What if your claim is denied because of a single buried sentence?

Exclusions are that sentence: the lines in your policy that tell you what the insurer won’t pay.

Skip them and you could get a denial instead of a check.

This post lists the most common exclusions across home, auto, health, and life insurance, explains why insurers use them, and gives the red flags to check before you file.

Read on to avoid surprises and save yourself big bills.

Key Exclusions Found Across Common Insurance Policies

An exclusion tells you what your insurance won’t pay for. It’s the line between getting a check and getting a denial letter.

Standard policies, home, auto, health, life, all include exclusions designed to limit the insurer’s exposure to predictable, intentional, or catastrophic losses. These show up in the “Exclusions” section, usually after coverage descriptions. Sometimes they’re buried inside definitions or endorsements. Skip them, and you’ll find out what’s not covered when you file a claim and get denied.

Here’s what you’ll find excluded across most policy types:

Intentional damage or injury. If you deliberately cause harm or destruction, coverage is denied.

Wear and tear. Gradual deterioration, rust, rot, aging-related failures. All excluded.

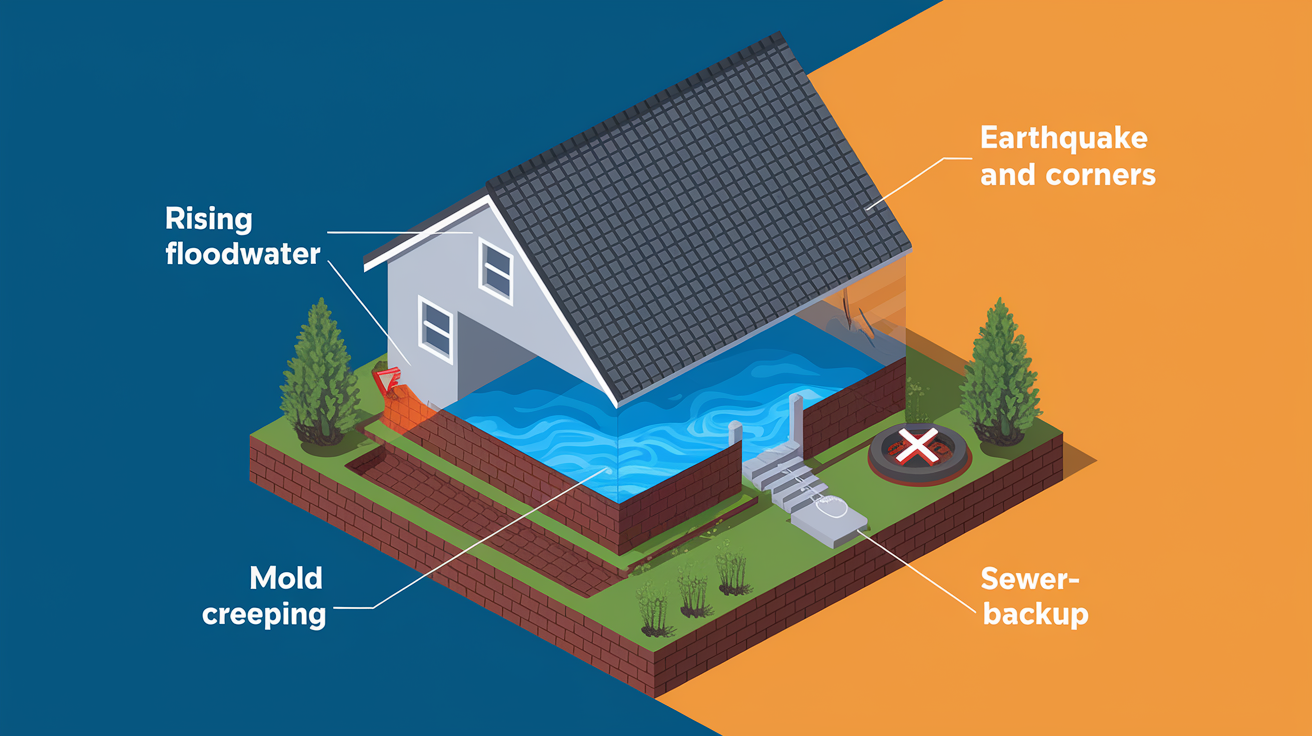

Flooding. Standard home and auto policies exclude flood damage unless you buy separate flood insurance.

Earthquakes. Earthquake damage gets excluded from homeowners policies. Requires an endorsement or separate policy.

Acts of war. War, invasion, insurrection, hostile military actions. Universally excluded.

Business losses. Personal policies exclude claims tied to business operations, commercial use, or professional services.

Cosmetic procedures. Health insurance generally excludes elective cosmetic treatments unless medically necessary.

High-risk activities. Life policies often exclude deaths from skydiving, racing, or other hazardous hobbies unless specifically ridered.

Criminal acts. Losses tied to illegal behavior are denied. Insurers may void claims if the underlying event was a crime.

Pre-existing conditions. While major U.S. health reforms limited this exclusion, short-term and limited-duration plans may still impose it.

Here’s how exclusions work in real life. A homeowner files a claim after heavy rain floods the basement. The insurer denies it. Flooding is excluded, and there’s no flood endorsement on file. A driver crashes during a road-rage incident. The insurer calls it intentional and denies the claim. A contractor’s client sues over intentional property damage during a payment dispute. The general liability policy excludes intentional acts. In each case, the policyholder believed they were covered until the exclusion was cited.

Home Insurance Exclusions Explained

Homeowners policies are written as “open peril” or “named peril” contracts. Open-peril policies cover everything except what’s explicitly excluded. Named-peril policies only cover listed causes. Either way, the exclusions list is where claims get denied, and most denials stem from a handful of recurring exclusions.

Flood damage is the most common gap. Standard homeowners policies exclude flooding caused by rising water, heavy rain, storm surge, or overflowing rivers. If your basement floods after a storm, you’re paying out of pocket unless you purchased a separate flood policy through the National Flood Insurance Program or a private carrier. Flood policies typically carry a 30-day waiting period before coverage begins, so you can’t buy one after the forecast shows a hurricane approaching.

Earthquake damage is also excluded unless you add an earthquake endorsement or buy a separate earthquake policy. This affects homeowners in seismic zones but also creates claim confusion in other regions. Some insureds assume “structural damage” is always covered, but if the trigger is ground movement, it’s excluded.

Mold resulting from poor maintenance or long-term leaks is excluded as well. Insurers will cover sudden mold growth from a burst pipe, but deny claims when mold spreads due to an unrepaired roof or ignored humidity problem.

Sewer backup and sump pump overflow are often excluded unless you add a sewer-backup endorsement. Without it, sewage flooding your basement during a storm is denied. Pest damage, termites, rodents, insects, excluded. Insurers expect you to handle prevention and mitigation. Wear and tear, gradual deterioration, and deferred maintenance are universally excluded. A settled foundation, rusted pipes, or a roof that fails after years of neglect will not trigger a payout.

Most home policies exclude or severely limit coverage for:

Flood damage. Excluded. Requires separate flood insurance with approximately 30-day waiting period.

Earthquake damage. Excluded unless endorsed or added as separate policy.

Mold from maintenance neglect. Covered only if caused by a sudden, covered peril.

Sewer backup and sump overflow. Excluded without endorsement.

Pest infestations and animal damage. Termites, rodents, and insect damage are not covered.

Auto Insurance Exclusions You Should Know

Auto policies exclude more than most drivers realize, especially when the damage stems from intentional acts, business use, or vehicle neglect. Standard personal auto policies are designed to cover accidents, unexpected collisions and liability from normal driving, but exclude anything that falls outside that definition.

Mechanical breakdown and normal wear and tear are excluded. If your transmission fails, your engine seizes, or your brake pads wear out, the insurer won’t pay for repairs. Mechanical breakdown insurance is a separate product, often sold by dealerships or as an optional add-on.

Racing, stunt driving, and intentional collisions are excluded. If you crash your car during a track day, road race, or out of anger, expect a denial. Damage caused while driving for commercial purposes, delivery driving, rideshare without proper endorsement, or hauling goods for pay, is excluded under personal policies.

Unlisted or excluded drivers create another common trap. If someone you explicitly excluded from your policy causes an accident while driving your car, the claim is denied. Custom parts and aftermarket equipment often have sublimits or are excluded entirely unless you notify the insurer and pay for an endorsement. Personal property inside the vehicle, laptops, phones, tools, is usually excluded. Those items fall under your homeowners or renters policy, not auto.

Typical auto exclusions include:

Mechanical failure and wear. Engine, transmission, brake, and electrical repairs are excluded. Consider mechanical breakdown insurance.

Racing, stunts, and intentional damage. Any competitive driving or deliberate collision is denied.

Commercial or delivery use. Personal policies exclude claims during business activities like food delivery or rideshare unless endorsed.

Unlisted or excluded drivers. If an excluded driver causes a loss, coverage is denied.

Health Insurance Exclusions and Limitations

Health insurance exclusions can be confusing because they vary by plan type, state, and whether the policy is ACA-compliant. Major medical plans sold after 2014 reforms generally can’t exclude coverage based on pre-existing conditions, but short-term plans and limited-duration policies still impose those exclusions.

Cosmetic procedures are excluded unless deemed medically necessary. A nose job for appearance is denied. Reconstructive surgery after an accident may be covered. Experimental or investigational treatments are commonly excluded, and the definition varies by insurer. Some plans deny coverage for new cancer therapies or off-label drug use unless the treatment is approved by a specific review panel.

Routine dental and vision care are excluded from most health plans and require separate dental and vision policies.

Long-term custodial care, nursing home stays, home health aides, assisted living, is excluded from standard health insurance. That exposure requires long-term care insurance. Fertility treatments, including in-vitro fertilization, are often limited or excluded. Many plans impose caps or exclude IVF entirely. Out-of-network care may be excluded or subject to much higher cost-sharing, depending on plan design.

Common health insurance exclusions:

Elective cosmetic surgery. Excluded unless reconstructive or medically necessary.

Experimental treatments. Often denied. Coverage depends on plan definitions and medical review.

Long-term custodial care. Excluded. Requires separate long-term care insurance.

Life Insurance Exclusions to Watch For

Life insurance exclusions typically focus on deaths that occur during the contestability period, deaths tied to high-risk behavior, and deaths resulting from misrepresentation on the application. The contestability period, commonly two years from policy issue, allows the insurer to investigate and deny claims if the insured lied on the application or omitted material facts.

Suicide clauses are standard. If the insured dies by suicide within the first two years, the insurer may return only the premiums paid or deny the death benefit entirely. After the two-year window, suicide is generally covered.

Deaths during hazardous activities, skydiving, BASE jumping, mountaineering, racing, are often excluded unless the insured purchased a rider covering those activities. Deaths tied to illegal acts or occurring during the commission of a crime are excluded.

Misrepresentation on the application is the most common basis for denial. If you understate health issues, omit smoking history, or lie about risky hobbies, the insurer can void the policy during the contestability period. After two years, policies typically become incontestable except in cases of outright fraud.

Key life insurance exclusions include:

Suicide within two years. Death benefit denied or limited to return of premiums during contestability period.

High-risk activities. Deaths from skydiving, racing, or other hazardous hobbies excluded unless ridered.

Misrepresentation or fraud. False statements on the application can void coverage within the contestability period, commonly two years.

Why Insurance Companies Use Exclusions

Exclusions exist to keep insurance functioning as a system designed for fortuitous, unexpected losses rather than predictable or intentional ones. Without exclusions, premiums would be unaffordable, and insurers would face exposure to correlated catastrophic events that could bankrupt the company and leave all policyholders without coverage.

Moral hazard is the first reason. If insurers covered intentional acts, maintenance failures, or easily preventable losses, policyholders would have less incentive to mitigate risk. Excluding wear and tear encourages property maintenance. Excluding intentional damage discourages fraud and reckless behavior. Excluding flood and earthquake from standard policies allows insurers to isolate catastrophic, geographically correlated risks and price them separately. When one hurricane or earthquake strikes, thousands of claims hit simultaneously, creating insolvency risk if not carefully managed.

Actuarial modeling and reinsurance structures rely on exclusions to predict loss frequency and severity. Catastrophic perils like war, nuclear events, and pandemics are excluded because they’re uninsurable under normal premium structures. Losses would be near-infinite and affect all insureds at once. Regulatory frameworks and reinsurance markets are built around this segmentation, which is why you buy separate flood, earthquake, and cyber policies rather than bundling everything into one contract.

Exclusions also allocate risk to the appropriate policy type. Professional liability belongs in an errors-and-omissions policy, not general liability. Employee injuries belong in workers’ compensation, not commercial general liability. Vehicle liability belongs in auto insurance, not homeowners. Exclusions draw these boundaries and prevent overlap that would lead to coverage disputes and claims denial when two policies each point to the other.

How to Fill Coverage Gaps and Reduce Risk

Closing exclusion gaps means identifying your real exposures and matching them to the right endorsements, riders, or separate policies. The goal isn’t to buy every add-on an agent offers, but to cover the scenarios most likely to cause financial hardship if excluded.

Start by purchasing separate policies for excluded catastrophic perils. If you’re in a flood zone, buy flood insurance through NFIP or a private carrier. Expect a 30-day waiting period. If you’re in a seismic zone, add earthquake coverage via endorsement or standalone policy. If you run a business from home or use your car for delivery or rideshare work, buy a business owner’s policy or commercial auto coverage. Personal policies exclude business use.

Add endorsements to fill common gaps in your existing policies. Sewer-backup endorsements are inexpensive and cover a frequent denial trigger. Scheduled personal property endorsements bypass sublimits on jewelry, art, and collectibles. Standard homeowners policies often cap jewelry coverage at $1,000 to $2,500, but scheduling items with appraisals extends full replacement value. Mechanical breakdown insurance for vehicles covers repairs excluded under standard auto policies. Umbrella liability policies extend your liability limits beyond your home and auto policies, commonly starting at $1,000,000 in additional coverage.

Common add-ons and supplemental coverage options:

Flood insurance. Separate policy required. 30-day waiting period typical for NFIP coverage.

Earthquake endorsement. Added to homeowners policy or purchased separately.

Sewer-backup endorsement. Covers sewage overflow and sump pump failure.

Scheduled personal property. Extends coverage for jewelry, art, collectibles beyond sublimits.

Umbrella liability. Adds $1,000,000+ in liability coverage above home and auto limits.

Commercial or rideshare endorsements. Covers business use of vehicles or home-based business operations.

Before buying add-ons, read your declarations page to confirm what’s already covered and review the exclusions section to identify real gaps. Don’t assume you need every endorsement. Focus on exposures that would cost more than a few thousand dollars out of pocket or that match your actual risk profile. Flood zone, earthquake region, high-value property, commercial activity.

Final Words

We ran through the exclusions policies hide: flood and earthquake for homes, wear and tear and racing for cars, cosmetic or experimental care for health, and risky hobbies or misstatements for life. We also covered why insurers use exclusions and straightforward ways to close gaps.

Don’t assume brochures tell the whole story. Check wording, networks, contestability periods, and get riders in writing.

Keep a short checklist that flags common insurance policy exclusions, get written answers, and add only the coverages you need. Do that and your policy will work when it matters.

FAQ

Q: What are the common exclusions in insurance, and what are some examples?

A: The common exclusions in insurance are intentional damage, wear and tear, floods and earthquakes, acts of war, business losses on personal policies, cosmetic procedures, and high‑risk activities.

Q: What are common exclusions to a life insurance policy?

A: Common exclusions to a life insurance policy include death from high‑risk hobbies, suicide during the contestability period, deaths tied to illegal acts, and fraud or material misrepresentation on the application.

{kind=link}