Who would you rather face after a disaster: a locked door or a cheap check?

Insurers use two tools that look similar but act very differently: exclusions and limitations.

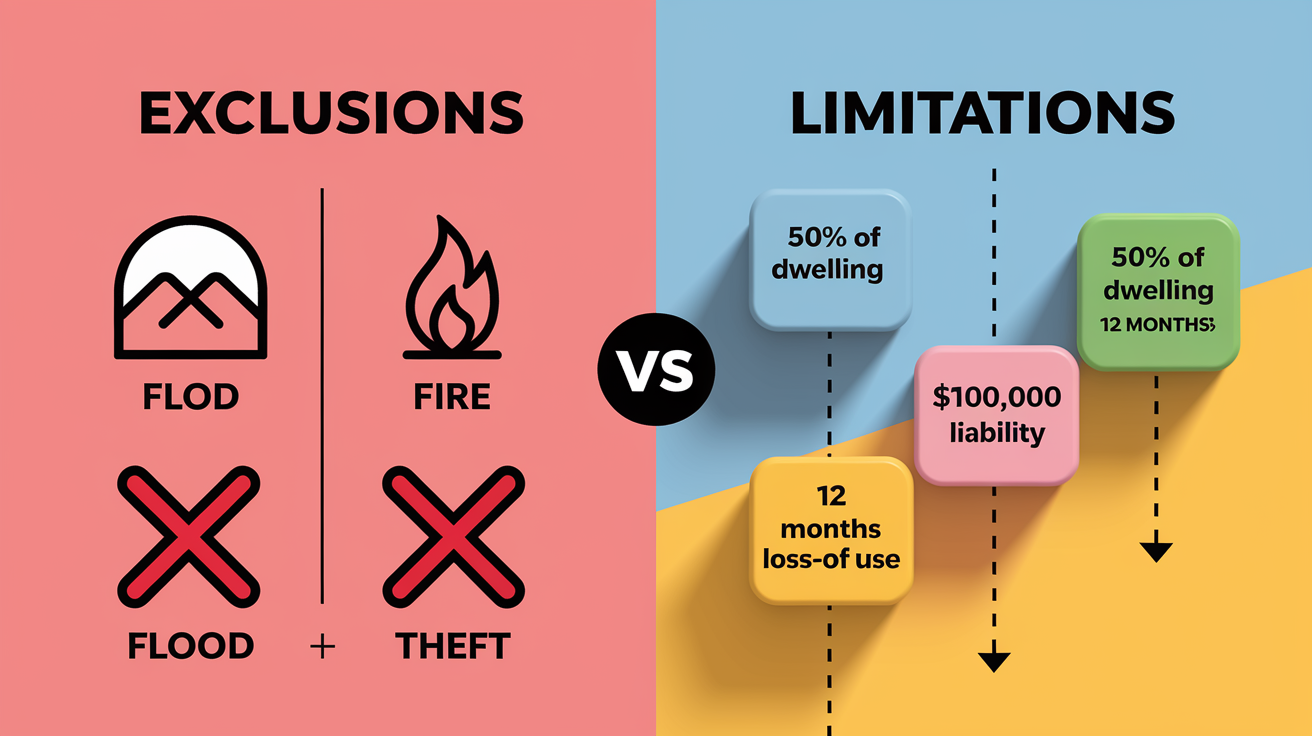

An exclusion means the insurer pays nothing for that risk; a limitation means they pay but only up to a cap or for a limited time.

This post cuts through the fine print so you can spot flood or intentional-act exclusions, dollar sublimits for jewelry and electronics, and the exact places on your declarations page to check.

By the end you’ll know which gaps to fix and which to accept.

Clear Breakdown of Policy Exclusions and Policy Limitations

A policy exclusion is a clause that cuts off coverage completely for a specific type of loss. When a risk is excluded, the insurer denies any claim tied to that cause, no matter how much damage you’ve got. Flood, government seizure, pest infestations, pre-existing damage. If your policy excludes flood and a river swamps your property, the claim gets denied. You’re paying for every dollar of repair yourself.

A policy limitation lets coverage stand but puts a ceiling on what the insurer pays or how long they’ll pay it. Limitations don’t kill coverage. They box it in. A dwelling limit of $250,000 often means your personal property limit sits at $125,000 (usually 50% of dwelling coverage). A liability policy capped at $100,000 pays claims up to that number, and anything past that is yours to cover.

The difference is straightforward: an exclusion triggers denial, a limitation triggers partial or capped payment. Exclusions show up in the “Exclusions” section, in defined terms, and in endorsements that add or strip away perils. Limitations appear on the declarations page (as dollar amounts or percentages), in sublimit schedules, and in conditions or endorsement language tied to time, category, or occurrence.

Here’s what each looks like:

- Exclusions: flood, government seizure or condemnation, nuclear hazard, intentional acts

- Limitations: 50% personal property sublimit, 12-month cap on loss-of-use payments, $100,000 personal liability ceiling, per-occurrence limit of $10,000 for jewelry unless you schedule it

How Policy Exclusions Function in Real Insurance Coverage

An exclusion works like a shut door. If the excluded peril causes the loss, the insurer pays nothing. Excluded perils get named directly: flood, earthquake, war, nuclear events, intentional damage, government action. These clauses exist because the risk can’t be insured at standard premium rates or belongs in a separate, specialized policy. Flood is almost always excluded from standard homeowners coverage and has to be written through a dedicated flood program or private flood insurer. Same goes for earthquake in seismic zones.

When you file a claim for an excluded peril, the denial letter cites the exclusion clause by name and page number. There’s no negotiation over amount. The entire claim gets rejected. If you want future protection, you’ll need to buy a separate policy or attach an endorsement before the next loss event. That additional coverage costs extra, and insurers won’t add it after damage has already occurred.

Common categories of exclusions:

- Natural perils sold separately (flood, earthquake, landslide, subsidence in some states)

- Intentional or criminal acts by the insured (arson, fraud, deliberate destruction)

- Government or regulatory action (seizure, condemnation, code-upgrade mandates in some cases)

- Wear, tear, and maintenance failures (gradual deterioration, mold from long-term leaks, pest infestations)

- Specific liability exposures (pollution, professional services, business activities conducted at home)

How Policy Limitations Restrict Coverage Without Eliminating It

A limitation sets boundaries on how much or how long coverage applies, but it doesn’t erase the coverage itself. The most common form is the dollar cap. A dwelling coverage limit of $300,000 caps the insurer’s payout for rebuilding, even if actual replacement cost runs higher. Personal property frequently gets limited to a percentage of the dwelling amount. 50% is typical, so that $300,000 dwelling yields a $150,000 contents limit. Loss-of-use benefits (hotel, rental, meals above your normal spending) often cap at 12 months or a fixed dollar amount, whichever comes first.

Liability policies impose per-occurrence limits and aggregate (annual) limits. A $100,000 liability limit means the insurer pays up to $100,000 per incident for bodily injury or property damage judgments and defense costs. If two claims pop up in one year and each hits $100,000, the insurer pays both, unless the policy also includes an annual aggregate that stops payment once total payouts hit a certain ceiling. Sublimits restrict coverage further for specific categories. Jewelry might cap at $2,500 total, electronics at $5,000, or business property at $2,500 unless you schedule those items separately.

| Limitation Type | Example Value |

|---|---|

| Personal property sublimit | 50% of dwelling limit ($150,000 when dwelling is $300,000) |

| Loss-of-use cap | 12 months or $30,000, whichever is reached first |

| Personal liability limit | $100,000 per occurrence |

Side-by-Side Comparison of Exclusions and Limitations in Practice

Understanding which clause applies tells you whether you’re getting a denial letter or a check with a lower-than-expected number. An exclusion shuts the door completely. Flood damage when flood is excluded means $0 paid. A limitation keeps the door open but only partway. Fire destroys your home and all your belongings, dwelling coverage pays up to $250,000 for the structure, and the 50% personal property sublimit pays up to $125,000 for contents, even if your actual furniture, clothing, and electronics were worth $200,000.

The distinction shows up clearly during claims. If your city condemns your building and forces demolition, and your policy excludes loss due to government action, the insurer denies the claim and you absorb the entire financial hit. If instead a covered fire destroys the same building, the insurer pays up to your dwelling limit (let’s say $250,000), but if rebuilding costs $280,000, you pay the $30,000 difference out of pocket. That’s a limitation, not an exclusion.

Exclusions typically require you to buy separate coverage or endorsements. Limitations can often be addressed by increasing your policy limits or scheduling high-value items. For example, if you own $50,000 in jewelry but your standard sublimit is $2,500, you can schedule the jewelry separately, pay a higher premium, and eliminate that sublimit. You can’t schedule coverage for a peril that’s excluded. You need a different policy altogether.

| Feature | Exclusion | Limitation |

|---|---|---|

| Coverage outcome | No payment; claim fully denied | Partial or capped payment |

| Typical trigger | Named peril (flood, government action, intentional act) | Dollar ceiling, time window, or per-item cap |

| How to address | Buy separate policy or endorsement (before loss) | Increase limits, schedule items, or add umbrella coverage |

| Example | Flood excluded → flood claim pays $0 | $250,000 dwelling limit → insurer pays max $250,000 even if rebuild is $280,000 |

Real-World Claim Scenarios That Illustrate These Clauses

A homeowner near a river experiences flooding after heavy rain. The water damages floors, drywall, and electrical systems. Total repair estimate is $80,000. The homeowners policy excludes flood. The insurer denies the entire claim, citing the flood exclusion on page 12 of the policy. The homeowner didn’t purchase separate flood coverage, so the $80,000 loss gets paid out of pocket.

Same homeowner suffers a kitchen fire six months later. The fire destroys the kitchen and spreads smoke damage through the rest of the house. Dwelling repairs cost $60,000. Contents lost (appliances, furniture, clothing) total $90,000. The policy has a $250,000 dwelling limit and a personal property limit of $125,000 (50% of dwelling). The insurer pays the full $60,000 for structure repairs but caps contents payment at $125,000, leaving the homeowner whole on contents in this instance. Had contents been worth $150,000, the $125,000 sublimit would’ve created a $25,000 gap.

Four scenarios that show how these clauses operate:

- Government condemnation (exclusion applies). City orders demolition due to code violations; policy excludes government action → claim denied, $0 paid.

- Total loss with dwelling limit (limitation applies). Fire destroys home, rebuild cost $280,000, dwelling limit $250,000 → insurer pays $250,000, homeowner pays $30,000 shortfall.

- High-value jewelry theft (sublimit applies). Jewelry worth $20,000 stolen, standard sublimit $2,500 → insurer pays $2,500 unless jewelry was scheduled separately.

- Liability claim exceeding limit. Guest injured, court awards $150,000; policy liability limit $100,000 → insurer pays $100,000 plus defense costs (if within limit), homeowner liable for remaining $50,000.

Where to Locate Exclusions and Limitations in Your Insurance Policy

Start with the declarations page. This summary lists your dwelling coverage amount, liability limit, and any endorsements or riders attached to the base policy. If your dwelling limit is $300,000, you can infer that your personal property limit is likely $150,000 (50% formula) unless the declarations page states otherwise. The declarations page also flags endorsements by name (“Earthquake Endorsement,” “Scheduled Personal Property,” “Increased Jewelry Coverage”), which modify exclusions or raise sublimits.

Next, turn to the section titled “Exclusions,” “What Is Not Covered,” or “Policy Conditions.” Read every listed peril line by line. Look for flood, earthquake, government action, nuclear hazard, intentional loss, and wear-and-tear language. Some exclusions get buried in definitions or conditions rather than grouped in one place, so scan defined terms for language like “We do not cover loss caused by…” or “Coverage does not apply to…” Endorsements can add coverage back in (for example, a flood endorsement converts the flood exclusion into covered peril for an additional premium), so always check attached endorsements and confirm what they modify.

Checklist for locating and interpreting these clauses:

- Read the declarations page and note Coverage A (dwelling) amount, liability limit, and listed endorsements.

- Find the “Exclusions” section and identify all named perils that produce $0 payment.

- Look for sublimit schedules or percentage formulas (e.g., “personal property limited to 50% of Coverage A”).

- Check for time-based limits (“loss of use payable for up to 12 months”).

- Scan endorsements for language that adds perils (for a fee) or raises caps.

- Search definitions and conditions for additional exclusion or limitation language not grouped in the main sections.

Legal and Interpretive Rules Affecting Exclusions and Limitations

Insurance policies are contracts of adhesion. The insurer drafts them, the consumer accepts or declines without negotiation. Courts in most states impose a duty on insurers to use clear, unambiguous language. When an exclusion or limitation is vague or open to two reasonable interpretations, the law typically resolves the ambiguity in favor of the policyholder. This doctrine, known as contra proferentem, means that if an insurer wants to deny coverage or cap payment, the exclusion or limitation must be written plainly enough that an ordinary person would understand it.

Vague exclusions are a frequent source of litigation. An insurer might cite a “pollution exclusion” to deny a mold claim, arguing that mold is a contaminant. If the policy doesn’t define “pollution” or “contaminant” clearly, and a reasonable person might interpret mold as ordinary water damage rather than pollution, courts often rule for the insured. Same applies to limitations. If a sublimit clause references “jewelry and furs” but doesn’t specify whether family heirlooms or costume jewelry are included, ambiguity favors broader coverage.

Disputes over exclusions and limitations drive most coverage litigation. When a claim gets denied or reduced based on unclear contract language, the insured can challenge the insurer’s interpretation through appraisal, arbitration, or lawsuit. Bad-faith claims arise when an insurer relies on a strained or unreasonable reading of an exclusion to deny a valid claim. If the insurer loses, it may owe not only the claim amount but also penalties, attorney fees, and extra-contractual damages.

How to Modify or Strengthen Coverage When Exclusions or Limitations Are a Problem

If your policy excludes a peril you need covered (flood, earthquake, or sewer backup), ask your insurer or agent about endorsements or separate policies. Flood coverage is almost always a standalone policy through the National Flood Insurance Program or a private carrier. Earthquake and sewer-backup coverage are typically available as endorsements for an additional premium. Premiums vary widely based on location, construction type, and claim history, but adding these endorsements is usually cheaper than buying a second full policy.

When a limitation creates a coverage gap, you’ve got three main strategies. First, increase your dwelling limit. If you raise coverage from $300,000 to $400,000, and personal property is pegged at 50%, your contents sublimit rises from $150,000 to $200,000. Second, schedule high-value items separately. Jewelry, art, collectibles, and electronics can be listed on a schedule with agreed values, bypassing the standard sublimits. Third, raise liability limits or add an umbrella policy. If your homeowners liability cap is $100,000 and you own significant assets, a $1 million umbrella policy sits above your base coverage and pays after the underlying limit is exhausted.

Three coverage-improvement options when exclusions or limitations are inadequate:

- Purchase standalone or endorsed coverage for excluded perils (flood, earthquake, sewer backup). Costs vary by region and risk but are necessary before a loss event.

- Increase base policy limits (dwelling, liability) to lift associated sublimits and reduce out-of-pocket exposure during total-loss scenarios.

- Schedule high-value personal property separately with itemized values to eliminate per-item or category sublimits. Typical for jewelry, art, musical instruments, and electronics.

Common Confusions About Exclusions and Limitations Answered

Many policyholders assume that “limited coverage” and “excluded coverage” mean the same thing. They don’t. Limited coverage means the insurer will pay something, up to a stated cap or under defined conditions. Excluded coverage means the insurer pays nothing for that peril. Period. If you confuse the two, you may expect a partial payment when in fact you’re getting a denial letter, or you may not pursue higher limits when you actually need them.

Another common mix-up involves deductibles, coinsurance, and sublimits. A deductible is the amount you pay before the insurer pays anything, common in health and auto policies, and increasingly in property policies for wind or hail claims. Coinsurance (in property insurance) penalizes you for underinsuring. If you carry only 80% of the required coverage, the insurer reduces claim payments proportionally. A sublimit is a ceiling on payment for a specific category or peril, regardless of your overall policy limit. These are three separate concepts, and each one affects your out-of-pocket costs differently.

Five concise clarifications on frequent misunderstandings:

- “Excluded” means no coverage at all for that peril; “limited” means coverage exists but is capped or conditional.

- A sublimit isn’t the same as a deductible. Sublimits cap how much the insurer pays for a category; deductibles reduce every covered claim by a fixed amount you pay first.

- Endorsements can convert an excluded peril into a covered one (for an added premium), but they can’t retroactively cover a loss that already happened.

- Time-limited coverage (e.g., 12-month cap on loss of use) is a limitation, not an exclusion. You still get paid, just not indefinitely.

- Increasing your dwelling limit often raises associated sublimits (like personal property at 50%), but it doesn’t remove exclusions. You still need separate coverage for excluded perils.

Final Words

When a claim hits, you now know the difference: exclusions remove coverage, limitations shrink what the insurer pays. That’s the action that breaks or makes your wallet.

You’ve seen where these clauses live (declarations page, exclusions, endorsements), common exclusions like flood or government action, and numeric limits such as a 50% contents cap or $100,000 liability ceiling.

Keep the policy exclusion vs policy limitation question front and center when shopping or updating coverage. Ask for endorsements, schedule valuables, and get written limits. Do that and you’ll avoid the worst surprises.

FAQ

Q: What are limitations and exclusions?

A: Limitations and exclusions differ: an exclusion removes coverage for a cause (flood, government action, infestation, pre-existing damage). A limitation restricts or caps payment (sublimits, time limits). Look on the declarations, exclusions section, or endorsements.

Q: What is an example of a policy limit?

A: An example of a policy limit is a $250,000 dwelling limit that yields a 50% personal property cap ($125,000); a $100,000 liability ceiling is common, while flood is often excluded entirely.

{kind=link}