Think Uber or Lyft will always cover you if you crash while working? Think again.

Rideshare insurance changes depending on whether the app is off, you’re waiting for a ping, or you’ve accepted a trip.

States set hard minimums, and companies fill some gaps, but not all.

This post explains the three coverage phases, the state rules you need to follow (like Texas and Florida), the common gaps that leave drivers on the hook, and the exact questions to ask your insurer before you hit the road.

Core Coverage Standards Every Driver Must Meet for Rideshare Insurance

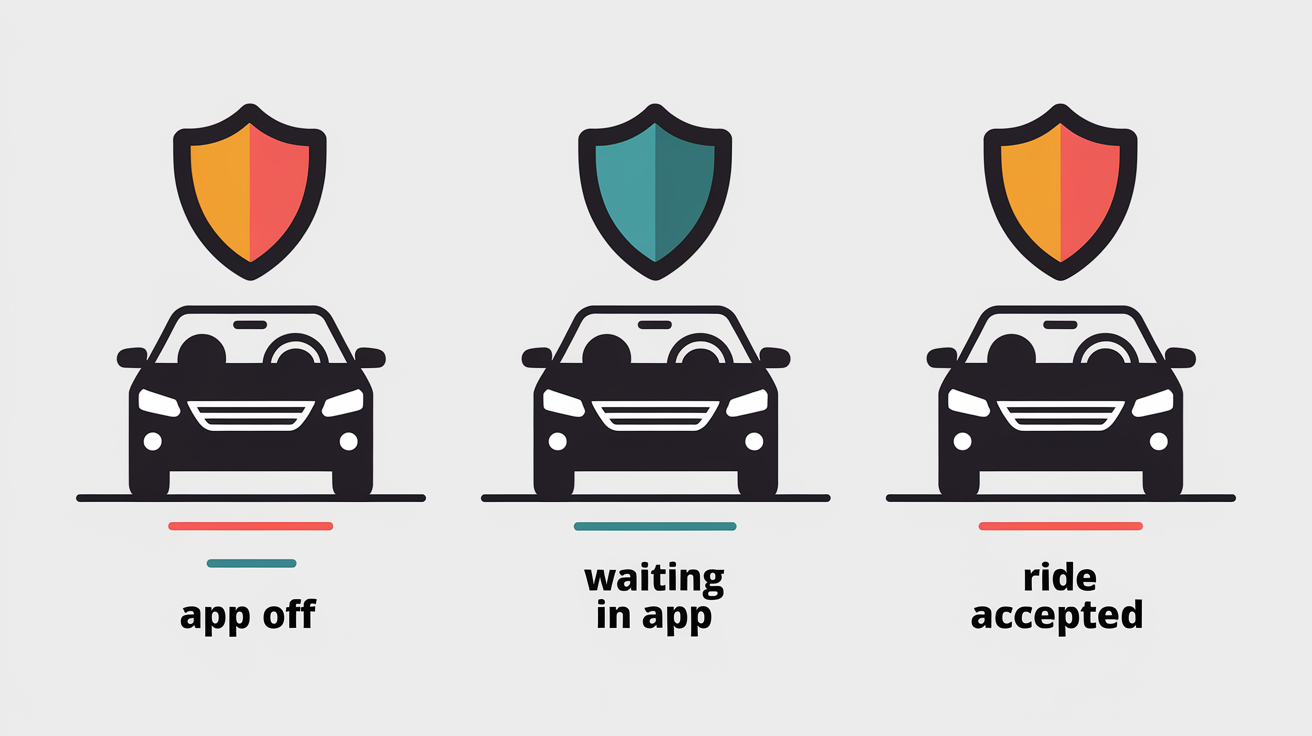

Rideshare insurance requirements flip completely based on what you’re doing with the app. App off? Your personal policy is all that’s standing between you and financial disaster. Log in and start waiting for pings, different coverage kicks in. Accept a trip and get a passenger in your car, you’re suddenly under a third layer of insurance.

States set minimum coverage floors that Uber, Lyft, and the rest must provide, or that you’ve got to carry yourself. These aren’t friendly suggestions. They’re legal requirements. Drive without them and you can end up personally liable for damages running into six figures. Texas spells it out in Insurance Code §1954.051. Florida has its own statutory minimums, plus a no fault system that throws personal injury protection into the mix.

Here’s how the three phases break down in states like Texas and Florida:

App off: Only your personal auto insurance covers you. In Florida, that’s at least $10,000 in personal injury protection (PIP) and $10,000 in property damage liability (PDL). Texas doesn’t require PIP, so your personal liability limits are what you’ve got.

Logged in, waiting for a ride request: Most states require $50,000 per person and $100,000 per accident in bodily injury coverage, plus $25,000 in property damage. Texas law sets bodily injury minimums at $50,000 per person and $100,000 per incident during this waiting period.

Ride accepted or passenger on board: Coverage jumps to $1,000,000 in liability, provided by the rideshare company. Covers bodily injury to third parties and property damage. In Texas, this phase also includes mandatory uninsured and underinsured motorist (UM/UIM) coverage.

Contingent comprehensive and collision: If you carry comp and collision on your personal policy, the rideshare company provides backup coverage for your vehicle during active trips. Don’t have comp and collision? The rideshare company won’t cover damage to your car, even mid trip.

Most drivers think the rideshare company covers everything once they flip on the app. Not even close. The waiting phase is where gaps open up. The offline phase is entirely on you.

How Insurers Determine Which Policy Applies in a Rideshare Claim

When you file a claim after a rideshare accident, the first question the insurer wants answered is simple: “What were you doing when the crash happened?” That answer determines which policy pays and which one walks away. If you were logged in but hadn’t accepted a ride, your personal insurer might deny the claim, saying you were engaged in commercial activity. Just dropped off a passenger and turned off the app? The rideshare company’s policy might not apply either.

Evidence matters here. Insurers don’t take your word for anything. They want proof of your exact status at impact. Can’t prove which phase you were in? The claim sits in limbo while two insurers argue over responsibility. You’re stuck in the middle. Here’s what insurers use to verify which policy applies:

App activity logs: The rideshare company’s internal system records when you logged in, accepted a ride, picked up the passenger, and ended the trip. These timestamps are the primary evidence in most phase disputes.

Ride receipts and platform records: If a trip was active, the passenger has a receipt. Trip hadn’t started yet? No receipt exists. Insurers request these records directly from Uber or Lyft, but you can pull your own trip history from the app.

Phone records and GPS data: If app logs are incomplete or disputed, insurers may request phone records to verify when the app was open and where your phone was located. Photos taken at the scene, timestamped by your phone, can establish the timeline.

The insurer’s job is to pay the smallest claim it legally can. Any ambiguity about which phase you were in? Expect a fight. That’s why documenting app status right after a crash, before you even move the car, can save you months of back and forth with adjusters.

State Level Rideshare Insurance Rules Drivers Must Follow

Every state sets its own rideshare insurance rules. Some states go way further than others. Texas and Florida both have specific statutes spelling out minimum coverage requirements for rideshare drivers, but the details differ. Other states rely on a patchwork of regulations, guidance from insurance commissioners, or voluntary agreements with Uber and Lyft.

Texas is clear. The state’s Insurance Code §1954.051 lists exact coverage amounts rideshare companies must provide. Florida treats rideshare drivers under its broader Transportation Network Company (TNC) framework, which also requires minimum coverage but adds PIP because Florida is a no fault state. A few states, like New York and California, go further, requiring higher liability limits or additional driver protections.

If you drive in multiple states, you need to know the rules in each one. Coverage that’s legal in Louisiana might not meet the bar in Texas. Here’s how Texas and Florida compare:

| State | Waiting Phase Minimums (logged in, no ride accepted) | Active Trip Minimums (ride accepted or passenger on board) |

|---|---|---|

| Texas | $50,000 per person BI / $100,000 per accident BI / UM/UIM required | $1,000,000 liability / UM/UIM required |

| Florida | $50,000 per person BI / $100,000 per accident BI / $25,000 PD | $1,000,000 liability / contingent comp/collision if driver has comp |

| Other States | Varies; check state insurance department or TNC regulations | Typically $1,000,000 liability; UM/UIM and contingent coverage rules vary |

Some states don’t publish clear TNC insurance rules at all. In those places, the rideshare company’s policy usually fills the gap, but that doesn’t mean it meets your state’s minimum auto insurance requirements when you’re offline or waiting. Check your state insurance department’s website or ask your insurer directly. Don’t assume Uber or Lyft will tell you what’s legally required. They’re not your insurance agent.

The Gap Between Personal Auto Policies and Rideshare Requirements

Most personal auto insurance policies were written before rideshare existed. They explicitly exclude coverage for commercial activity. That means the moment you turn on the Uber or Lyft app, your personal policy may stop covering you, even if you’re just sitting in a parking lot waiting for a ping. This is the gap that catches drivers off guard.

The waiting phase is the danger zone. You’re logged in and available, but you haven’t accepted a ride yet. The rideshare company provides some liability coverage during this phase, usually $50,000 per person and $100,000 per accident. But that’s often less than your personal policy’s limits, and it may not cover damage to your own car at all. If your personal insurer denies the claim because you were app on, and the rideshare company’s policy doesn’t cover your vehicle, you’re stuck paying out of pocket.

Here are the most common coverage gaps that leave rideshare drivers exposed:

Waiting for a ride request: Your personal policy excludes app on activity, but the rideshare company’s waiting phase coverage doesn’t include comp or collision for your car.

Immediately after passenger exit: You’ve ended the trip in the app, but you’re still parked near the drop off. Some policies treat this as “offline,” leaving you uncovered if you’re hit in the next 60 seconds.

Personal policy cancellation: Some insurers will cancel your personal policy entirely if they discover you’re driving for Uber or Lyft without telling them, even if you never filed a rideshare related claim.

Contingent comp/collision limits: The rideshare company’s backup coverage for your vehicle only applies if you already carry comp and collision. Dropped those coverages to save money? There’s no backup at all.

State minimum personal policies: If your personal liability coverage is just your state’s minimum (often $25,000 to $50,000), and your personal insurer denies a claim because you were app on, you’re relying entirely on the rideshare company’s lower waiting phase limits.

A rideshare endorsement is the simplest fix. It’s an add on to your personal auto policy that fills the waiting phase gap, covering your car and liability even when you’re logged in but haven’t accepted a ride. Not every insurer offers one. Some will refuse to cover rideshare drivers at all. If your current insurer won’t help, shop around. Several national carriers now offer rideshare specific policies or endorsements.

Rideshare Company Coverage: What Uber and Lyft Actually Provide

Uber and Lyft provide insurance, but it’s not the same as your personal policy, and it doesn’t cover every situation. Their coverage is built around the three phases of rideshare activity. What they provide in each phase is spelled out in their insurance disclosures and state filings. The problem? Most drivers never read those disclosures, and the coverage isn’t always as broad as it sounds.

During the waiting phase, when you’re logged in and available but haven’t accepted a ride, Uber and Lyft typically provide $50,000 per person and $100,000 per accident in bodily injury liability, plus $25,000 in property damage coverage in states like Florida. In Texas, the bodily injury minimums are $50,000 per person and $100,000 per incident, and the company must also provide uninsured and underinsured motorist coverage. This waiting phase coverage is contingent, meaning it only applies if your personal policy doesn’t cover the accident. Personal insurer denies the claim? The rideshare company’s policy steps in.

Once you accept a ride and you’re either on your way to pick up the passenger or the passenger is in your car, coverage jumps to $1,000,000 in liability. This covers bodily injury to the passenger, other drivers, pedestrians, and property damage. It also includes uninsured and underinsured motorist protection in Texas. Third parties injured by your negligence can make a claim against this $1,000,000 policy. Passengers in your car are also covered.

Here’s what Uber and Lyft require before their contingent comprehensive and collision coverage applies during an active trip:

You must carry comprehensive and collision coverage on your personal auto policy.

Your personal policy must be active and in good standing at the time of the accident.

The accident must occur while a ride is accepted or a passenger is on board, not during the waiting phase.

Don’t have comp and collision? The rideshare company will not cover damage to your vehicle, even if the accident happens mid trip and wasn’t your fault. That’s a costly surprise for drivers who dropped those coverages to lower their monthly premium. The rideshare company’s policy protects passengers and third parties. It’s not designed to protect your car unless you’re already protecting it yourself.

Costs, Rate Factors, and How to Select the Right Rideshare Insurance

Rideshare endorsements and commercial rideshare policies cost more than basic personal auto insurance, but the price spread is wide. Some drivers pay an extra $10 or $15 per month. Others see their premium jump by several hundred dollars a year. The difference comes down to how much you drive, where you drive, your vehicle, and your insurance company’s appetite for rideshare risk.

A rideshare endorsement, an add on to your existing personal policy, is usually the cheapest option if your insurer offers one. It fills the waiting phase gap and often includes comp and collision coverage while you’re logged in. A full commercial rideshare policy costs more, but it provides higher liability limits and broader coverage across all three phases. Drive more than 20 hours a week or rely on rideshare income to pay your bills? Commercial coverage is often worth the extra cost.

Here are the six biggest factors that determine how much you’ll pay for rideshare insurance:

Driving frequency and hours per week: More time on the road means more risk. Insurers price accordingly. Drivers who log 40+ hours a week pay significantly more than casual weekend drivers.

Where you drive: High traffic urban areas, cities with high accident rates, and regions with expensive medical costs all push premiums higher.

Vehicle type and value: Insuring a new SUV costs more than insuring a seven year old sedan. Comprehensive and collision premiums are tied directly to your car’s replacement cost.

Your driving record: Accidents, tickets, and claims in the past three to five years increase your rate. A clean record qualifies you for safe driver discounts.

Coverage limits you choose: Minimum state limits are cheaper, but many drivers buy $250,000 to $1,000,000 in liability coverage to protect personal assets. Higher limits mean higher premiums.

Deductibles: Choosing a $1,000 deductible instead of a $250 deductible lowers your monthly cost, but you’ll pay more out of pocket after an accident.

Shop around. Not every insurer writes rideshare policies, and pricing varies wildly. Get quotes from at least three carriers. Ask specifically about rideshare endorsements, not just commercial policies. Some companies that won’t insure full time rideshare drivers will cover part time drivers with an endorsement. If you’re turned down, ask why. Sometimes it’s your driving record, sometimes it’s just company policy.

Filing Claims After a Rideshare Accident and Proving Proper Coverage

Filing a rideshare insurance claim is more complicated than filing a normal auto claim because three policies might be involved: your personal policy, your rideshare endorsement or commercial policy, and the rideshare company’s policy. Which one applies depends entirely on what you were doing when the accident happened. You’ll need proof.

The insurance company’s first move is to figure out whether they owe you anything. Offline? Your personal insurer handles it. Waiting for a ride? The rideshare company’s contingent waiting phase policy might apply, but only if your personal insurer denies coverage. On a trip? The rideshare company’s $1,000,000 policy should cover it, but they’ll verify your app status first. Insurance companies will look for any reason to shift responsibility to another policy, so your documentation needs to be airtight.

Here’s the step by step process for filing a rideshare insurance claim and protecting your right to coverage:

Document app status immediately after the crash: Before you talk to anyone, open your rideshare app and take a screenshot showing whether you’re offline, waiting, en route, or on a trip. App crashed or your phone broke? Write down your last known status and the time.

Collect all evidence at the scene: Get photos of vehicle damage, the other driver’s insurance card, witness contact information, and the exact location. Were you on a trip? Ask the passenger for their name and confirm the ride is logged in your trip history.

Pull app logs and trip receipts as soon as possible: Log into your Uber or Lyft driver dashboard and download your trip history. Trip was active? Save the receipt showing pickup and drop off times. Were you waiting? Note the timestamp when you last accepted a ride.

Report the accident to the correct insurer first: On a trip? Contact the rideshare company’s insurance team (Uber and Lyft both have dedicated claim phone lines and online portals). Offline? Call your personal insurer. Waiting? You may need to file with both and let them sort out who pays.

Do not sign anything until you understand what policy applies: Adjusters will ask you to provide recorded statements, sign medical releases, and authorize access to your phone records. Don’t sign or agree to anything until you know which policy is covering the claim and whether you’re being offered a fair settlement. If the claim is disputed or the injuries are serious, talk to an attorney before you sign.

Phase disputes are common. Insurers will argue over timestamps, app logs, and whether you’d truly ended a trip or were still “available.” If the rideshare company’s records show you were offline but you swear you were logged in, you’ll need phone records, GPS data, or witness statements to prove it. The burden of proof is on you. Keep records, keep receipts, and keep copies of everything you send to an insurer.

Final Words

If you’re driving—logged out, waiting, or on a trip—know this: coverage changes with your app status and the biggest risk is when you’re logged in but waiting. We covered the three coverage phases, state minimums (Texas and Florida), and what Uber and Lyft supply.

We also explained how insurers decide which policy pays, common gaps in personal policies, what endorsements cost, and the evidence you need for a claim.

Check your policy, ask for written confirmation of rideshare limits, and confirm rideshare insurance requirements with your insurer. You’ll be safer.

FAQ

Q: What kind of insurance do I need for rideshare?

A: The kind of insurance you need for rideshare is your personal auto policy plus a rideshare endorsement or commercial coverage; TNCs often provide contingent liability, commonly $50,000/$100,000 waiting and $1,000,000 during trips.

Q: Can I do Uber without rideshare insurance?

A: You can drive for Uber without a separate rideshare policy, but you risk claim denial if your personal policy excludes app-on activity; get a rideshare endorsement or confirm Uber’s contingent coverage before driving.

Q: Is rideshare insurance more expensive?

A: Rideshare insurance is usually more expensive than a standard policy, typically adding a small annual increase to several hundred dollars; cost depends on driving frequency, vehicle type, and driving record.

Q: Can I DoorDash without rideshare insurance?

A: You can DoorDash without a rideshare endorsement in many places, but personal policies often exclude delivery while the app is on; get a delivery endorsement or confirm the platform’s contingent coverage before accepting orders.

{kind=link}