first of the month after approval. If evidence of insurability is needed, expect a 3 to 6 week timeline from application to effective date, and the insurer may deny the change if your health has declined since the original policy was issued.

When HRAs (ICHRA, QSEHRA, Integrated/GCHRA) Change Plan Effective Dates

Individual Coverage HRAs (ICHRAs) and Qualified Small Employer HRAs (QSEHRAs) let employers reimburse employees’ individual health insurance premiums tax free, but reimbursements don’t begin until the underlying health plan is active. If your employer implements an ICHRA on July 1 and you enroll in an individual plan that starts August 1, you won’t see reimbursements until August, even though the ICHRA offer is technically available July 1. Implementing an ICHRA also triggers a 60 day special enrollment period for employees, meaning they can buy individual coverage outside open enrollment as soon as the ICHRA is offered, and their plan effective date follows standard marketplace rules. Usually the first of the month after enrollment.

Integrated HRAs (also called Group Coverage HRAs or GCHRAs) pair with an employer sponsored group health plan to reimburse out of pocket costs like deductibles and coinsurance. These can be added at any point during the year without triggering a special enrollment period, because employees are already enrolled in the underlying group plan. The effective date is the day the employer formally adopts the HRA, which can be mid month or on the first, and reimbursements are available immediately for claims incurred on or after that date. Though in practice, claims must be submitted and approved before the employer pays, so the first reimbursement check usually arrives 2 to 4 weeks after the HRA launch.

Key HRA timing differences:

ICHRA effective date: The date the employer’s ICHRA plan document specifies. Reimbursements begin only after the employee’s individual plan starts.

ICHRA special enrollment period: Employees have 60 days from the ICHRA offer date to enroll in individual coverage. Plan start follows marketplace rules (first of the month after approval).

QSEHRA effective date: January 1 for calendar year plans. Reimbursements begin when the employee’s individual plan or alternative coverage (with a preventive/MEC plan if required) is active.

Integrated HRA / GCHRA effective date: Any day the employer chooses. No enrollment period needed since employees are already on the group plan. Reimbursements available immediately for post effective date claims.

Reimbursement start vs HRA start: The HRA can be “live” on paper, but actual reimbursement payments don’t flow until the employee has active coverage and submits qualifying claims.

Situations That Delay or Change the Expected Effective Date

Missing documentation is the most common reason a coverage change doesn’t take effect on the expected date. Fail to provide a marriage certificate within the insurer’s required timeframe (often 30 to 60 days) and your special enrollment request gets denied, pushing your effective date to the next open enrollment or the next qualifying event. Underwriting review adds days or weeks when you’re increasing coverage limits, adding high risk drivers or properties, or applying for life insurance riders that require medical evidence. Submit your application expecting a May 1 start, and if underwriting isn’t complete by the carrier’s cutoff date (often the 15th of the prior month), your effective date automatically shifts to June 1 or later.

Payment timing and grace periods create another layer of delay and uncertainty. Most carriers require the first premium payment before coverage binds, and if you enroll on December 14 but don’t pay until December 20, your January 1 effective date might slip to February 1 because the insurer’s payment cutoff was December 15. Late payments during the policy term trigger grace periods (usually 30 days for marketplace plans, shorter for private plans), and if you’re trying to make a mid policy change while in a grace period, many carriers will block the change until your account is current, delaying your requested effective date by weeks or even canceling the pending change if you don’t catch up in time.

Four common delay causes:

Carrier enrollment cutoffs: Enroll after the 15th of the month and many insurers automatically push your start date to the first of the month after next, even if you thought you were within the window.

Paper vs electronic submission: Mailed applications and documents can add 5 to 10 business days of postal and manual processing time compared to instant electronic submissions.

Incomplete or incorrect forms: A missing signature, wrong Social Security number, or unsigned beneficiary change form sends your request back to the bottom of the queue, restarting the processing clock.

Outstanding premium balance or grace period status: Carriers routinely freeze all policy changes (adding dependents, increasing limits, changing coverage tiers) until past due premiums are paid in full, and the freeze can last the entire grace period.

Final Words

Quick recap: most changes hit on the first day of the next month. Open enrollment and marketplace deadlines push many starts to Jan 1 or Feb 1. SEPs can be same-day for births or follow 60-day rules. Employer changes hinge on payroll cutoffs and notice. Auto, home, and life changes often start immediately unless underwriting holds them up.

Know the difference between effective date and issue date. Watch for missing docs, late payment, or carrier cutoffs.

Ask your insurer or HR: when do insurance changes take effect, and get it in writing. Do that and you’ll avoid nasty surprises.

FAQ

Q: Does insurance take effect immediately?

A: Insurance doesn’t always take effect immediately. Many changes start the next day or the first of the following month; some require carrier cutoffs, same‑day coverage, or proof and payment before they’re active.

Q: Is autoimmune disease covered by insurance?

A: Autoimmune disease is generally covered by health insurance, but coverage, prior‑authorization, drug formularies, and out‑of‑pocket costs vary by plan—ACA plans can’t deny you for preexisting conditions.

Q: Is Medicare free at age 65?

A: Medicare isn’t automatically free at 65. Part A is premium‑free for most who paid Medicare payroll taxes; Part B, Part D, and Advantage plans usually charge monthly premiums and cost‑sharing.

Q: Can I get life insurance with lupus?

A: You can often get life insurance with lupus, but approval and rates depend on severity, medications, organ involvement, and recent flares; expect higher premiums or rated policies and provide medical records.

{kind=link}