Do you run a side business from home?

Your homeowners policy might still deny claims under its professional services exclusion.

That clause can turn a simple mistake into an expensive, uncovered legal fight.

This post explains what counts as a “professional service,” how common coverage gaps leave home-based workers exposed, and the practical checks and fixes to close the holes before you get sued.

Read on to protect your money, not just your house.

Understanding the Professional Services Exclusion in Homeowners Insurance

A professional services exclusion in a homeowners policy removes coverage for claims that come from doing professional work for someone else. Or failing to do it right. This clause blocks coverage when you’re giving advice, making a diagnosis, treating someone, or using professional judgment for other people. Whether you charged them or did it as a favor doesn’t always matter. The standard language reads: coverage is excluded for property damage or bodily injury “[a]rising out of the rendering of or failure to render professional services.”

Courts use a two-part test to figure out if something counts as “professional service.” First question: does the activity need specialized knowledge, labor, or skill? Second: is it mostly mental work instead of physical? In Stonegate Ins. Co. v. Smith (decided June 29, 2022), an Illinois court ruled that using a small propane torch to heat pipes during a shower valve replacement was mainly physical work, not professional. Even though plumbing can need specialized knowledge. The insured was a carpenter, not a plumber. He didn’t get paid. And the court kept its ruling narrow, limited to the specific facts about torch use. Ambiguous exclusions get read in your favor. But expect courts to stick close to the exact situation in front of them.

For you as a homeowner, this exclusion kicks in if you do any skilled work at home or for neighbors. Paid or not. If the work crosses from “helping out” into something that needs licensing, certification, or specialized training, and if it involves professional judgment or advice instead of simple manual labor, your homeowner policy might deny the claim. Insurers look at a few factors when deciding whether to use the exclusion:

- Does the activity need a professional license or certification?

- Is the work mostly intellectual (design, advice, diagnosis) or physical (hammering, lifting, digging)?

- Did you get paid, or was it part of a business or calling?

- Do you present yourself as qualified to do this service?

Common Professional Activities Excluded Under Homeowners Policies

Professional services exclusions typically deny coverage for consulting and management advice, legal representation or counsel, medical treatment or healthcare services, accounting and tax prep, financial planning or investment advice, and technical or software development you did for clients. These count as professional because they need specialized knowledge. They involve professional judgment. And the liability comes from the quality of advice or diagnosis, not just the physical work.

When you give advice, strategy, or skilled analysis to another person, and that advice causes financial loss, bodily injury, or regulatory trouble, the claim usually falls under professional liability instead of general personal liability. A tax preparer who makes an error that triggers an IRS penalty. A therapist doing telehealth from a home office whose patient claims harm from bad counseling. A freelance lawyer reviewing a contract from a home workspace and missing a critical clause. All face claims that homeowners policies will exclude. The insurer’s logic is simple: you were doing professional work, so the loss isn’t covered under a policy built for personal risk, not professional.

Typical excluded professions and activities:

- Consulting (management, HR, marketing strategy, IT advisory)

- Legal services (contract review, representation, legal opinions)

- Medical, dental, or therapeutic services (telehealth, counseling, physical therapy)

- Accounting, bookkeeping, and tax preparation

- Financial advisory, investment advice, and insurance sales

- Architectural, engineering, or design services that need certification

How the Professional Services Exclusion Creates Coverage Gaps for Home-Based Businesses

The professional services exclusion creates a sharp coverage gap for Americans running businesses from home. A standard homeowners policy is built for personal risks. Slip and fall injuries at a backyard barbecue. A tree falling on a neighbor’s fence. It’s not designed to cover client injuries during a business consultation, property damage caused by your product or service, errors in professional advice that lead to financial loss, damage to business equipment or inventory stored at your place, or cyber and privacy problems when you collect, store, or process client data from a home office.

Many insurers use revenue thresholds or physical markers to decide when a home activity has crossed into “business use.” Common triggers: clients or customers regularly visiting your place, keeping inventory or commercial-grade equipment at home, or hitting annual gross receipts above a certain number. Often cited in market practice as ranging from $2,500 to $25,000, though the exact number varies by carrier. Once you cross that line, even if your policy doesn’t explicitly exclude your activity by name, the professional services exclusion or a broader business pursuits exclusion will probably bar the claim.

The gap widens when you look at specific loss scenarios. A consultant whose client says bad strategic advice caused a failed product launch faces a professional liability claim. Excluded. A home baker whose customer has an allergic reaction triggers product liability. Often excluded or severely limited. A wedding photographer whose hard drive crashes, losing all ceremony images, faces a claim for negligent service delivery. Excluded. A virtual assistant who suffers a data breach exposing client credit card numbers faces regulatory fines and civil suits. Excluded. An accountant who misses a filing deadline, resulting in penalties. Excluded.

Common uncovered loss scenarios:

- Client claims financial loss due to your professional advice or error

- Client gets injured during a business meeting or service delivery at your home

- Your work product (software, documents, physical goods) causes third-party property damage

- Business equipment (computers, tools, inventory) gets stolen or destroyed

- Cyber incident exposes client data, triggering regulatory penalties and lawsuits

Differences Between Homeowners Liability and Business/Commercial Liability

Homeowners insurance is built for personal liability. Defending you when a guest trips on your stairs or your dog bites a neighbor. Typical personal liability limits range from $100,000 to $300,000, with some high-value policies offering $500,000 or $1,000,000. These policies explicitly exclude coverage for professional services, business activities, product liability (goods you make or sell), completed operations (liability after you finish a job), advertising injury, and most employment claims. The underwriting assumption is simple: you live there, you don’t operate a business there.

Commercial General Liability (CGL) policies flip that assumption. A CGL covers third-party bodily injury and property damage from your business operations, your products, and your completed work. Standard CGL limits are $1,000,000 per occurrence and $2,000,000 aggregate, though higher limits are common. CGL policies include coverage for advertising injury (libel, slander, copyright infringement in your ads), products and completed operations, and defense costs for business suits. They don’t, however, cover professional liability. Errors in your advice, diagnosis, or professional judgment. For that, you need a separate Professional Liability or Errors & Omissions (E&O) policy.

E&O policies are narrow: they cover claims alleging negligent acts, errors, or omissions in rendering professional services. Limits typically start at $100,000 to $250,000 per claim for very small practices, with $1,000,000 per claim being a common market benchmark for consultants, accountants, and therapists. E&O is claims-made coverage, meaning the claim must be made during the policy period (or an extended reporting period), not just the incident. E&O policies exclude bodily injury, property damage, and intentional acts. Those fall to CGL or other lines.

| Policy Type | Typical Limits | Coverage Scope |

|---|---|---|

| Homeowners (HO-3, HO-5) | $100,000–$500,000 personal liability | Personal risks; excludes business, professional services, products, completed operations |

| Commercial General Liability (CGL) | $1,000,000 per occurrence / $2,000,000 aggregate | Third-party injury/property damage from business operations, products, advertising; excludes professional liability |

| Professional Liability (E&O) | $100,000–$1,000,000 per claim | Errors, omissions, negligence in rendering professional services; excludes bodily injury and property damage |

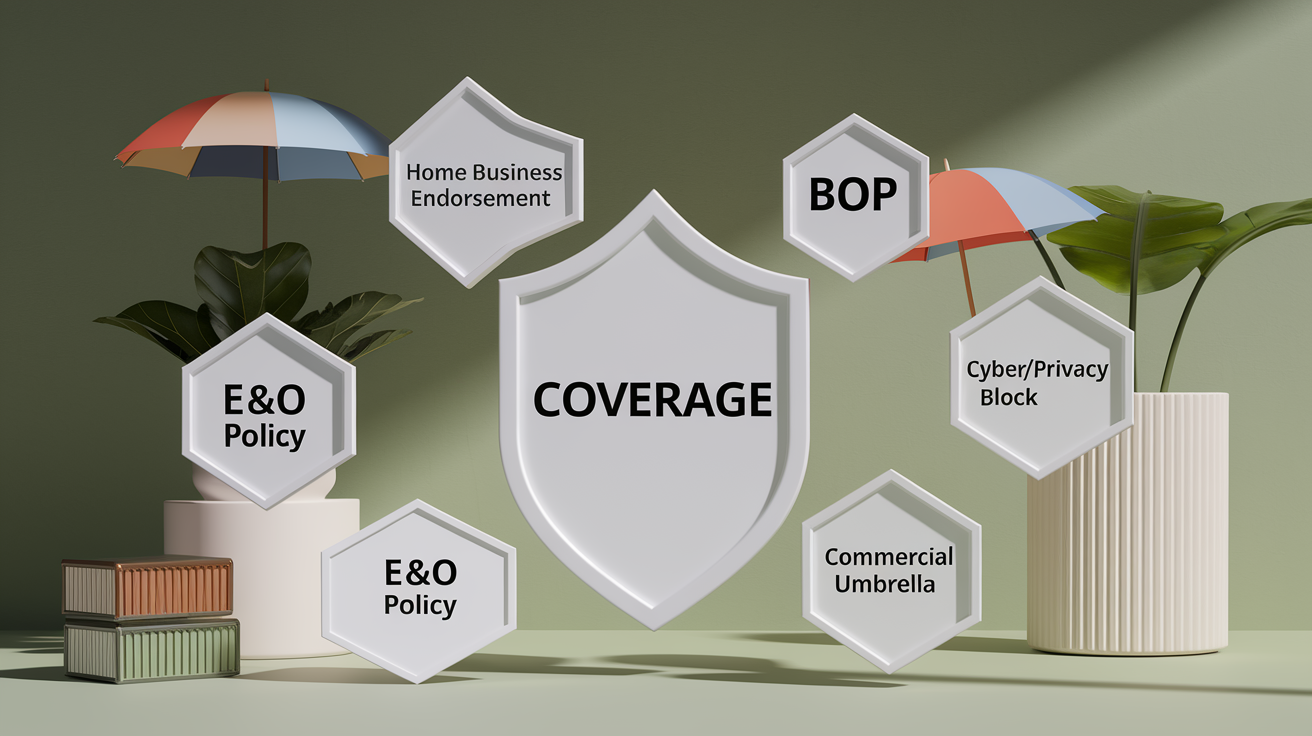

Insurance Options and Endorsements to Address Professional Services Exclusions

If you run a business from home, you’ve got several paths to close the coverage gap. The right one depends on your activity, revenue, whether clients visit, and the nature of your liability exposure. For very small, low-risk operations (think occasional tutoring, small craft sales on Etsy), a home-business endorsement added to your homeowners policy might work. These endorsements typically add limited liability (often $100,000 to $300,000) and a small amount of business personal property coverage (commonly $2,500 to $10,000) for an additional annual premium in the range of $50 to $300. Coverage is narrow. Many endorsements still exclude professional liability, and they cap coverage at low limits.

For businesses with moderate revenue, regular client contact, or inventory stored at the residence, a Businessowners Policy (BOP) is often the better fit. A BOP bundles Commercial General Liability, business property coverage, and business income (lost revenue if you can’t operate due to a covered loss) into one package. BOPs are designed for small, low-hazard businesses and typically carry $1,000,000 per occurrence / $2,000,000 aggregate liability limits, with property limits set to the value of your business equipment and inventory. Annual premiums for a small home-based BOP commonly range from $500 to $2,000, depending on your business class, revenue, and claim history.

If your work involves advice, professional judgment, or services that need certification, you need standalone Professional Liability or Errors & Omissions (E&O) coverage. E&O policies are tailored by profession. There are specific forms for accountants, consultants, therapists, IT professionals, and many other fields. Limits start at $100,000 per claim but commonly reach $1,000,000 per claim and $1,000,000 or $2,000,000 aggregate. Premiums vary widely: a solo consultant with $50,000 in revenue might pay $400 to $1,200 per year; a small accounting practice might pay $1,500 to $3,000. E&O is claims-made, so pay close attention to retroactive dates and tail coverage when you switch carriers or retire.

Two additional options round out the suite. If you handle client data (names, addresses, credit cards, health information), cyber liability and privacy insurance is critical. Cyber policies cover notification costs, credit monitoring, regulatory fines, and defense of privacy lawsuits. And if you need higher liability limits than your underlying CGL or E&O provides, a commercial umbrella policy can add $1,000,000 to $5,000,000 in excess coverage, sitting above your primary policies and kicking in once their limits are exhausted.

Common insurance solutions to address professional services exclusions:

- Home-business endorsement (limited liability and property for low-revenue, low-risk home operations)

- Businessowners Policy (BOP) combining CGL, property, and business income

- Professional Liability / Errors & Omissions (E&O) for advice-based and licensed services

- Cyber liability / privacy insurance for data breach and regulatory defense

- Commercial umbrella for additional liability limits above underlying policies

Real Case Insight: What Stonegate v. Smith Teaches About Professional Services Exclusions

In Stonegate Ins. Co. v. Smith, decided by an Illinois appellate court on June 29, 2022, the insured was a carpenter by trade who agreed to replace a shower valve as a favor for a neighbor in a multi-story townhouse. While heating pipes with a small propane torch, he caused a fire that spread to the second-story unit. The insurer filed a declaratory judgment action, arguing that the homeowners policy’s professional services exclusion barred any duty to defend or indemnify. The exclusion language was typical: coverage didn’t apply to property damage “[a]rising out of the rendering of or failure to render professional services.”

The court rejected the insurer’s argument. Applying the two-part test, the court assumed without detailed analysis that plumbing work could involve specialized knowledge or skill (prong one). But the court held that the specific act at issue (heating pipes with a torch) was predominantly physical and manual labor, not intellectual or professional judgment (prong two). The exclusion therefore didn’t apply. Critically, the court noted that the insured wasn’t a licensed plumber, received no compensation, and was performing the work as a one-time favor. Those facts likely influenced the outcome, and the court explicitly limited its holding to the narrow scenario of torch-heating pipes.

The Stonegate decision reinforces a core coverage principle: ambiguous exclusions get read against the insurer and in your favor. But it also shows that courts won’t stretch that principle beyond the specific facts. If the insured had been a licensed plumber, if he’d charged for the work, or if the claim had come from a design decision rather than manual execution, the court might have ruled differently. For you as a homeowner, the lesson is practical. Document the nature of the work, your qualifications, and whether you were paid. If the work is predominantly physical and you lack professional credentials, you might have an argument that the exclusion doesn’t apply. If you routinely perform the work for others, hold a license, or exercise professional judgment, expect the insurer to invoke the exclusion and prepare to get separate professional liability coverage.

How to Review Your Policy for Professional Services Language

Start by pulling your homeowners policy declarations page and the full policy form. Specifically the exclusions section of the liability coverage. Search for the phrases “professional services exclusion,” “business pursuits,” “arising out of the rendering of professional services,” “insured in the business of,” and “errors and omissions exclusion.” Insurers use different wording, but these phrases are common markers. If you find language that excludes coverage for damage arising from professional services or business activities, flag it and read the surrounding context. Some policies define “professional services” in the definitions section. Others leave the term undefined, relying on common understanding and case law.

Next, gather the facts of your own situation. Do you perform work at home for compensation? Do you hold a professional license or certification? Do clients, customers, or patients visit your residence for business purposes? Do you maintain inventory, tools, or equipment that you use in a trade or business? Do you exercise professional judgment, give advice, or diagnose conditions as part of your work? Write down your answers and any supporting documents: business licenses, contracts, revenue records, professional certifications. These facts determine whether your activity will trigger an exclusion and whether you need separate commercial or professional liability coverage.

Schedule a policy review with your insurance agent or broker at least one to two months before your renewal date. Bring your fact summary and ask specific questions. Does the policy exclude my business activity? If I add a home-business endorsement, what’s covered and what remains excluded? Do I need a separate BOP, CGL, or E&O policy? Can the carrier issue a manuscript endorsement to carve back coverage for my specific activity? Request written confirmation of coverage scope. Verbal assurances aren’t binding. If your carrier can’t or won’t provide adequate coverage, get quotes from commercial lines brokers who specialize in small business and professional liability.

Steps to review your homeowners policy for professional services language:

- Locate and read the liability exclusions section of your homeowners policy

- Search for key phrases: “professional services,” “business pursuits,” “rendering of,” “errors and omissions”

- Gather facts about your home-based work: licensure, revenue, client visits, equipment, advice provided

- List specific activities you perform and whether they are manual labor or professional judgment

- Schedule a policy review with your agent or broker 1–2 months before renewal, bringing your fact summary and asking for written clarification of coverage scope

Steps to Get Proper Business Coverage if You Work From Home

Before shopping for coverage, collect hard facts about your business. Document your annual gross receipts, the number of clients or customers you serve, whether clients visit your home or you work remotely, the value of business equipment and inventory kept at your residence, any professional licenses or certifications you hold, and sample client contracts or engagement letters. Insurers will ask for this during underwriting, and accurate disclosure is essential. Misrepresenting your business activities can void coverage when you need it most. If your gross receipts are modest (under $10,000 annually) and you have no employees, no inventory, and no client visits, a home-business endorsement might be enough. If you exceed those thresholds or if clients come to your residence, plan on a separate commercial policy.

Request quotes for the coverage types that match your exposure. If you sell products or provide services that could cause third-party injury or property damage, get a CGL quote (typically part of a BOP for small businesses). If you provide advice, consulting, design, or other professional services, get a standalone E&O or Professional Liability quote. Make sure the policy form is tailored to your profession (tech E&O, accountants’ professional liability, therapists’ malpractice, etc.). If you handle client data electronically, add a cyber liability quote. If you need higher limits than the underlying policies provide, request a commercial umbrella quote. Annual costs vary widely, but expect to pay $200 to $2,000 per year for a small BOP or E&O policy, and $100 to $500 for a modest cyber policy, depending on your revenue, claim history, and risk profile.

Timeline matters. Many endorsements and commercial policies take effect immediately, but underwriting can take days to weeks if the insurer requests additional information, inspections, or signed applications. To avoid a coverage gap, start the process one to two months before your homeowners policy renews. If you’re mid-term and have just started a business, contact your agent immediately. Don’t wait until renewal. Some homeowners policies require you to notify the insurer promptly of material changes in risk, and operating a business from the insured premises is almost always considered material.

Once you have quotes, compare not just price but coverage scope, exclusions, limits, deductibles, and whether the policy is occurrence or claims-made. Occurrence policies cover incidents that happen during the policy period, regardless of when the claim is filed. Claims-made policies (common for E&O) cover claims filed during the policy period for incidents that occurred after the policy’s retroactive date. Claims-made policies require careful management when you renew or switch carriers. Ask about tail coverage (extended reporting period) and nose coverage (prior acts) to avoid gaps.

Actionable steps to secure proper coverage for home-based business work:

- Collect documentation: annual revenue, licenses, client contracts, equipment value, number of client visits

- Determine if you need CGL, E&O, cyber, or a combination based on your specific business activities

- Request written quotes from commercial lines agents or brokers, not just verbal estimates

- Compare policy forms for exclusions, limits, deductibles, and occurrence vs claims-made structure

- Disclose all business activities accurately on applications to avoid coverage disputes later

- Implement coverage 1–2 months before homeowners renewal or immediately if you start a business mid-term

Checklist for Homeowners Running a Business From Home

If you perform any paid work from home, or even unpaid skilled work that could trigger a liability claim, use this checklist to confirm you have proper coverage. Work through each item at least annually, ideally two months before your homeowners policy renews, and any time you change the nature or scale of your business activity.

- Identify and list all business activities you perform from home, including services, products sold, and advice provided

- Determine whether clients, customers, or patients visit your residence for business purposes

- Calculate annual gross receipts and compare to your insurer’s business-use thresholds (commonly $2,500–$25,000)

- Inventory business property and equipment kept at home and note current replacement value

- Review your homeowners policy exclusions for “professional services,” “business pursuits,” and related clauses

- Verify whether you hold professional licenses, certifications, or credentials that define your work as a professional service

- Obtain quotes for a home-business endorsement, BOP, CGL, or E&O policy depending on your exposure

- Compare liability limits across policies (confirm $1,000,000 per occurrence for CGL and $1,000,000 per claim for E&O as baseline targets)

- Assess whether you need cyber/privacy coverage if you collect, store, or process client data electronically

- Schedule an annual insurance review with your agent or broker 1–2 months prior to renewal and document coverage decisions in writing

Final Words

If you run work from home, check your policy now. This post defined the professional services exclusion, listed common excluded activities, and showed how gaps pop up for home-based businesses.

We compared homeowners limits to commercial options and walked through fixes — endorsements, BOP, E&O, umbrella — plus the Stonegate case showing courts can side with the insured when work is manual.

Read your policy language, get answers in writing, and consider the right endorsement. Ask your agent about the professional services exclusion homeowners so your coverage actually works when you need it.

FAQ

Q: What is a professional services exclusion?

A: A professional services exclusion is a homeowners policy clause that denies coverage for claims resulting from providing or failing to provide professional services. Insurers look for specialized knowledge and mostly intellectual work; courts often favor the insured.

Q: What are some examples of professional services?

A: Some examples of professional services include legal advice, tax or accounting work, medical or therapy services, financial planning, consulting and technical/software services, and paid client work like commercial photography done from home.

Q: What are the common exclusions in a homeowners policy?

A: Common exclusions in a homeowners policy include professional services and business activities, vehicle-related liability, intentional acts, wear-and-tear, and standard perils like flood and earthquake that need separate policies.

Q: What does E&O not cover?

A: Errors and omissions (E&O) insurance does not cover bodily injury or property damage claims, intentional misconduct, first-party property loss, or broad commercial risks better covered by general liability or property policies.

{kind=link}