Ever opened a renewal notice and saw your premium jump with no percent listed?

That’s how insurers bury the math.

You can figure the rate increase in seconds with one simple formula: (New − Old) ÷ Old × 100.

This post walks you through that exact calculation, gives real-dollar examples, a spreadsheet shortcut, and the common gotchas people miss—like comparing different billing terms or confusing percentage points with percent change.

By the end you’ll know whether a hike is reasonable, worth disputing, or a firm reason to shop.

Core Method for Calculating an Insurance Rate Increase Percentage

The formula’s simple: subtract your old premium from your new one, divide that difference by your old premium, multiply by 100. Written out: (New Premium − Old Premium) / Old Premium × 100. Works for auto, home, health, life. Works for annual, semi-annual, monthly premiums.

You need this because insurers won’t always tell you the percentage on renewal notices. You’ll see a dollar jump with no context, or vague language about “market adjustments.” Computing it yourself shows whether the change is worth accepting, negotiating, or walking away from.

Here’s how you do it:

-

Find the dollar increase. Subtract old from new. Old annual premium was $900, new one’s $1,260? That’s a $360 increase.

-

Divide the dollar increase by your old premium. Same example: $360 ÷ $900 = 0.40.

-

Multiply by 100. Take that 0.40, multiply by 100, you get 40%. There’s your rate increase percentage.

People screw this up by confusing percentage increase with percentage points. A jump from 5% to 10% is 5 percentage points, but it’s a 100% increase in relative terms: (10 − 5) / 5 × 100 = 100%. When you’re calculating premium changes, use dollar amounts. Not prior percentages. Round your final result to two decimal places—40.00% or 88.89%—and make sure you’re comparing the same coverage and billing term. Annual to annual. Monthly to monthly. Otherwise your math’s off.

Step-by-Step Premium Increase Examples Using Real Dollar Amounts

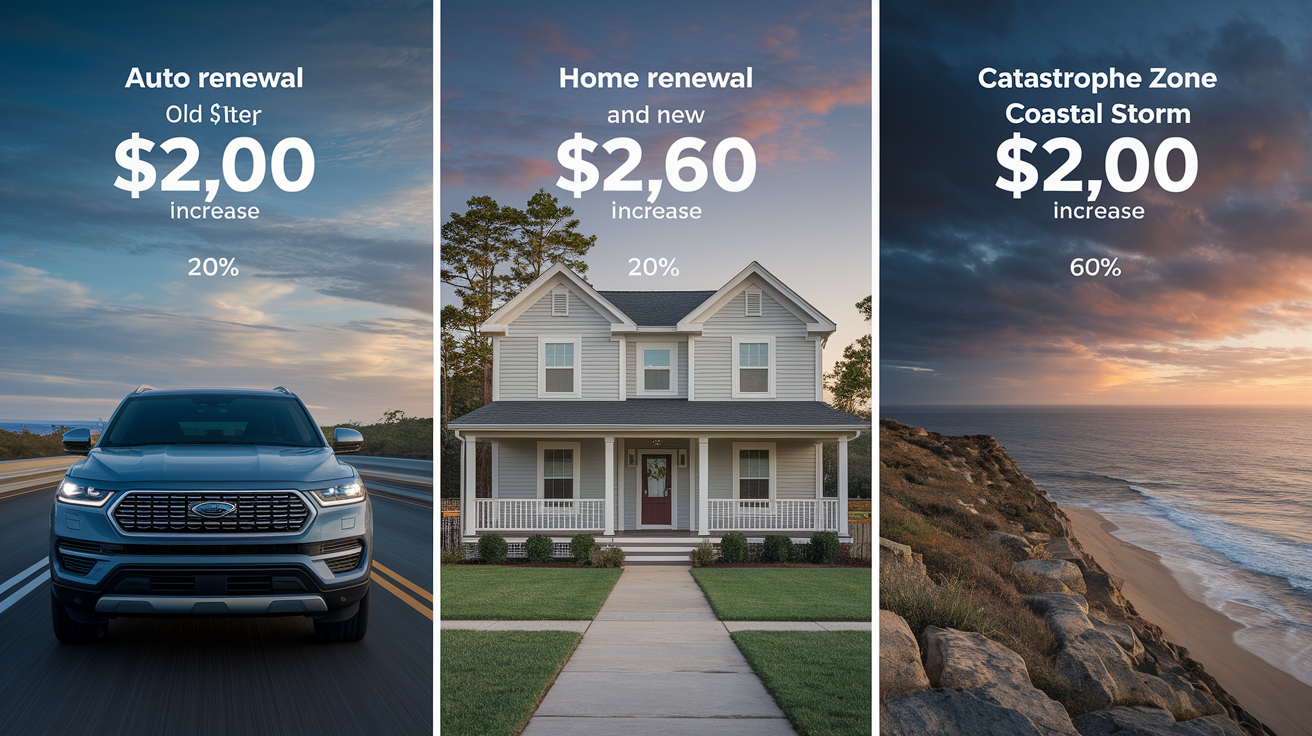

Example 1: Moderate increase on auto. Previous annual premium was $1,200. Renewal shows $1,440. Dollar increase is $1,440 − $1,200 = $240. Divide $240 by $1,200, you get 0.20, multiply by 100: 20% increase. This happens after a minor at-fault accident, a small comprehensive claim, or you lose a safe-driver discount because of a ticket.

Example 2: Big increase after a major claim. Old homeowner premium was $900 per year. After filing a liability claim with a $15,000 payout, renewal jumps to $1,260. Increase is $1,260 − $900 = $360. Divide $360 by $900 = 0.40, multiply by 100: 40% increase. This range (30–50%) shows up for moderate-to-serious claims that tell the insurer you’re higher risk now.

Example 3: Severe increase in a catastrophe zone, clean record. You live in coastal Louisiana. Old premium was $2,000 annually. After multiple hurricanes hit the region (you filed nothing), your renewal’s $3,200. Increase is $3,200 − $2,000 = $1,200. Divide $1,200 by $2,000 = 0.60, multiply by 100: 60% increase. Market factors like inflation, catastrophic losses, reinsurance costs can drive big percentage increases even when your personal record’s spotless.

| Old Annual Premium | New Annual Premium | Dollar Change | Percentage Increase |

|---|---|---|---|

| $1,200 | $1,440 | $240 | 20.00% |

| $900 | $1,260 | $360 | 40.00% |

| $2,000 | $3,200 | $1,200 | 60.00% |

Spreadsheet and Calculator Methods for Computing Premium Percentage Changes

Setting up a spreadsheet takes two minutes and gives you a reusable template. Open Excel or Google Sheets, create five columns: A = Policy Type (Auto, Home, whatever), B = Old Premium, C = New Premium, D = Dollar Increase, E = Percentage Increase. First row under each column, enter your labels. Row 2 is where you enter data and formulas.

Exact Cell Formulas to Use

- Cell A2: Type the policy name or insurer (like “Auto – State Farm”).

- Cell B2: Enter your old annual premium as a number (1200).

- Cell C2: Enter your new annual premium (1440).

- Cell D2 formula:

=C2-B2— Calculates the dollar increase automatically. - Cell E2 formula:

=(C2-B2)/B2*100— Computes the percentage increase. For a rounded result to two decimals, use=ROUND((C2-B2)/B2*100,2).

Once you’ve got formulas in row 2, click the small square at the bottom-right corner of cell E2, drag down to autofill for more rows. You can compare three, five, ten quotes side by side. You’ll see instantly which insurer’s renewal is an outlier, which offers are competitive. Shopping after a rate increase? This method shows you the best replacement option in seconds.

Interpreting Your Insurance Premium Percentage Increase

Not all percentage increases hit the same. A 10% jump on a $600 policy is $60 annually. Noticeable but manageable. A 60% jump on a $2,500 policy is $1,500 extra per year, which can force budget trade-offs or a switch to a new insurer. Knowing common ranges helps you decide how aggressively to respond.

Here’s a practical framework:

- Under 20%: Minor increase. Often tied to loss of small discounts, inflation adjustments, or a non-severe comprehensive claim. Usually not worth switching insurers unless you were already shopping.

- 20% to 50%: Moderate increase. Shows up after at-fault accidents, mid-sized claims, or big market cost shifts. Worth requesting an itemized explanation, asking about discounts, running comparison quotes.

- 50% to 100%: Big increase. Suggests major underwriting concern—serious accident, multiple claims, high-risk property exposure, market disruption. Strong case to shop competitors, review your coverage for over-insurance, appeal or negotiate if the increase seems unjustified.

- Over 100%: Excessive increase. Rare outside catastrophe zones or after multiple high-severity claims. Investigate the insurer’s rationale, file a complaint with your state regulator if the justification’s weak, immediately compare quotes from at least three other carriers.

Most post-claim increases stick around for three to five years. A 40% hike isn’t a one-time cost, it’s a multi-year financial drag. If your $1,200 premium becomes $1,680 and stays elevated for four years, you’re paying an extra $1,920 total. That cumulative impact makes even “moderate” percentages worth addressing.

One thing: percentage increases and percentage points aren’t the same. If your insurer says rates are “up 3 percentage points,” that’s vague unless you know the base. A rate moving from 5% to 8% is 3 percentage points but a 60% relative increase: (8 − 5) / 5 × 100 = 60%. Always calculate using dollar amounts to avoid confusion. When you’re evaluating year-over-year changes, use the same formula but confirm you’re comparing identical coverage and billing cycles. Annual to annual, not annual to a six-month term.

Insurance Type Differences in Calculating and Understanding Rate Increase Percentages

Auto insurance rate increases are the most predictable and the most studied. After an at-fault accident, the national average increase is around 58%, but state-level variation is wide. New Jersey drivers see roughly 80%, Rhode Island drivers average closer to 15%. Insurer algorithms vary too. One carrier might raise rates 82% after an at-fault collision, another just 23%. Comprehensive claims (theft, weather damage) typically produce smaller percentage increases, often 10–25%, because they don’t indicate driver behavior risk.

Homeowners insurance behaves differently. Rate increases depend heavily on claim type and property characteristics. A liability claim from a slip-and-fall might trigger a 20–40% increase. A major roof or water-damage claim in a high-risk area can push increases above 50%. Repeated claims within a few years often lead to non-renewal rather than another percentage hike. Market forces matter more here than in auto. If roofing costs in your region jumped 35% since 2020, your insurer’s rate adjustment reflects that even if you never filed a claim. Location exposure—distance to a fire hydrant, hurricane or wildfire zone, age of electrical and plumbing systems—gets re-priced frequently, so percentage changes aren’t always tied to your behavior.

Health insurance premium changes are the least connected to individual claims in the traditional sense. If you’re in an employer group plan, your premium’s based on the risk pool, not your personal medical history. Individual marketplace (ACA) plans adjust premiums annually based on age, rating area, tobacco use, plan metal level, but not your claims from the prior year. But if you switch from a Bronze plan to a Gold plan, the percentage difference can be big. Sometimes 60–100% higher premiums for lower deductibles and out-of-pocket limits. Calculating the percentage change is useful when comparing plan options year to year, but the drivers are plan design and regulatory factors, not claim surcharges.

How Coverage Choices Change the Percent Increase

Adjusting your deductible or adding endorsements changes both your premium and the baseline used in percentage calculations. Raise your auto collision deductible from $500 to $1,000, you might save $120 annually. If your old premium was $1,200, your new premium becomes $1,080—a 10% decrease: ($1,080 − $1,200) / $1,200 × 100 = −10%. The percentage looks good. But you’ve also increased your out-of-pocket risk by $500 per claim.

-

Deductible increases lower the percentage but raise claim-time cost. A high deductible might turn a 40% increase into a 25% increase, but you’re self-insuring more risk.

-

Adding endorsements raises the baseline premium. Add earthquake coverage to your homeowner policy for $300/year, any market-wide percentage increase applies to the new, higher base, compounding the dollar impact.

-

Removing coverage lowers the base and can mask rate increases. If your insurer drops certain coverages or limits due to underwriting changes, your premium might stay flat even though the per-unit rate increased. Always compare identical coverage when calculating percentage changes.

Factors That Drive the Size of an Insurance Rate Increase Percentage

Your personal rating factors have the most direct influence on percentage increases. Credit-based insurance scores are a major lever in most states. A driver in Texas with excellent credit might pay $1,200 annually for the same coverage that costs a driver with poor credit $1,800—a $600 difference. If both drivers file identical at-fault claims, the percentage increase formula starts from a different base, but the insurer’s underwriting adjustment often scales similarly. The driver with poor credit ends up paying even more in absolute dollars after the hike.

Claims frequency and severity drive the biggest post-claim percentage jumps. A single at-fault accident with $8,000 in property damage and $12,000 in medical bills signals higher future risk than a $2,000 fender-bender with no injuries. Insurers use historical data and increasingly machine-learning models to predict repeat-claim probability. If your accident fits a high-risk pattern—young driver, urban area, late-night collision—the percentage increase will be steeper than for an older driver in a rural area with a minor parking-lot bump.

Market-level cost trends affect everyone in a risk pool, often creating percentage increases that have nothing to do with your personal record. Between 2020 and 2024, roofing materials in some regions increased 30–40%. Auto repair labor and parts costs rose steadily due to supply-chain issues and wage inflation. Insurers build these cost forecasts into rate filings two to three years ahead. That means a 2024 renewal increase might reflect repair-cost projections for 2025–2026 claims. In catastrophe-exposed areas—coastal Florida, wildfire zones in California, hail-prone Texas—reinsurance costs spiked after major loss events, and insurers passed those costs to policyholders as percentage increases even when individual homeowners filed no claims.

Here are five things that directly influence how large your percentage increase will be:

- Credit-based insurance score: Poor credit can add 30–60% to baseline premiums. Post-claim increases compound that gap.

- Claims and violation history: A clean record for five years earns maximum discounts. A single at-fault accident typically removes those discounts and adds a surcharge for 3–5 years.

- Location and rating territory: ZIP codes with higher claim frequency, theft rates, or catastrophic exposure see bigger percentage increases during market-wide repricing.

- Inflation and repair-cost trends: When parts, labor, medical care, or construction costs rise, insurers adjust rates upward across entire books of business.

- Insurer loss ratios: If an insurer’s loss ratio (claims paid ÷ premiums collected) exceeds targets, regulators often approve rate increases to restore financial stability, raising everyone’s premiums by a similar percentage.

How to Minimize or Challenge a High Premium Percentage Increase

If your percentage increase falls into the “moderate” or “significant” range, you’ve got leverage. Start by calling your insurer, ask for an itemized breakdown of the rate change. Request confirmation that all applicable discounts—multi-policy, good driver, defensive driving course, low mileage, paperless billing—are still applied. Sometimes a discount expires or gets dropped due to a data error, inflating the percentage increase unnecessarily.

State insurance regulators require most insurers to justify rate increases, especially after claims. If your increase seems disproportionate to the claim severity or your driving record, file a complaint with your state insurance department. Regulators review whether the insurer followed approved rate schedules and applied increases consistently. In a few cases, complaints trigger audits that result in refunds or adjustments. You can’t usually “negotiate” a rate in the traditional sense, but you can ask for accident forgiveness if it’s available as a policy add-on and you haven’t used it yet.

The best response to a high percentage increase is shopping for replacement coverage. Get quotes from at least three other insurers, using identical coverage limits, deductibles, policy features so the percentage comparison is apples-to-apples. Loyalty doesn’t pay in insurance. Switching after a rate hike often saves 15–30%, sometimes more. Even if the new insurer factors in your recent claim, competitive underwriting and different risk models mean your percentage increase with them might be half what your current insurer’s charging.

Here are five actions to take when facing a high percentage increase:

-

Enroll in or purchase accident forgiveness if you haven’t had a claim yet. Some insurers offer it as a standard feature after a few claim-free years. Others sell it as an add-on for $30–$60 annually. It prevents the first at-fault accident from raising your rate.

-

Complete a state-approved defensive driving course. Many states and insurers offer a 5–10% discount for completing a course, which directly reduces your new premium and lowers the effective percentage increase.

-

Increase your deductible to offset part of the hike. Raising your auto deductible from $500 to $1,000 often saves $100–$150 per year. Just confirm you can cover the higher out-of-pocket cost if you file another claim.

-

Remove low-value add-ons like rental reimbursement or roadside assistance. These typically cost $5–$15 per month. Dropping them won’t erase a 40% increase, but it shaves a few percentage points and reduces the dollar impact.

-

Shop aggressively and don’t wait until renewal day. Start comparing quotes 30–45 days before your renewal date. This gives you time to verify coverage details, check insurer complaint ratios with your state regulator, make a switch without a coverage gap.

Most rate increases following an at-fault accident persist for three to five years. After that window, if you maintain a clean record, your rates typically drop back toward pre-claim levels. State notice requirements vary, but insurers generally must provide 30–60 days’ written notice before implementing a rate increase, giving you a realistic window to shop and switch if the new rate’s unacceptable.

Quick Reference Guide to Insurance Premium Percentage Calculations

The formula’s the same every time: (New Premium − Old Premium) / Old Premium × 100. Use it for renewals, mid-term adjustments, quote comparisons, multi-year trend analysis. Always work with the base premium amount. Exclude fees, taxes, installment charges so your percentage reflects the actual underwriting rate change, not billing add-ons.

When reviewing your renewal notice or quote, double-check the following:

- Confirm you’re comparing the same billing term. An annual premium vs. a six-month premium will produce a misleading percentage. Convert both to annual if needed.

- Verify the coverage limits and deductibles match. If your insurer reduced a limit or raised a deductible, the percentage change isn’t purely a rate increase. It’s a coverage change.

- Check for missing discounts. Multi-policy, good driver, other discounts sometimes drop off incorrectly, inflating the percentage increase.

- Look for itemized surcharges on the notice. Some insurers list accident surcharges or violation fees separately. Add those into the “New Premium” when calculating the true percentage increase.

- Ask the insurer to explain any increase above 25%. Regulators typically require justification for large hikes. The explanation might reveal an error or a factor you can address (like a recent credit-score drop you can dispute).

- Compare your calculated percentage against state or national averages. If your 60% increase is far above the state average for your situation, that’s a red flag to shop other insurers or file a regulatory inquiry.

Final Words

Use the formula (New − Old) / Old × 100 and run the numbers now. Do the manual math once, then double-check in a spreadsheet so you don’t confuse percent with percentage points.

This guide showed worked examples, exact Excel formulas, how to read the size and duration of increases, what drives them, and practical steps to reduce or appeal a hike.

Run the quick checklist and use how to calculate insurance rate increase percentage as your go-to test before you sign or dispute a renewal. You’ll be ready to act and avoid a costly surprise.

FAQ

Q: How do I figure out the percentage of a rate increase?

A: The percentage of a rate increase is (New − Old) ÷ Old × 100. Subtract, divide by the old premium, multiply by 100, round to two decimals, and don’t confuse percent with percentage points.

Q: How to calculate insurance rate?

A: To calculate an insurance rate, multiply the insurer’s base rate by your exposure (value or units) and apply adjustments for age, territory, claims, and discounts. Ask for a written rate breakdown from the insurer.

Q: What is the 50% rule in insurance?

A: The 50% rule usually means if repair costs exceed 50% of a property’s replacement cost, the claim is treated like a total loss for payout. State rules and policy language can change that—verify with your insurer.

Q: What is 20% NCB in insurance?

A: A 20% NCB (no-claim bonus) is a 20% discount on your renewal premium for remaining claim-free. It applies at renewal, varies by company, and is reduced or lost if you file a claim.

{kind=link}