Insurance promises often end with the five words that sink claims: “this policy does not cover.”

Those are policy exclusions — the contract’s hard no.

They decide what your insurer will refuse to pay even when you desperately need help.

This post cuts through the legal language to show what exclusions look like, where they’re hidden in a policy, and the common gotchas that wipe out claims.

Read on to learn who should worry, which exclusions matter most, and the three checks to avoid a nasty surprise at claim time.

Clear Explanation of Policy Exclusions and How They Work

A policy exclusion tells you exactly what your insurer won’t pay for. When you see “this policy does not cover,” you’re reading an exclusion. These aren’t suggestions. They’re the parts of your contract that draw hard lines around what’s protected and what isn’t.

Exclusions work like legal stop signs inside your policy. They don’t hint at what might not be covered. They give the insurer explicit permission to say no, even when your loss feels devastating or urgent. If what happened to you falls under an exclusion, the company can point to that clause and refuse to pay. That’s why exclusions matter more than almost anything else in your policy.

You won’t find all your exclusions in one tidy section. The Declarations page might flag a few big ones upfront. There’s usually a section called “Exclusions” where most of the denial language lives. But definitions matter just as much, because they tell you what words like “flood” or “wear and tear” actually mean in this contract. And endorsements? Those can quietly add new exclusions or change old ones. Skip any of these and you’re setting yourself up for a nasty surprise at claim time.

Here are some exclusions you’ll see all the time:

- Flood damage in homeowners policies

- Anything you did on purpose

- Pre-existing conditions in older health plans (mostly gone since 2014)

- Cosmetic procedures

- Normal aging, rust, rot, things breaking down over time

Common Insurance Policy Exclusions Across Major Policy Types

Homeowners policies cut out risks that would destroy affordability if they were included by default. Flood and earthquake damage almost never show up in standard coverage. You need separate policies for those, either through the National Flood Insurance Program or private companies. Maintenance problems get excluded too. Mold, termites, worn-out roofs, rotting wood? Not covered. The insurer’s position is simple: you could’ve prevented it, so it’s on you. Intentional damage, nuclear events, and war are also out. If your roof leaks because you ignored missing shingles for three years, that’s a textbook exclusion.

Auto policies exclude risky use and deliberate acts. Racing your car, doing stunts, or using your personal vehicle for commercial deliveries without the right coverage? Excluded. Crash it on purpose? No payout. Normal mechanical failures aren’t covered unless you bought a breakdown endorsement. And if someone drives your car who isn’t listed on the policy or who you specifically excluded to lower your premium, that accident might not be covered either. A transmission dying after years of hard use? That’s wear and tear, not an insured loss.

Health insurance cuts out elective and experimental stuff. Cosmetic surgery, fertility treatments, and investigational procedures usually aren’t covered unless your plan says otherwise. Before the Affordable Care Act, insurers could refuse to cover pre-existing conditions. Federal rules mostly killed that practice in 2014 for individual and group plans. Dental and vision often get excluded from base medical coverage. You need separate policies for those.

Travel insurance has gotten pickier post-pandemic. Pandemics, epidemics, wars, terrorism (unless you buy it back), government travel bans, extreme sports, and pre-existing conditions are commonly excluded unless you pay for a waiver. After COVID, lots of travel insurers added explicit pandemic language to shut down future claims. Ignore a government travel warning and your trip cancellation claim might get tossed.

| Insurance Type | Examples of Exclusions |

|---|---|

| Homeowners | Flood, earthquake, mold, maintenance, wear and tear |

| Auto | Racing, intentional damage, commercial use, mechanical breakdown |

| Health | Cosmetic procedures, experimental treatments, elective care |

| Travel | Pandemics, war, high-risk activities, government travel bans |

Why Policy Exclusions Exist and How They Shape Coverage

Insurers use exclusions to decide what they’ll cover and how much to charge. Without them, every policy would have to cover everything, and premiums would be impossibly high. Exclusions let insurers carve out the stuff that’s too risky, too expensive, or too predictable, then either refuse it completely or sell it separately at a different price.

They also stop moral hazard. That’s insurance-speak for “people behaving badly because they’re insured.” If policies covered intentional damage, some folks might wreck their own stuff for a payout. Excluding that behavior keeps fraud down and premiums lower for everyone else.

There are four big reasons exclusions exist:

- Keep catastrophic or wildly unpredictable risks off the table (pandemics, nuclear disasters, war)

- Avoid paying for maintenance and aging, which you can control

- Stay legal (some risks can’t be insured by law)

- Keep base premiums affordable by slicing off high-cost scenarios

How Exclusions Affect Claims and Why Denials Occur

When you file a claim, the insurer checks two things: does the loss fit what’s covered, and does an exclusion apply? If your situation matches an exclusion, the claim gets denied or cut down, even if it seems like something insurance should obviously handle. Your basement floods in a storm? Homeowners policy says no, because flood damage is excluded. The insurer doesn’t care how bad you need the money. It cares what the contract says.

In claims where you’re reporting your own loss, you have to show the event fits basic coverage. Then the insurer has to prove an exclusion applies. And that exclusion has to be clear, visible, and understandable. If it’s hidden in tiny print, written in gobbledygook, or contradicts something else in the policy, a court might refuse to enforce it. Vague exclusions usually get read in your favor.

Arguments happen when exclusion language is fuzzy or when important words aren’t defined. Say your policy excludes “wear and tear” but doesn’t explain what that means. Your roof collapses after years of deferred fixes. Was it sudden (covered) or gradual (excluded)? You and the insurer will fight about it. Missing definitions and overly broad wording create disputes and lawsuits.

Here’s what triggers most exclusion-based denials:

- Intentional acts or crimes by you or someone on your policy

- Excluded perils like flood or earthquake when you didn’t buy separate coverage

- Cosmetic or elective health procedures

- Maintenance neglect, aging, rust, decay

- Using your personal car for business without commercial coverage

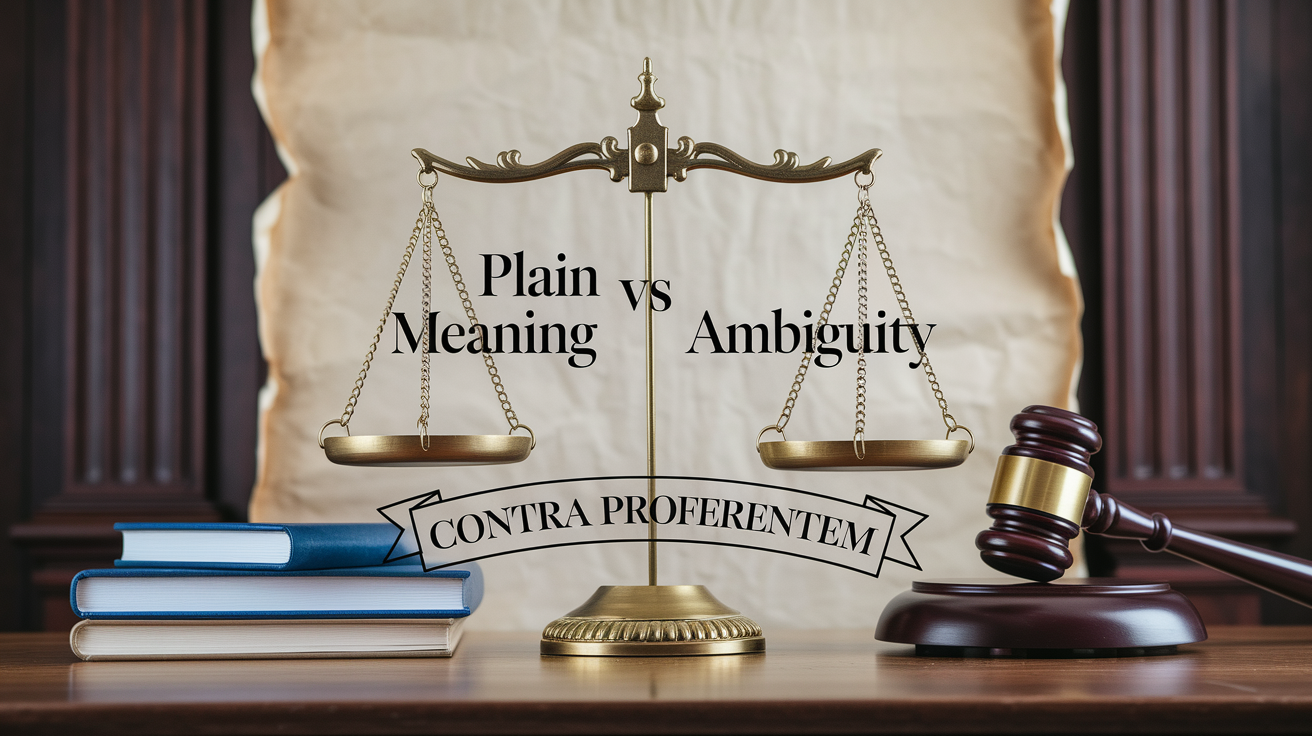

Interpreting Policy Exclusion Language and Understanding Legal Standards

Courts don’t just rubber-stamp every exclusion an insurer writes. Judges use rules designed to protect you from buried traps and one-sided contracts. The starting point is plain meaning. If the exclusion says “flood,” the court asks how a normal person would understand that word, not how the insurer wants it understood. Clear language gets enforced as written.

But when exclusion language is ambiguous (it can reasonably mean two different things), courts use a rule called contra proferentem. That’s Latin for “against the drafter.” Since insurers write policies, unclear terms get interpreted in your favor. If an exclusion could mean “sudden water damage” or “all water damage,” and the policy doesn’t clarify, the narrower version usually wins.

Plain Meaning vs Ambiguity Rules

Plain meaning interpretation requires everyday language a regular person can understand. Vague phrases like “related losses” or “arising out of” cause problems when the link between the exclusion and your claim isn’t obvious. Your house gets smoke damage from a wildfire. The policy excludes “pollution” but doesn’t define it. The insurer says smoke is pollution. A court will ask whether normal people call wildfire smoke pollution.

Burden of Proof for First-Party vs Third-Party Claims

In first-party claims (you’re reporting your own loss), once you show the loss happened and fits basic coverage, the insurer has to prove the exclusion applies. And the exclusion has to be clear and easy to spot. In third-party claims (someone says you caused harm and your liability policy kicks in), the insurer’s job gets harder. Courts require proof the exclusion works “in all possible worlds.” That means every version of the facts has to support the exclusion. If there’s any plausible story where coverage exists, the insurer has to defend the claim.

How Courts Apply Consumer Protection Doctrines

Some courts use the reasonable expectations doctrine. It says coverage should match what a reasonable buyer would expect based on ads, agent conversations, and how the policy is structured, even if exclusion language technically says otherwise. You bought “comprehensive” auto coverage and the agent never mentioned hitting a deer isn’t covered. A court might toss the exclusion because it contradicts what you reasonably expected. This varies by state and shows up more in consumer cases than business ones.

Modifying, Removing, or Buying Back Exclusions

Lots of exclusions aren’t set in stone. Insurers sell endorsements, riders, or separate policies that add coverage back for excluded stuff. You pay more, sometimes with new deductibles, but you close the gap. Flood and earthquake coverage almost never come standard in homeowners policies. You can buy standalone flood insurance through the National Flood Insurance Program or private carriers, and earthquake endorsements from your homeowner insurer or a specialty company. This lets you tailor coverage to your actual risks.

Business policies let you negotiate or buy back exclusions more easily. A standard policy might exclude cyber incidents. You can add a cyber liability endorsement covering data breaches, ransomware, and notification costs. Pollution exclusions can be narrowed or removed with a pollution liability rider. If you sign contracts that make you liable for stuff, a contractual liability endorsement covers those obligations, which are otherwise excluded.

Health and auto policies offer limited modifications too. Some health plans let you add vision, dental, or alternative medicine coverage that’s normally excluded. Auto policies may offer mechanical breakdown coverage to fill the wear and tear gap. Adding coverage raises your premium, but it kills a potential denial scenario.

You’ve got four ways to deal with exclusions:

- Buy endorsements or riders from your current insurer to narrow or kill specific exclusions

- Purchase separate standalone policies for excluded stuff like flood, earthquake, or cyber risk

- Negotiate exclusion wording when buying or renewing, especially for business coverage

- Add umbrella or excess liability coverage that might fill gaps left by your base policy

How to Find and Read the Exclusions in Your Insurance Policy

Start with your Declarations page. It lists your policy number, limits, deductibles, and often flags key exclusions or endorsements. Then go to the section labeled “Exclusions” or “What Is Not Covered.” That’s where most denial language lives, usually in numbered or bulleted lists. Don’t stop there. Check the Definitions section, because terms like “flood,” “business use,” or “experimental treatment” get defined narrowly in ways that make exclusions bigger than they look.

Review the Conditions section and any Endorsements stapled to your policy. Conditions sometimes sneak in exclusion-like rules, such as “we won’t pay if you don’t report the loss within 30 days.” Endorsements can add new exclusions or change old ones. If you’ve got five endorsements and you skip them, you might miss a new pandemic exclusion or a change to where your coverage applies.

Watch for vague or undefined terms, overly broad categories like “all water damage” without details, exclusions buried in long paragraphs instead of clearly listed, and contradictory language where one section seems to cover what another excludes. Spot any of these? Get written clarification from your agent or insurer before you file a claim.

Use this when reviewing exclusions:

- Read the Declarations page, Exclusions section, Definitions, Conditions, and all Endorsements

- Highlight exclusions that match risks you actually face (flood zone, home business, chronic illness)

- Look for undefined terms or squishy language like “related to” or “arising out of”

- Note exclusions that conflict with what your agent said or what ads promised

- Ask your insurer for written explanations of anything unclear

- Request a list of available endorsements or riders with premium quotes in writing

Frequently Asked Questions About Policy Exclusions

Does an exclusion always mean my claim will be denied?

Not always. If the exclusion’s worded poorly, wasn’t disclosed right, or conflicts with other policy language, you might be able to fight it. Courts read unclear exclusions in your favor.

Can I negotiate exclusions before I buy a policy?

Sometimes. Commercial policies and high-value personal coverage (like umbrella or specialty homeowners) often allow negotiation or endorsements. Standard consumer policies are less flexible, but you can ask about riders or separate coverage.

What should I do if I discover an exclusion that affects me after buying the policy?

Call your agent or insurer right away. Get written confirmation of the exclusion and what options exist to add coverage. If the exclusion wasn’t disclosed when you bought and contradicts what you were told, document those conversations and think about talking to a lawyer.

When should I hire a lawyer to review exclusions?

When you’re facing a big denied claim, when exclusion language is unclear or contradicts what an agent said, or when the denial seems to ignore policy terms or case law in your state. Insurance dispute attorneys can tell you whether an exclusion is actually enforceable.

Are exclusions the same across all insurance companies?

No. Lots of exclusions are standard (flood, intentional acts, wear and tear), but wording and scope vary. One company’s mold exclusion might be absolute. Another’s might apply only to mold from long-term neglect. Always compare exclusion lists when shopping.

Final Words

In the action: this post defined policy exclusions, showed where they appear, and gave clear examples by policy type.

You saw how exclusions shape claims, the legal rules courts use, and practical ways to modify or buy back coverage.

Read your policy with the checklist, flag vague wording, and ask for written answers.

If you can answer what does policy exclusion mean for your own plan, you’ll avoid nasty surprises and pick coverage that actually works when you need it.

FAQ

Q: What is an example of a policy exclusion?

A: An example of a policy exclusion is flood damage; many homeowners policies exclude floods. Other common exclusions include intentional acts, pre-existing conditions, cosmetic procedures, and wear-and-tear.

Q: What is an exclusion policy?

A: An exclusion policy is a clause that lists perils, items, or situations an insurer will not cover; it defines which claims the insurer can deny or limit under your contract.

Q: What is the purpose of policy exclusions?

A: The purpose of policy exclusions is to limit insurer risk and keep premiums affordable by removing high volatility or uninsurable perils, like floods or intentional acts, from standard coverage.

{kind=link}