Think your personal auto policy will cover work trips? Think again.

The business use exclusion can strip coverage the moment your car’s used for work and leave you paying medical bills, repairs, and legal fees out of pocket.

This isn’t rare. One uncovered crash can cost tens of thousands and wreck your future premiums.

In this post, I’ll show what the exclusion actually blocks, how coverage limits matter, common traps like rideshare and contractor driving, and the quick checks to avoid a denial.

Core Explanation of the Business Use Exclusion

The business use exclusion in a personal auto policy kicks coverage to the curb when your car’s being used for work. Personal auto insurance gets priced around everyday private driving. Commuting to your regular job, weekend errands, family road trips, hitting up friends. When the car shifts into business mode, the risk picture changes completely. Drivers using vehicles for work rack up more miles, make more stops, haul cargo or people for money, and spend way more time in congested areas. Insurers see that as a different animal from personal driving and won’t cover it without a separate business policy or add-on.

Most standard personal policies include clear language that kicks out coverage when you use the vehicle “for business purposes,” “in the occupation, profession, or business of the insured,” or “for transporting goods or passengers for a fee.” Wording shifts by carrier and state, but the intent’s the same. Personal coverage stops when the vehicle goes to work. Insurers apply this broadly. Liability, collision, comprehensive, uninsured motorist, medical payments—all of it can vanish during a business trip.

The exclusion protects the insurer’s pricing model. Business driving pumps up both how often claims happen and how bad they get. Drivers who spend most of their miles on work face way higher accident rates. Published claims data show collision rates for heavy business drivers run 30–40% higher than private drivers, and drivers spending over 80% of annual mileage on work trips are 50% more likely to crash. Without the exclusion, insurers would underprice the risk and everyone’s premiums would go up to cover the shortfall. Instead, carriers price personal and commercial separately, each tied to its own risk bucket.

Common excluded business activities:

- Driving to meet clients or customers as part of your job

- Delivering goods, packages, food, or equipment for pay

- Transporting passengers for money through rideshare or taxi apps

- Hauling work tools, materials, or inventory to job sites regularly

What Insurers Consider Business Use

Insurers define business use as any driving that directly supports commercial activity, generates income, or fulfills job requirements beyond a standard commute. It’s broader than most drivers think. It’s not just vehicles owned by businesses or titled as commercial. Personal cars driven by self-employed people, gig workers, and employees running work errands can all trigger the exclusion if the activity fits the insurer’s definition. Carriers look at trip purpose, not job title or employment status.

Commuting from home to a regular fixed workplace usually counts as personal use, even though it’s work related. Most policies accept that regular commuting is part of life and bake those miles into personal pricing. The line moves when the driving itself becomes the work. Running errands during the day, visiting clients, delivering stuff, transporting people for pay. That’s when insurers call it business. The distinction trips people up because it hinges on the nature of the trip, not the driver’s intent or how often it happens. Even one delivery for pay during an otherwise personal drive can shove that trip into the business category.

Insurers typically flag these as business use:

- Making multiple work stops during the day, like sales calls or service appointments

- Transporting clients, co-workers, or business contacts for work

- Delivering goods or documents as part of a job or side gig

- Using the car to haul equipment, supplies, or inventory to and from sites

- Running a rideshare or delivery app, whether a passenger or order’s in the car or not

Real-World Examples: Rideshare, Delivery, and Contractor Driving

Rideshare and delivery driving create some of the biggest coverage gaps. When you log into Uber, Lyft, DoorDash, or similar platforms, your personal policy typically stops covering you right then. This kicks in even if you’re just waiting for a request and haven’t picked up a passenger or package yet. The app tells the insurer the vehicle’s now available for commercial hire, which lands squarely in the business use exclusion. Lots of drivers think their personal policy covers them until they accept a trip. Most carriers say the exposure starts the second the app goes live.

Contractors and tradespeople hit similar walls when they use personal vehicles to move tools, materials, or equipment to job sites. A plumber driving to a client’s house with pipes and a toolbox in the trunk is doing business. If an accident happens during that trip, the insurer can deny the claim because the vehicle was in business use when the loss occurred. Same goes for general contractors, electricians, landscapers, and freelancers treating their cars as mobile workshops. Even if the business is small or the trips are occasional, the exclusion can stick as long as the insurer can show the vehicle was working when the crash happened.

Salespeople, real estate agents, and consultants who visit clients or job sites during the workday also trip the exclusion. Driving from the office to meet a client for a pitch, showing a property, dropping off documents to a business partner—all business activities. Mixing personal errands into the same trip doesn’t bring coverage back. The insurer looks at the primary reason for the drive, and if the work stop is why you’re out there, the exclusion applies. One accident during a client visit can leave you without liability, collision, or medical payments coverage because the trip got classified as business.

Examples that split covered from excluded:

- Covered: driving to the grocery store on a Saturday afternoon

- Excluded: driving to the grocery store to grab catering supplies for a business event you’re hosting

- Covered: commuting from home to your employer’s office every morning

- Excluded: driving from the office to meet a client at a coffee shop during your workday

Consequences of Violating the Business Use Exclusion

When you use a personal vehicle for business and an accident happens, the insurer can deny the whole claim. That denial can wipe out liability coverage for injuries and property damage you caused, collision coverage for repairs to your car, medical payments for your passengers, and uninsured motorist coverage if the other driver has nothing. The denial isn’t a penalty. It’s the insurer using the policy terms. If the exclusion language is clear and the facts show the vehicle was in business use at the time, courts usually back the denial. You’re then personally on the hook for everything. The other party’s medical bills, vehicle repairs, legal fees if you get sued, and the cost to fix or replace your own car.

Insurers investigate business use after accidents, especially when the claim’s big or the circumstances smell like commercial activity. They review statements from the driver and passengers, check the vehicle for business equipment or signage, pull employment records, request phone logs or app data if rideshare or delivery’s suspected, and compare the loss location and time with what you said about vehicle use on the application. If the investigation turns up undisclosed business use, the insurer can deny the claim even if you thought you were covered. Lying about vehicle use on an insurance application can also trigger policy rescission, where the insurer cancels coverage retroactively and refunds premiums, leaving you uninsured from day one.

Beyond claim denial, ongoing business use of a personal vehicle can get your policy canceled or not renewed once the insurer finds out. Carriers run periodic checks, and if they discover you’re using the car for excluded business, they can cancel mid-term for material misrepresentation or just not renew when the term ends. A cancellation for misrepresentation makes it harder and pricier to get coverage elsewhere. Drivers who lose coverage this way often end up in the high-risk or non-standard market, where premiums can run two to three times higher than standard personal rates. The financial and legal exposure from a single uncovered accident, plus the cost of future insurance, can easily hit tens of thousands of dollars.

Coverage Alternatives When You Use Your Personal Car for Work

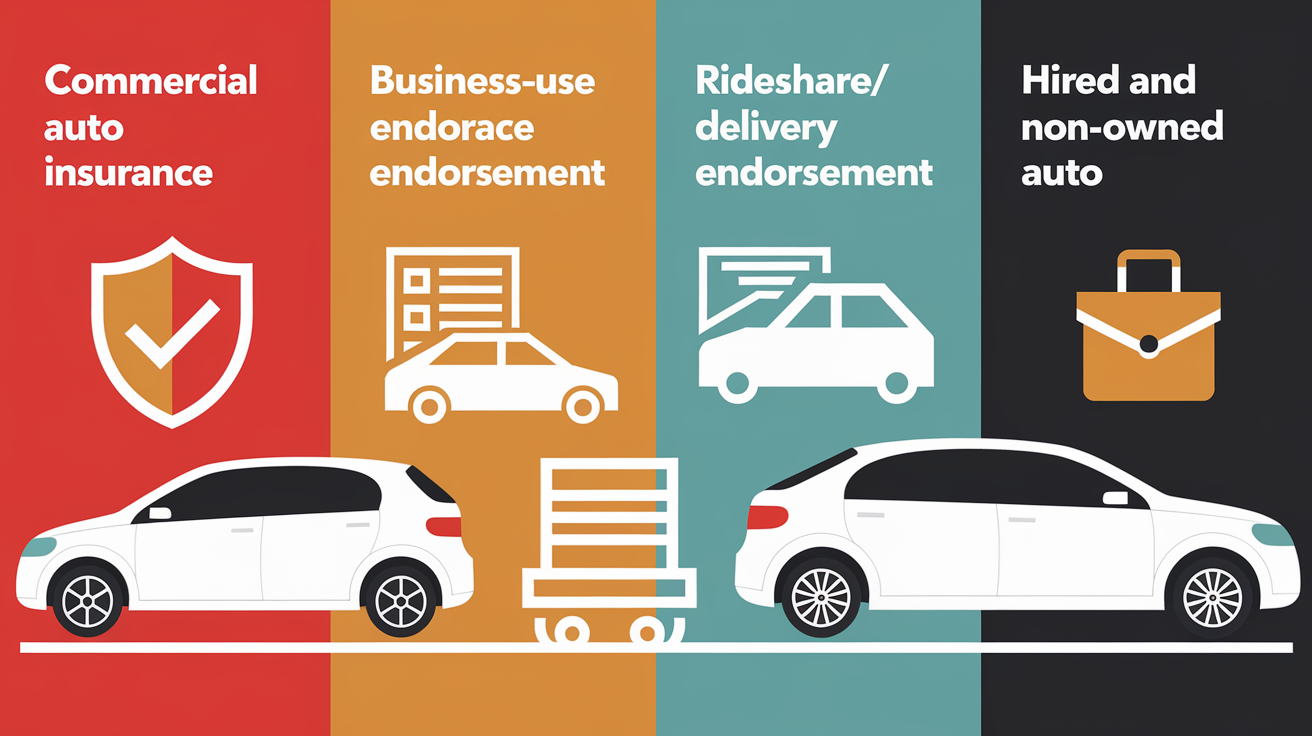

If you use your personal vehicle for any business activity, you need coverage built for that use. The most common options are commercial auto insurance, business-use endorsements, rideshare or delivery endorsements, and hired and non-owned auto insurance. Each addresses different levels of business activity and covers what a standard personal policy excludes. Picking the right one depends on how often you use the car for work, whether you transport goods or passengers, and whether the vehicle’s owned by you personally or a business entity.

| Coverage Type | Applies To | Key Benefit |

|---|---|---|

| Commercial Auto Insurance | Vehicles used regularly for business, deliveries, client transport, or owned by a business | Broad liability protection, higher limits, coverage for cargo and equipment, multiple authorized drivers |

| Business-Use Endorsement | Occasional or light business driving (client visits, errands) on a personally owned vehicle | Adds limited business-use coverage to a personal policy; typically costs under $100/year |

| Rideshare/Delivery Endorsement | Drivers who use rideshare or delivery apps (Uber, Lyft, DoorDash, etc.) | Fills gaps while app is active but before passenger/order is accepted; coordinates with platform coverage |

| Hired and Non-Owned Auto (HNOA) | Businesses whose employees use personal vehicles for company errands or tasks | Covers business liability when an employee is driving their own car; does not cover damage to employee’s vehicle |

Commercial auto insurance is the full-coverage answer for anyone relying on a vehicle for daily business operations. It gives you higher liability limits (often starting at $1 million combined single limit instead of the $100,000/$300,000 split common in personal policies) and covers business-specific risks like cargo damage, tools and equipment, and legal defense if the business gets sued after an accident. Commercial policies also let you list multiple drivers and can cover vehicles titled to a business entity, which personal policies can’t touch. For self-employed contractors, delivery businesses, and any operation where the vehicle’s a primary asset, commercial auto isn’t optional.

Guidance for Gig Workers and Self-Employed Drivers

Gig workers face some of the biggest coverage gaps under personal auto policies. Rideshare drivers, food delivery couriers, freelance delivery services, platform-based workers. Lots of drivers jump into gig work assuming their personal insurance will kick in if something goes wrong, only to find out after a crash that the claim got denied. The business use exclusion applies the second the app turns on, and most personal policies explicitly exclude any driving for pay or while available for hire. Rideshare and delivery platforms provide some coverage, but it’s usually limited to specific periods (like only while a passenger’s in the car or an order’s being delivered), leaving drivers exposed during wait time or while driving to pick someone up.

Self-employed people who use personal vehicles for client visits, deliveries, equipment transport, or any income-generating activity need to figure out whether their personal policy includes business use or if they need a commercial policy or endorsement. Sole proprietors, independent contractors, freelancers, and small business owners often think occasional business use is fine as long as the vehicle’s titled in their name. That assumption gets expensive. If you drive to meet clients, haul materials, deliver products, or use your car as a mobile office, your personal auto insurer can deny your next claim and cancel your policy. The misclassification risk runs highest among self-employed workers because they control how the vehicle gets used and might not see the line between personal errands and business.

Practical steps for gig and self-employed drivers:

- Tell your insurer about your gig or business activity before you start driving commercially. Not disclosing can void coverage entirely.

- If you drive for rideshare or delivery platforms, ask your carrier if they offer a rideshare or delivery endorsement and what periods of app use it covers.

- Compare the cost of adding a business-use endorsement (often under $100/year) against the risk of a denied claim and out-of-pocket liability.

- Confirm that any platform-provided insurance coordinates with your personal or endorsed policy and understand which coverage is primary during each phase of a trip.

Final Words

Check your policy now: the business use exclusion can wipe out coverage the moment you drive for work. This article defined the exclusion, showed what insurers call business driving, and listed the common excluded activities.

We walked through real examples — rideshare, delivery, contractor work — the claim-denial and cancellation risks, plus fixes like endorsements, rideshare add-ons, and commercial policies.

If you drive for pay, ask for written proof from your insurer. Understanding the business use exclusion personal auto policy prevents surprise bills and keeps you covered when it matters.

FAQ

Q: Does my personal auto policy exclude business use?

A: The personal auto policy typically excludes business use: insurers will deny claims for work-related driving like deliveries, client rides, or tool hauling unless you add a business-use endorsement or buy commercial coverage.

Q: Can I buy a vehicle for my business and use it for personal use?

A: You can buy a vehicle for your business and still use it personally, but the insurer and tax rules matter: insure it commercially and track personal use, because mixing uses can affect coverage, claims, and deductions.

Q: What is excluded in a personal auto policy?

A: A personal auto policy excludes most business activities: carrying paying passengers, deliveries and courier work, transporting tools or inventory, towing trailers for work, and rideshare or gig driving.

Q: Can my business pay for my personal car insurance?

A: Your business can pay your personal car insurance, but paying doesn’t change coverage: if you use the car for work without proper commercial coverage or endorsement, claims may be denied and liability could fall on you or the business.

{kind=link}