Think your insurer is on your side? Think again.

When a denial cites a policy exclusion, the clock is running and you can lose the right to appeal.

This guide gives clear, step-by-step actions to fight that exclusion: read the denial, get the full policy, gather records, build a timeline, demand the claim file, and write a tight appeal letter.

You’ll learn what evidence matters, common gotchas insurers use, internal and external review routes, and exactly what to ask for so you don’t waste your appeal window.

Immediate Steps for Challenging Policy Exclusions in a Denied Claim

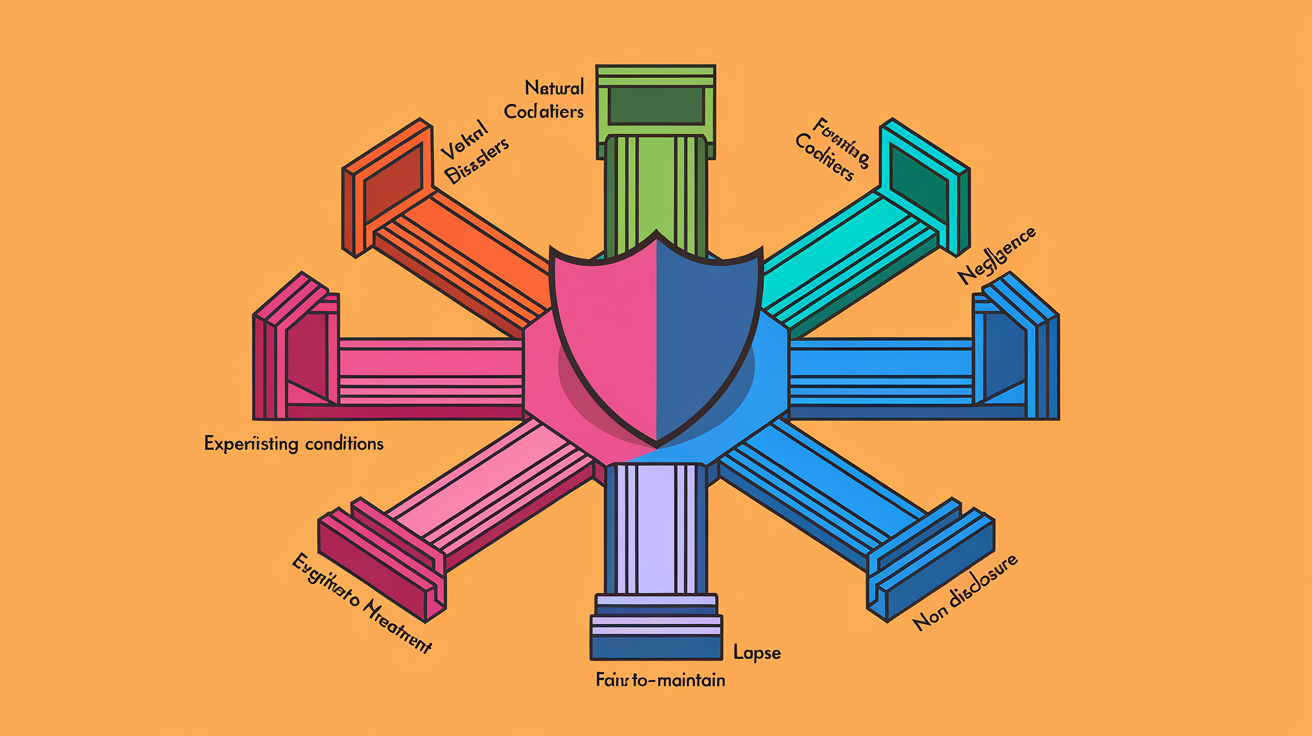

Most claim denials come down to one thing: an adjuster matched your situation to an exclusion somewhere in the policy. Insurers are supposed to pay valid claims. But exclusions give them legal exits. Natural disasters, pre-existing conditions, missed payments, property maintenance issues, illegal conduct, experimental treatments, and stuff you didn’t disclose when you bought the policy. These seven triggers account for most denials.

Once you get that denial letter, the clock’s running. Most insurers and state laws give you somewhere between 30 and 180 days to appeal. Miss that window and you’re done. Read the denial letter twice. Note which exclusion they cited, the denial date, and any appeal instructions or deadlines. Then dig out your full policy. Declarations page, exclusions, definitions, endorsements. All of it. Don’t rely on memory or summaries. Exclusion language is technical. One word can flip the whole thing.

Timely documentation makes or breaks these fights. Adjusters and appeals reviewers look for gaps, inconsistencies, missing proof. If you wait weeks to gather records or follow up, they’ll assume you don’t have a case. Document every phone call. Save every email. Track every submission.

Six things to do first:

-

Get the full denial letter in writing. If they denied you over the phone, request a written copy citing the exact policy exclusion, section number, and factual basis.

-

Gather all records related to the incident. Health claims: medical records, prescriptions, test results, doctor’s notes. Property claims: photos, repair estimates, inspection reports, receipts. Auto claims: police reports, accident photos, witness statements.

-

Compare the policy language to what actually happened. Read the exclusion word by word. Does the policy define the excluded event narrowly? Does your situation actually match that definition, or is the insurer stretching things?

-

Build a timeline. Include when you bought the policy, when the incident happened, when you filed, when they denied you, and any relevant history (maintenance work, doctor visits, premium payments).

-

Send questions to the adjuster in writing. Ask for the claim file, investigative reports, and a detailed explanation of how they applied the exclusion to your specific facts. Request copies of any internal notes or third-party reports.

-

Request your complete claim file. They have to provide it. It often reveals assumptions, errors, or missing evidence you can challenge in an appeal.

Understanding Policy Exclusion Language and How It Is Interpreted

Exclusion clauses are written by insurers. They’re supposed to be clear. Legally, an exclusion must be conspicuous, plain, and unambiguous to hold up. If the language is vague or buried in dense text, courts often rule it’s unenforceable. Insurers like broad exclusion language because it gives them more room to deny claims. But that same breadth can backfire. If the policy says “illegal acts” without defining what qualifies, a court may read it narrowly in your favor.

The legal principle is called contra proferentem: ambiguous policy language gets interpreted against the insurer. If two reasonable interpretations exist, the one favoring coverage wins. There’s also the “reasonable expectations” doctrine. Courts will honor what a reasonable consumer would expect the policy to cover, even if the fine print says otherwise.

How Insurers Must Prove an Exclusion Applies

The insurer carries the burden of proof. They must show, with evidence, that your claim falls squarely within the exclusion. For first-party claims (where you’re filing for your own loss), you must first show the event falls within basic coverage. Then the insurer must prove a specific exclusion applies. For third-party claims (where someone else is making a claim against your policy), the insurer’s burden is even higher. They must prove the exclusion applies under every reasonable interpretation of the facts.

This creates openings. If the insurer relies on assumptions (“we think this was pre-existing,” “it looks like neglect”) without hard evidence, their exclusion argument fails. If they conduct a shallow investigation, skip witness interviews, ignore your submitted records, or misread medical timelines, you can challenge the denial on procedural grounds. Insufficient investigation is a common reason exclusion-based denials get reversed.

Evidence and Documentation Required to Challenge Policy Exclusions

Evidence is the foundation here. Adjusters and appeals reviewers don’t take your word for it. They want records, reports, photos, expert opinions, timelines. The more documentation you provide, the harder it is for the insurer to dismiss your claim on vague or speculative grounds.

Start by collecting everything the adjuster should have reviewed but may have ignored. Pre-existing condition disputes hinge on medical records that establish onset dates. Property neglect allegations fall apart when you produce maintenance invoices and inspection reports. Allegations of illegal conduct or negligence can be rebutted with police reports, toxicology results, or witness statements showing the insurer’s theory doesn’t match the facts.

Eight critical pieces of evidence to gather:

- Complete policy document, including declarations page, endorsements, exclusions section, and definitions section.

- Declarations page, showing coverage amounts, effective dates, and premium payment history.

- Medical records, including office visits, test results, hospital records, prescription history, and any records predating the policy effective date if you’re challenging a pre-existing condition exclusion.

- Complete claim file from the insurer, including adjuster notes, investigative reports, third-party evaluations, and internal correspondence.

- Proof of loss documentation, such as itemized repair estimates, receipts for expenses already paid, or sworn statements of loss submitted during the claim process.

- Photos and inspection reports, documenting the condition of property before and after the incident, or showing maintenance work that rebuts neglect allegations.

- Expert reports, such as independent medical opinions, forensic engineers’ assessments, accident reconstructionists’ findings, or toxicology interpretations that contradict the insurer’s conclusions.

- Timeline worksheet, listing policy purchase date, incident date, claim filing date, all communications with the insurer, denial date, and all applicable deadlines for appeals or external review.

Writing an Effective Appeal Letter to Dispute an Exclusion

An appeal letter is your formal, written argument that the exclusion doesn’t apply. It must cite specific policy language, attach supporting evidence, and request a clear action: reverse the denial and pay the claim. A vague, emotional letter without citations or documentation will be ignored.

Start by identifying the exact exclusion clause the insurer cited. Quote the policy section, number, and language verbatim. Then explain, point by point, why the exclusion doesn’t fit your facts. If the policy excludes “intentional acts” but the incident was accidental, cite the police report, witness statements, and any forensic evidence showing lack of intent. If the exclusion applies to “experimental treatment” but your procedure is FDA-approved and widely accepted, attach clinical guidelines, your doctor’s letter, and insurance billing codes showing standard-of-care status.

After you submit the appeal, follow up in writing every 10 to 14 days. Request status updates, ask for confirmation that your evidence was reviewed, and note any new deadlines or next steps. Keep a log of every communication. Send appeals by certified mail or another traceable method so you have proof of receipt.

Four essential components of every appeal letter:

- Policy citation: Quote the exclusion clause verbatim, including section and page number, and cite any relevant definitions from the policy.

- Evidence summary: List and attach all supporting documents (medical records, photos, expert reports, timelines) and explain how each piece contradicts the insurer’s exclusion argument.

- Alternative causation theory: If the insurer says the loss was caused by an excluded event, present a competing explanation supported by records. For example, “The damage was caused by wind, a covered peril, not flood, an excluded peril, as shown by the engineer’s report.”

- Explicit request for reversal: State clearly that you’re requesting the insurer reverse the denial and pay the claim in full, and specify a reasonable deadline for their response.

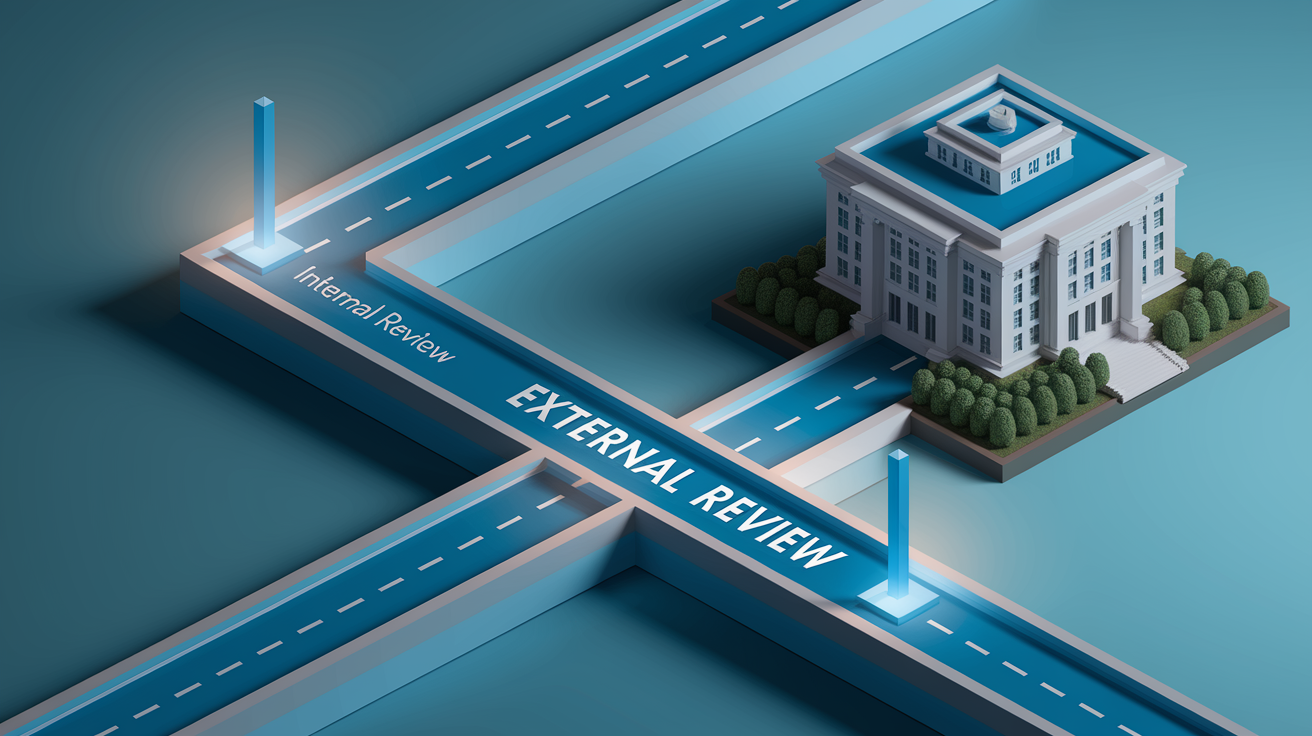

Internal and External Appeal Processes for Reversing Exclusion-Based Denials

After your initial appeal letter, the insurer will route your case through internal review. This typically involves a supervisor or appeals unit that wasn’t involved in the original denial. Internal review can take 30 to 60 days, and the insurer must respond in writing. If they uphold the denial, ask for the name and title of the reviewer, the date of the review, and a detailed written explanation of their decision.

If internal review fails, escalate to senior management or the insurer’s ombudsman if one exists. Some carriers have consumer affairs divisions or policyholder advocates whose job is to resolve disputes before they reach external review or litigation. Document every escalation step, and track response times. If the insurer misses its own deadlines or state-mandated response windows, note it in your complaint file.

When internal options are exhausted, or if the insurer is unresponsive, move to external dispute resolution. This is where your documentation and timelines become critical, because external reviewers rely on the written record you’ve built.

External Review and State-Level Complaints

Most states offer some form of external review for insurance disputes. You can file a complaint with your state insurance department or commissioner. The department will investigate, request the claim file from the insurer, and issue a finding or facilitate mediation. Complaints are usually free to file. Insurers take them seriously because repeated complaints can trigger regulatory scrutiny or fines.

External review bodies (sometimes called independent review organizations) are neutral third parties that evaluate whether the insurer’s exclusion decision was correct. For health insurance, many states mandate external review for medical necessity and experimental treatment disputes. For property and auto claims, external review is less common, but arbitration or appraisal clauses in the policy may provide a binding dispute resolution path. Check your policy for arbitration requirements and deadlines, and consider whether arbitration is faster and cheaper than litigation or if it limits your legal options.

Legal Theories Used to Challenge Insurance Policy Exclusions

When appeals and external review fail, legal action may be necessary. Courts analyze exclusion disputes using several well-established doctrines. If the exclusion language is ambiguous, courts apply contra proferentem and interpret it in favor of coverage. If the insurer conducted an inadequate investigation or ignored evidence, courts may find the denial was arbitrary or in bad faith. If the insurer’s interpretation of the exclusion conflicts with the reasonable expectations of the policyholder, courts may rule the exclusion unenforceable.

Bad faith claims go beyond simple contract disputes. If the insurer denied your claim knowing the exclusion didn’t apply, delayed the investigation without justification, or refused to pay after the exclusion argument collapsed, you may have grounds to sue for bad faith. Successful bad faith claims can result in payment of the original claim plus consequential damages, attorney fees, and in some states, punitive damages.

| Legal Theory | How It Helps Challenge an Exclusion |

|---|---|

| Contra Proferentem | Ambiguous exclusion language is interpreted in favor of the policyholder; if two reasonable readings exist, coverage is favored. |

| Reasonable Expectations Doctrine | Courts honor what a reasonable consumer would expect the policy to cover, even if exclusion language is technically present. |

| Insufficient Investigation / Bad Faith | If the insurer denied the claim without adequate evidence or ignored policyholder-submitted proof, the denial may be reversed and damages awarded. |

| Declaratory Judgment Action | Policyholder files suit asking the court to declare whether the exclusion applies; shifts the dispute from administrative appeals to judicial review. |

Common Exclusion Types Consumers Successfully Challenge

Seven exclusion categories drive most denials, and each contains built-in vulnerabilities. Natural disaster exclusions (floods, earthquakes, hurricanes) are often misapplied when the true cause of loss is wind or rain, both typically covered perils. Pre-existing condition exclusions fail when medical records show the condition was diagnosed after the policy effective date or when the insurer can’t prove the condition existed before coverage began. Negligence or illegal conduct exclusions require proof of intent or criminal activity, not just assumptions or arrests.

Lapsed policy exclusions get used when the insurer claims you missed premium payments. But if you can show timely payment or that the insurer failed to send proper notice, the lapse argument collapses. Failure-to-maintain-property exclusions are common in homeowners claims, but maintenance records, invoices, and inspection reports often prove routine upkeep occurred. Specific treatment exclusions (experimental or elective procedures) are frequently overturned when the treatment is FDA-approved, medically necessary, or widely accepted as standard care. Non-disclosure exclusions require the insurer to prove you intentionally withheld material information and that the information would have changed the underwriting decision.

Each of these exclusion types relies on the insurer making factual assumptions. Your job is to produce records that prove the assumptions are wrong.

Why These Exclusions Are Often Misapplied

Adjusters work under tight timelines and handle hundreds of claims. They rely on checklists, automated systems, and cursory reviews of submitted evidence. When an exclusion looks like it might apply, many adjusters deny first and investigate later. They assume you won’t appeal. Or that you lack the documentation to fight back.

Misapplication happens most often when causation is ambiguous. Was the roof damage caused by wind (covered) or flood (excluded)? Was the overdose accidental (covered) or intentional (excluded)? Did the medical condition exist before the policy (excluded) or develop after (covered)? Insurers frequently choose the excluded interpretation without conducting the deeper investigation required to prove it. If you can produce an independent expert report, a detailed timeline, or records the adjuster never requested, you shift the burden back onto the insurer to prove their exclusion theory is correct.

When to Hire Legal Counsel to Fight an Exclusion Denial

Hire an attorney when the claim value justifies the cost, when the insurer’s denial relies on speculation rather than evidence, or when you’ve exhausted internal appeals and need to escalate to litigation, arbitration, or external review. Legal help is also critical when the insurer alleges you committed fraud, withheld information, or engaged in illegal conduct. Those allegations carry reputational and legal risks beyond the claim itself.

Many consumer attorneys who handle insurance disputes work on contingency, meaning they take a percentage of any recovery and charge nothing if you lose. Typical contingency fees range from 25% to 40%, depending on whether the case settles or goes to trial. Confirm the fee structure, costs, and scope of representation in writing before signing a retainer agreement.

Three circumstances that require legal involvement:

- High claim value or large policy limits: When the denied claim exceeds $50,000, or when the insurer’s denial exposes you to significant out-of-pocket costs, hiring counsel ensures you have the resources to fight a prolonged dispute.

- Insurer relies on incomplete investigation or speculation: If the denial letter cites assumptions, ignores your submitted evidence, or lacks specific factual support for the exclusion, an attorney can demand the full claim file, depose the adjuster, and challenge the denial on procedural and substantive grounds.

- You face allegations of fraud, misrepresentation, or criminal conduct: These allegations can void your policy, trigger rescission, or expose you to legal liability beyond the claim. Legal counsel is essential to protect your rights and reputation.

Final Words

If your claim was denied for an exclusion, act fast: get the denial letter, compare it to your policy, and gather records and photos. Start the internal appeal and keep a tight timeline.

Remember how exclusion language is interpreted — ambiguities can help you, and the insurer must prove the exclusion applies. Write a focused, evidence-backed appeal and don’t be shy about escalating to an external review or counsel if needed.

For practical next steps on how to challenge policy exclusions, use the checklist here and stay persistent. You increase your chance of a reversal.

FAQ

Q: Can you appeal an insurance plan exclusion?

A: You can appeal an insurance plan exclusion by immediately getting the denial letter, comparing the exclusion language to your loss, collecting supporting records, requesting the claim file, asking for internal review, and escalating if needed.

Q: What not to say to the insurance adjuster?

A: Don’t tell the insurance adjuster you caused the damage, guess about details, give inconsistent statements, accept a quick low offer, or agree to a recorded statement without checking your rights or getting legal advice.

Q: How would you explain policy exclusions to a customer?

A: Explain policy exclusions to a customer as specific situations the insurer won’t pay for; name examples, show definitions, point out common traps, and tell them to review the exact clause and gather proof to dispute it.

Q: What are the two main reasons for denying a claim?

A: The two main reasons for denying a claim are that the loss fits a policy exclusion, and that the claimant lacks proof or eligibility—like non-disclosure, lapsed coverage, or insufficient medical or property evidence.

{kind=link}